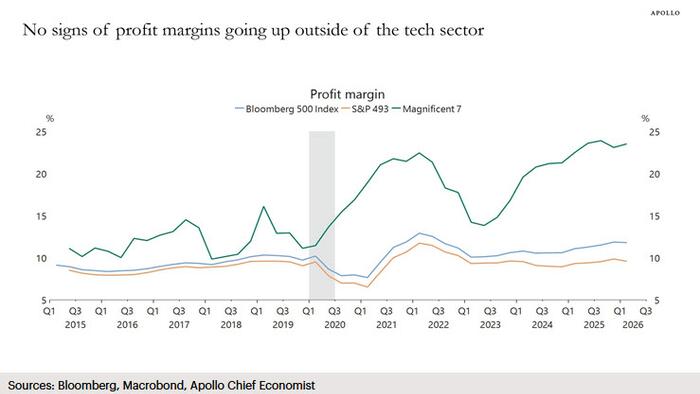

Here’s a number that should make you uncomfortable: the Magnificent Seven tech companies have seen their profit margins climb from roughly 15% in Q1 2023 to around 25% in Q1 2026. The other 493 companies in the S&P 500? They’re still parked at about 10%, exactly where they were three years ago.

Torsten Slok, chief economist and partner at Apollo Global Management, laid out this gap in a Daily Spark note dated June 30, 2026. His core argument is straightforward: if the hundreds of billions flowing into AI infrastructure aren’t actually making non-tech companies more profitable, then the valuations propping up the companies selling AI tools might be built on sand.

The ROI problem nobody wants to talk about

Companies in healthcare, banking, energy, manufacturing, defense, pharma, transportation, construction, and a dozen other sectors are spending on AI but not seeing it show up in their bottom lines. Profit margins across these industries have barely budged.

Slok warned this creates the conditions for what he called a “painful repricing” of AI company valuations. The logic is almost mechanical. If the customers buying AI products aren’t getting richer from using them, eventually they slow down. When that happens, the revenue growth baked into Big Tech stock prices starts looking optimistic.