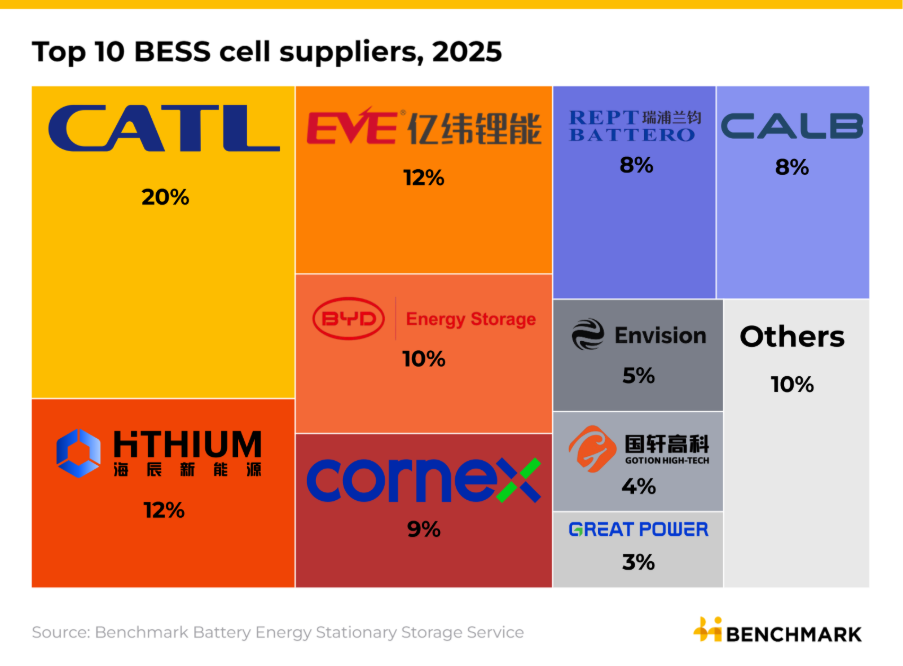

CATL in 2025 was the only cell manufacturer globally with over 100GWh of capacity dedicated to BESS. In 2026, planned expansion from EVE Energy and Hithium will see them both also surpass 100GWh of dedicated BESS capacity, with CORNEX, CALB, BYD and Great Power not far behind, each expected to exceed 70GWh of expected by year-end.

Close behind CATL, Hithium and EVE Energy each captured approximately 12% of cell shipments, taking second and third place respectively.

For Hithium, this represents a significant step up from fourth place and 9% share in 2024. The company signed a five-year, 120GWh cooperation agreement with system integrator CRRC in December 2025, underpinning continued growth.

EVE Energy, which had held second place in 2024, dropped to third but remains strongly competitive: in 2025 the company secured more than ten cell offtake agreements of at least 1GWh each, including a 50GWh deal with HyperStrong and 20GWh with Rochenergy. EVE Energy has sustained that momentum into 2026, leading offtakes YTD with over 160GWh of offtakes signed in H1 alone.

BYD, simultaneously leading the system shipment rankings, leveraged its vertically integrated position to reach a 10% share of cell shipments, placing fourth.