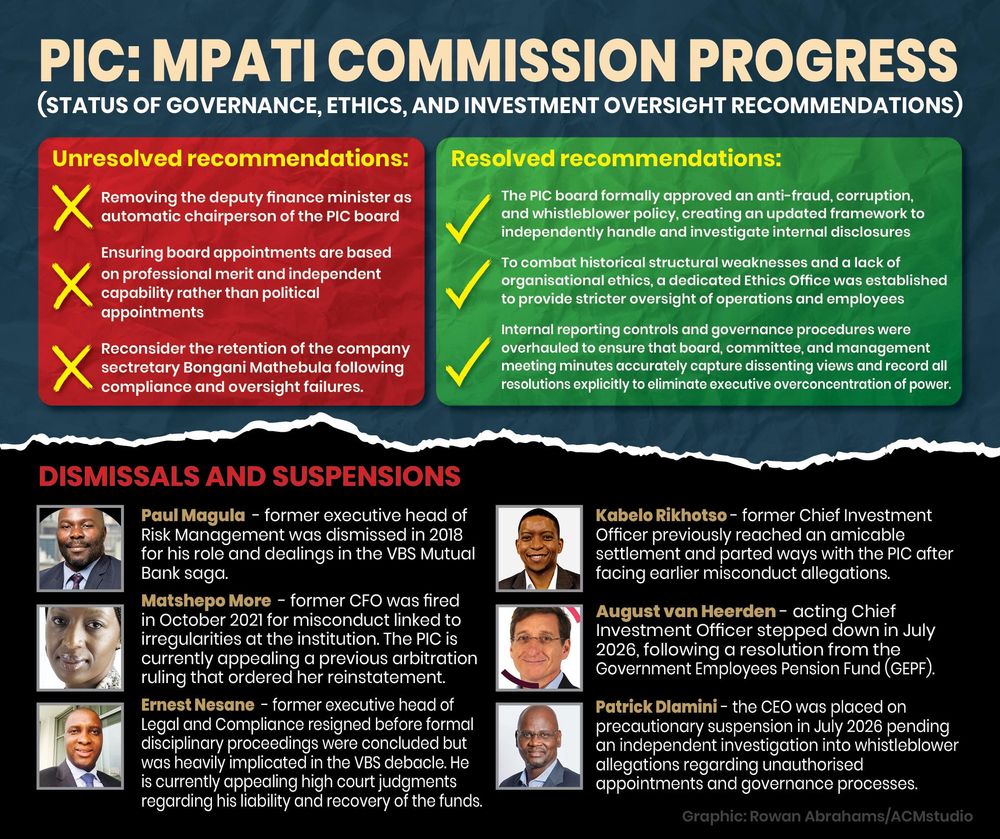

In the world of asset management, there is no endorsement more coveted than a mandate from the Public Investment Corporation (PIC). As the asset manager with more than R3-trillion to invest, the PIC is the bedrock of the asset management ecosystem and has, over many years, operated as a lifeline for some businesses seeking to gain a foothold in the market. To be granted a mandate from the PIC is not easy for obvious reasons. Since so many potential players can approach the PIC, it has to implement stringent measures of vetting and assessing asset managers before giving them the responsibility to manage funds on its behalf. Chancers with no core skills or track record in managing third-party funds responsibly are unlikely to get any share of the PIC mandate. The scrutiny applied in the vetting process means that few poorly governed or technically incompetent managers will get far in the process.Considering how robust such processes are, it boggles the mind to see just how consistently dire and diabolical the PIC’s own governance is. As an institution that has its genesis from the public debt commissioners, the PIC’s architecture has always involved representatives of public servants in its model. The corporatisation of the PIC in 2004 meant that it shifted towards a company structured and governed in line with the practices adopted by many other companies that operate in South Africa. In this dimension, the best governance practices of many large institutions should have prevailed. Unfortunately, the historical “imbalance” between representatives of the public servants whose funds are being managed and the investment and governance gurus who have an intimate appreciation of the complexities associated with governing institutions of its kind remains a perennial challenge. That dilemma is best captured by the fact that unlike other companies where the question of who is best to chair the board may be subject to some element of deliberation, the PIC is essentially compelled to accept whoever serves as the deputy finance minister of the day to be its chair. That on its own is not fatal, as a deputy finance minister may indeed be capable of leading a board with great distinction.The core issue is that in cases where political considerations overwhelm governance commitments, or the deployed politicians are perhaps not the best suited to lead the board at that point, the board is paralysed unless the politicians of the day trigger a political shuffle, which may be due to reasons that are far removed from the question of what works best for the PIC. To complicate the matters further, the governance model requires the concurrence of the shareholder representative in some key matters. That right happens to be exercised by the political boss of the PIC’s chair, which, if consensus materialises, is not an issue. But when the meeting of the minds does not materialise it is unclear how such deadlocks can be broken. During the process of untangling the governance mess of the PIC a few years ago, the Mpati commission recommended that the model of deploying a politician to chair the PIC should be revisited. The ANC government resisted the recommendation. While the Mpati recommendation may have been influenced by the simple proposition that the PIC should be able to have the best chair available rather than limiting the canvas to just one deployed politician, the current impasse where the two politicians are responsible for the PIC at the board and shareholder level is the most convincing illustration of how broken the model is. The irony is that as the PIC demands good governance from those seeking to do business with it, it simultaneously has no idea what good governance actually entails.• Sithole is an accountant, academic and activist.Business Day

KHAYA SITHOLE | The PIC demands governance it does not practise

Political appointments and structural weaknesses undermine PIC's own governance

621 words~3 min read