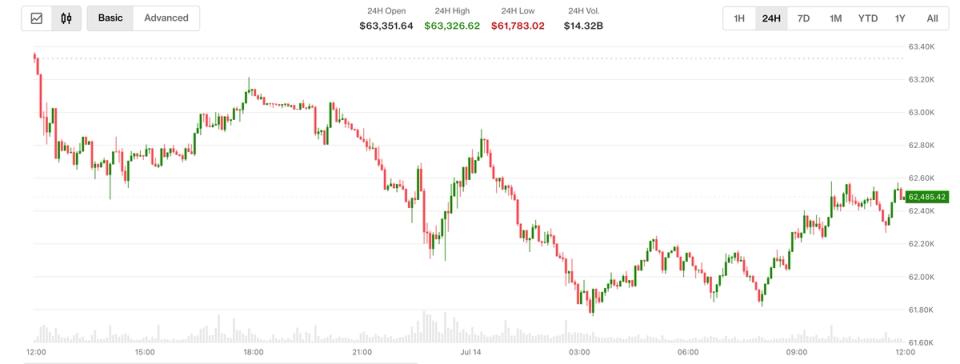

US Treasury prices jumped on July 14 after the June Consumer Price Index came in below expectations, prompting traders to rapidly unwind bets that the Federal Reserve would raise interest rates in the near term. The bond rally pushed yields lower and sent a ripple through every asset class that cares about the cost of money, which is to say, all of them.

Just 24 hours earlier, the mood was very different. Fed Governor Christopher Waller had spent July 13 warning that stubborn core inflation could force the central bank’s hand on tightening. Money markets had priced in roughly a 50% probability of a rate hike at the July meeting, with near-100% odds baked in for a move by September. Then the CPI print landed at 8:30 a.m. ET and rewrote the script.

What the inflation data actually showed

The June CPI reading came in softer than economists had forecast, marking a welcome deceleration from May’s 4.2% year-over-year inflation figure.

Traders didn’t need a second invitation. The probability of a July rate hike dropped sharply after the release, and the near-certainty of a September move also softened. Treasury prices, which move inversely to yields, climbed as the market repriced the entire rate path.