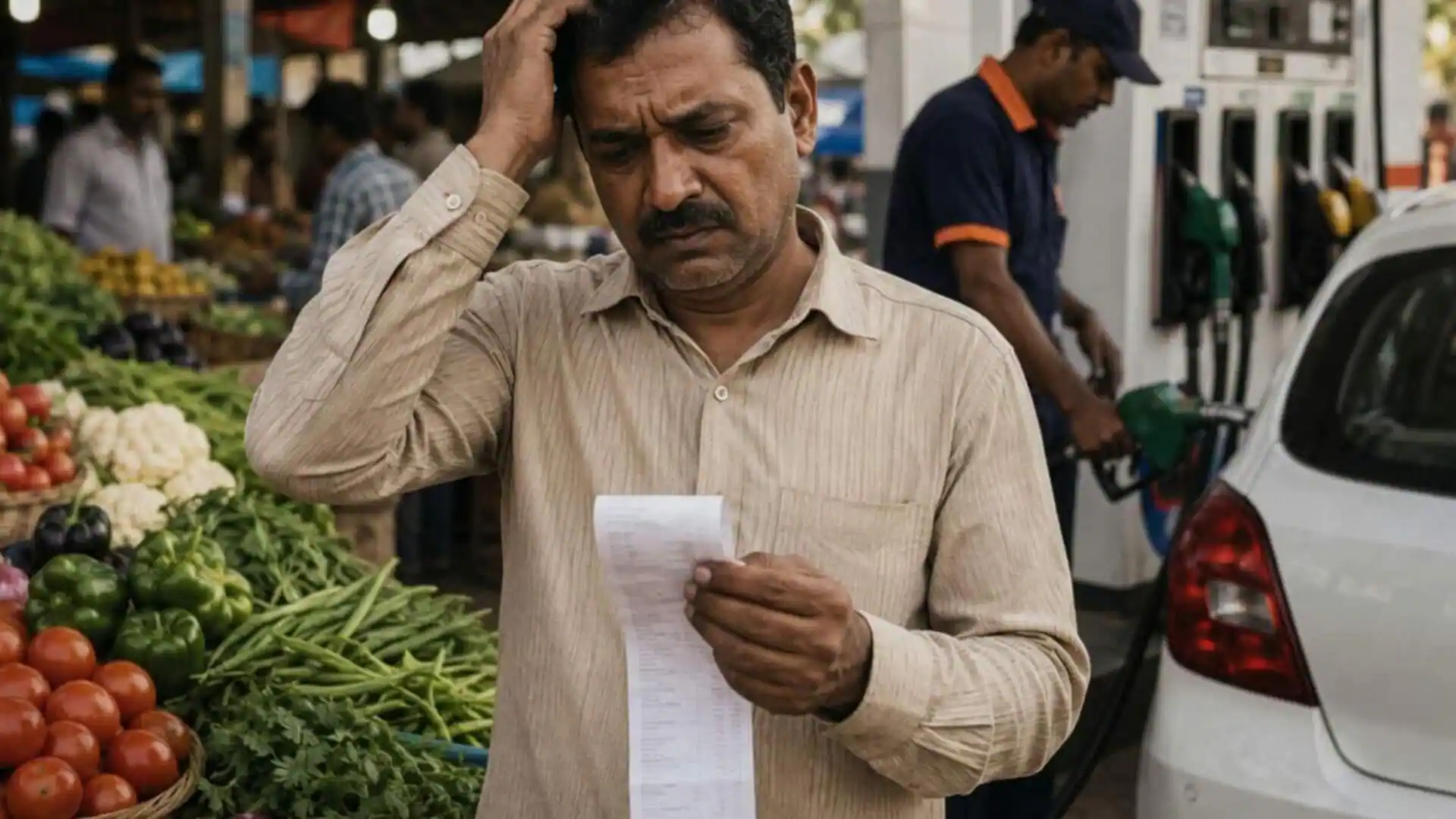

India’s consumer price index inflation for June 2026 rose to 4.38% from 3.93% in May mainly because of higher food and fuel prices. It has crossed the Reserve Bank of India (RBI’s) inflation target of 4% and is now moving to its upper tolerance band of 6%. If inflation keeps rising for next some months because of rising fuel costs, uncertain global geopolitical conditions among other factors, there is a possibility that the RBI may increase the repo rate in the next few Monetary Policy Committee (MPC) meetings. Rising inflation is also seen as one of the indicators of fixed deposit interest rate hike, specially on short-to-medium term deposit. It’s not just rising inflation, but there are some other factors, such as high credit demand, low deposit, high bond yield, competitive interest rates from other schemes, that are also indicating that banks may raise FD rates in the future. The question is when banks may start taking such a step. Here are some of the indicators that suggest why banks may increase FD rates in the next few months.Also Read: 8th Pay Commission HRA calculator: Can HRA go up to Rs 1,93,000/month? HRA estimates for Level 14-18 employees at 2.0, 2.1, 2.28, 2.57 fitment factors Rising inflation Inflation has risen significantly in the last few months, from 2.74% in January to 4.38% in June. Adhil Shetty, CEO, BankBazaar.com, says concerns around the monsoon and global geopolitical tensions kept inflationary pressures elevated. Shetty further says whether inflation remains above the RBI's 4% target will depend on the progress of the monsoon, food supply conditions, crude oil prices and global developments. Anand K Rathi, co-founder, MIRA Money, says recent energy shock and higher crude oil prices have also made transportation more expensive, which is making inflation worse. When inflation rises for a long term, the RBI reciprocates with increasing the repo rate. Shetty says at present, one month of inflation above 4% may not be enough to justify an immediate increase in the repo rate, but if inflation remains elevated over the coming months or moves closer to 6%, the possibility of a rate hike would increase.Also Read: OPS vs CPS: Andhra Pradesh allows one-time switch to Old Pension Scheme for eligible employees; check who qualifiesA high repo rate may provide cushion for banks to increase FD rates on some of its deposits. Deposit-credit growth Banks also monitor deposit growth, credit demand and liquidity conditions before making FD rate changes. Shetty says that the gap between credit and deposit growth has widened in recent months, meaning banks are lending faster than they are mobilising deposits. “When this gap persists, banks may need to attract more deposits to support future lending, and offering higher FD rates is one way to do that,” says Shetty. However, liquidity conditions and each bank's funding position also influence how quickly deposit rates move. 10-year G-Sec yield is high Banks try to keep their FD rates higher than government securities to attract investors. 10-year G-Sec is considered as an important benchmark for many interest rates in India. 10-year G-Sec yield has come down from 7% in early June to 6.775%. But it is still higher than FD rates of many banks. A high 10-year G-Sec rate also indicates that banks are likely to consider raising FD inter rates due to competitive pressure. High interest rates on small savings schemes Many small savings schemes are providing over 7% interest rates to their depositors. Despite many indicators suggesting so, the government hasn’t decreased interest rates of these schemes since December 2024. High interest rates of small savings schemes are providing a stiff competition to FD rates of many banks. If banks want to raise more deposits, they will have to compete with small savings interest rates and they will be compelled to consider interest rate hike When can banks increase FD rates? Raj Khosla, founder & managing director, MyMoneyMantra.com, says although there is no mandated timeframe, as soon as the RBI brings any policy change, banks typically revise their FD rates within a few days to 4-6 weeks. The exact speed of revision depends on several banking operational factors, says Khosla. Shetty says some banks revise FD rates within a few days of an RBI policy change while others may wait for several weeks depending on their funding requirements and liquidity position. “Private sector and small finance banks often respond faster when they need deposits, whereas larger public sector banks may take longer if they already have sufficient liquidity,” explains Shetty. Khosla says it has been noted that banks often adjust short and medium-term FD rates more quickly than long-term rates. Rathi says banks may not increase rates on long-term deposits as they may think that the current inflationary forces are only temporary and may not want to lock in higher interest rates for a long time. We can see that while many indicators are suggesting banks may increase interest rates on certain FD tenures, it may still take some time before they make such a move. They may also wait for the RBI policy change, look at credit-deposit ratio, liquidity and a few other factors before deciding so.

Can banks increase FD interest rates as inflation crosses RBI’s target of 4%? - The Economic Times

Rising inflation has crossed the Reserve Bank of India's target, signaling potential repo rate hikes. Higher inflation and increased credit demand suggest banks might raise fixed deposit interest rates soon. Banks monitor deposit growth and credit demand before adjusting their fixed deposit rates. High yields on government securities and small savings schemes also pressure banks to increase FD rates.

859 words~4 min read