Private credit investments have long been viewed as one of the main beneficiaries of the higher interest-rate environment. However, recent redemption limits imposed by certain evergreen vehicles have raised concerns among investors. Do you see this as a temporary liquidity issue, or as a structural warning sign for the broader industry?

Evergreen funds are usually structured with quarterly redemption clauses, requiring investors to indicate in advance their wish to get out of the fund at its net asset value (NAV). The fund manager assesses these aggregated requests to serve them on a best effort basis, when there is cash available for redemption –, that is to say cash coming as a repayment of underlying investments plus any profit.

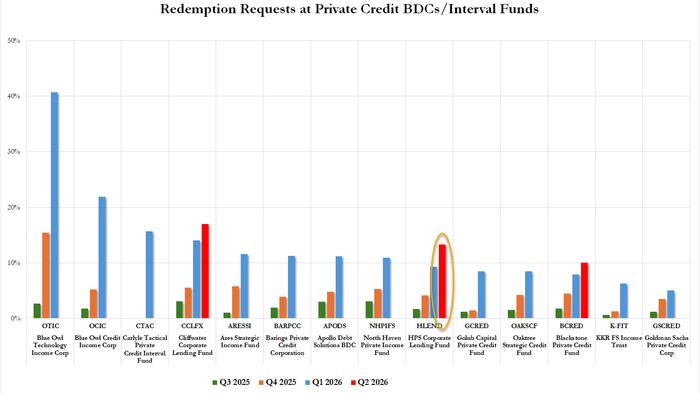

The volume of redemptions is usually capped in evergreen funds at 3 to 5% of the NAV of evergreen funds per quarter. These limits are embedded in the conception of the product and clearly indicated.

«The gating provides an indication of the perception of some investors but does not sum up the whole picture.»

Some evergreen fund managers communicated on the fact that recent aggregated redemption requests exceeded these limits, leading them to stop at the indicated threshold, a mechanism known as «gating». This gating provides an indication of the perception of some investors but does not sum up the whole picture. For example, evergreen funds often accept fresh capital from new investors while others have indicated their intention to leave.