When people think about building a digital bank, they usually imagine the visible part of the product: a mobile app, accounts, cards, payments, onboarding, notifications, and a clean user interface.

But the real complexity starts behind the screen.

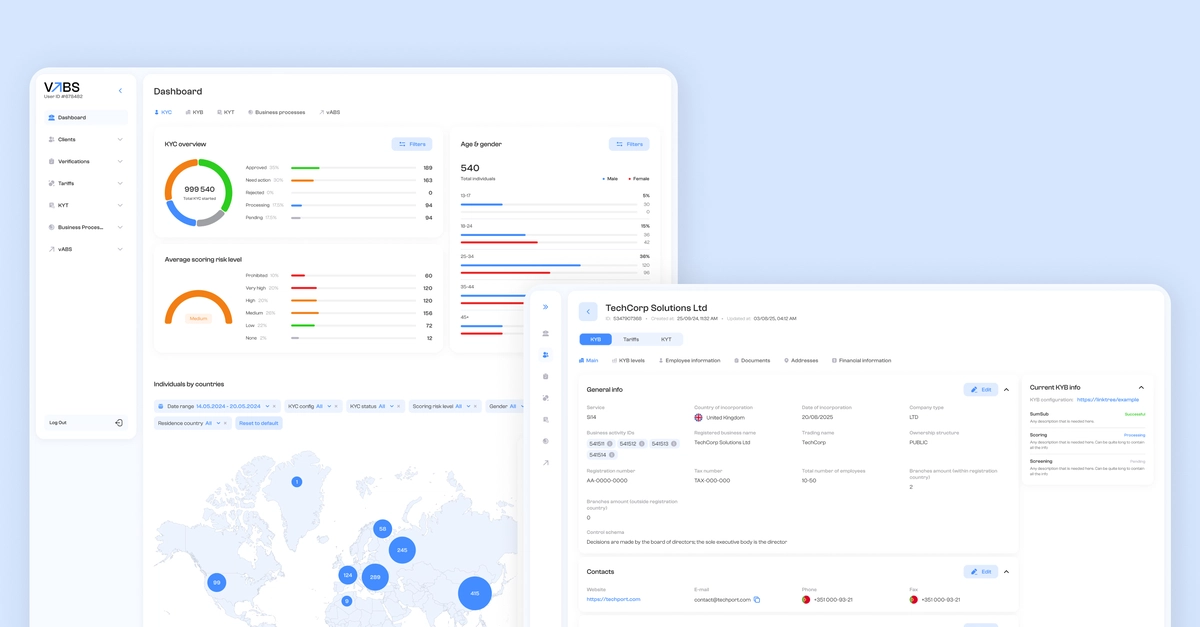

A digital banking product needs a reliable core ledger, account logic, payment routing, transaction monitoring, KYC and KYB workflows, AML controls, reconciliation, tariffs, limits, internal approvals, audit logs, support tools, reports, and operational dashboards.

Without this internal layer, even a well-designed fintech app becomes difficult to scale. Payments are checked manually. Compliance teams work with scattered data. Finance teams reconcile transactions in spreadsheets. Support teams do not see the full client context. Every new product or payment provider requires custom internal logic.

This is the problem VABS was built to solve.