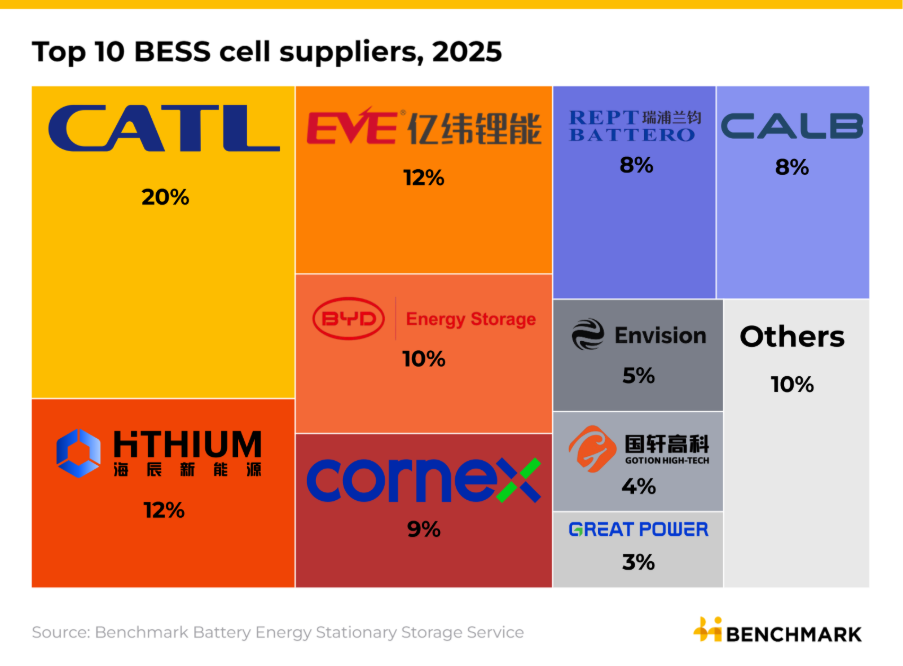

China’s CATL, the world’s largest BESS cell manufacturer with 121GWh shipped in 2025, does not appear in Wood Mackenzie’s integrator rankings because it operates primarily as a cell supplier rather than delivering turnkey systems.

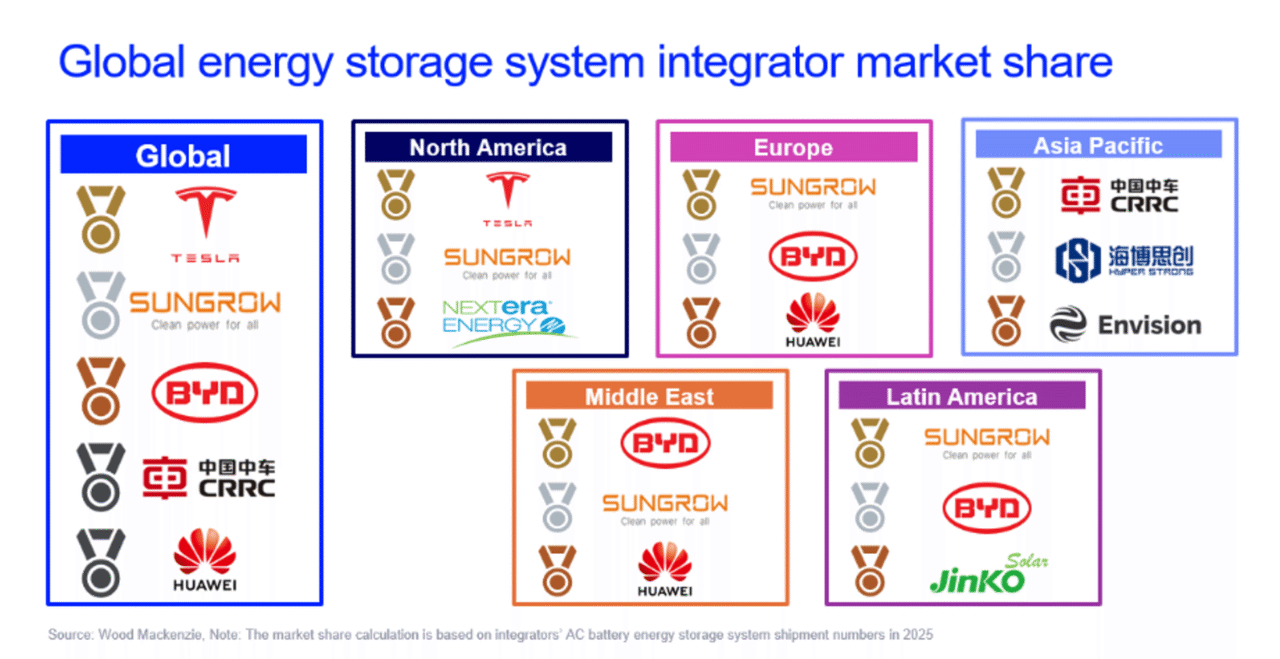

The integrator market is more fragmented than cell manufacturing. The top 10 system integrators captured approximately 68% of the market in 2025, with the remaining 32% split among Tier 2 and Tier 3 players, up from just 18% in 2024.

Regional dynamics

In North America, Tesla retained its leadership position, supported by its Megapack hardware, Autobidder software, and US-based manufacturing. NextEra Energy entered the top three for the first time, benefiting from its vertically integrated position.

The competitive landscape faces imminent transformation through new federal legislation. The “One Big Beautiful Bill Act” (OBBBA) establishes escalating domestic content requirements for projects seeking federal tax incentives, beginning at 55% in 2026 and reaching 75% by decade’s end. These thresholds create substantial barriers for Chinese suppliers.