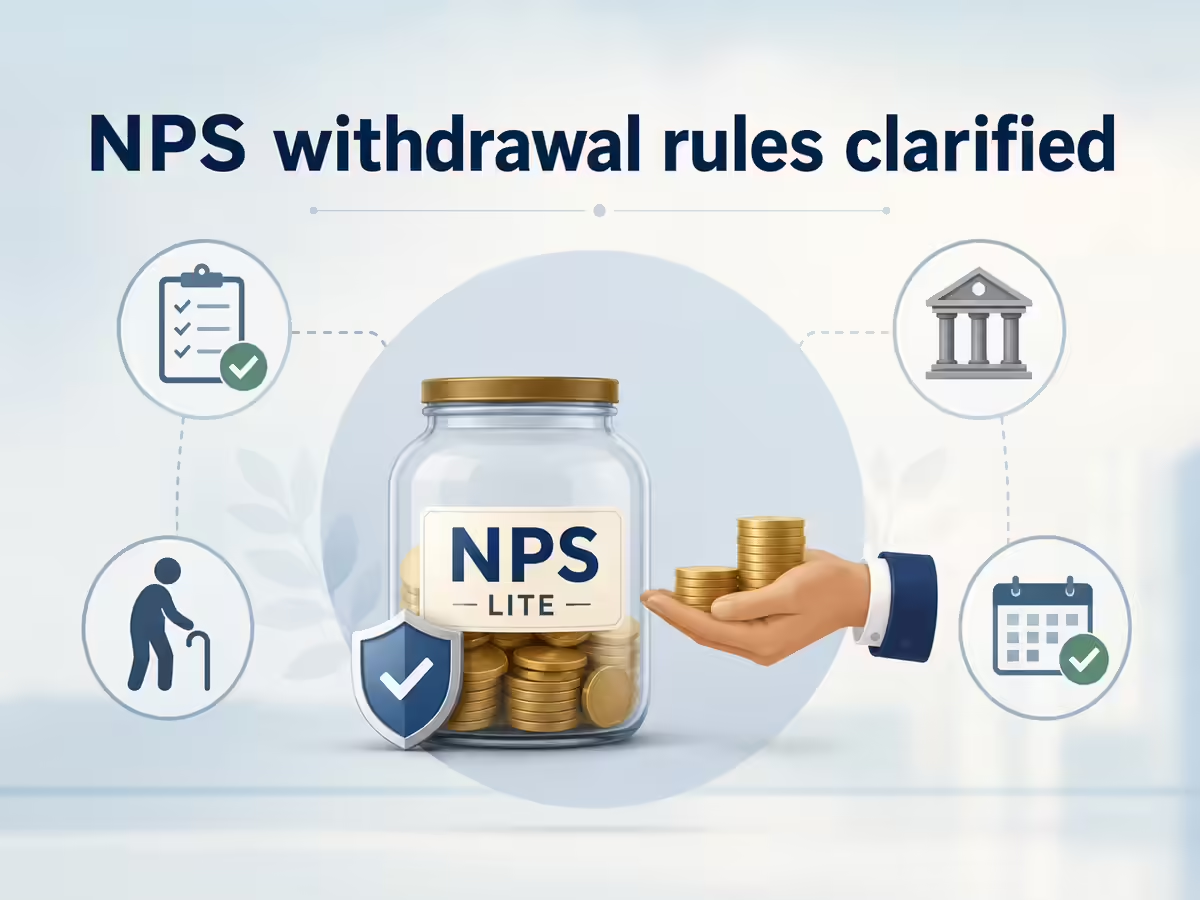

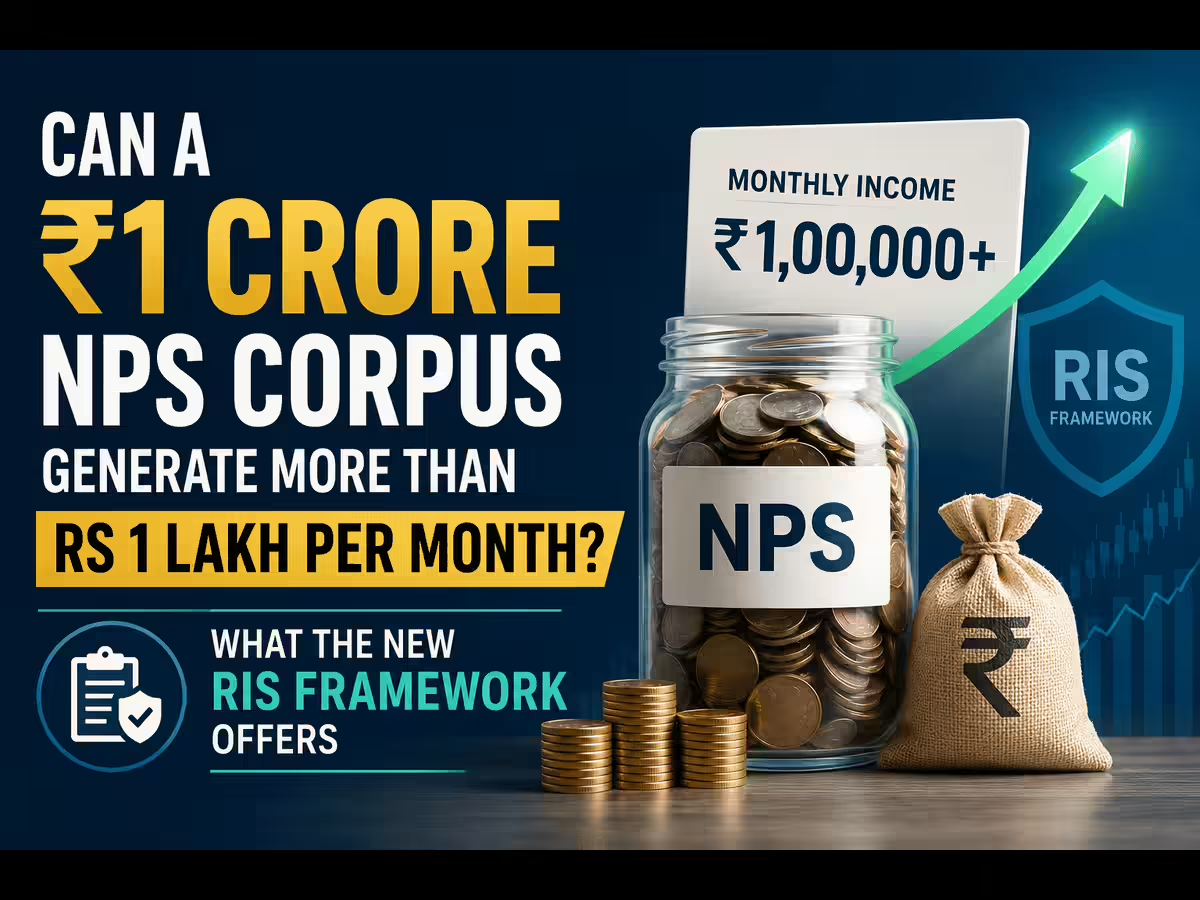

For years, the one persistent complaint about the National Pension System (NPS) was its rigidity at exit. You built a retirement corpus over 20-30 years, and at 60, the rulebook decided you couldn’t simply walk away with it. A large chunk had to go into an annuity. That has now changed. Let us understand what’s on the table.What changedIn December 2025, PFRDA substantially amended NPS exit/withdrawal norms. The mandatory annuity portion has come down from 40 per cent to 20 per cent of corpus viz. subscribers can withdraw up to 80 per cent as lump sum against 60 per cent earlier. For smaller corpus, the rules are more generous. If accumulated NPS wealth is up to ₹8 lakh, you can withdraw the entire amount as lump sum. For ₹8-12 lakh, you can take out up to ₹6 lakh with the balance routed into structured withdrawal or annuity. Above ₹12 lakh, the 80:20 split applies.However, there’s a tax issue here. Section 10(12A) of the Income Tax Act exempts only 60 per cent of withdrawn corpus. The additional 20 per cent PFRDA permits you to withdraw, gets taxed at a slab rate unless the tax law catches up with the new pension norms. So, the extra liquidity is real, but plan for tax bill on the incremental 20 per cent rather than assuming it’s tax-freeRetirement planningThe practical upshot is, NPS now gives you more control on the day you stop earning salary. Earlier, a large slice of money was locked into an annuity that paid a modest return, with limited say in how it was structured. Now, you can keep much bigger share of corpus working for you in instruments and at a pace you choose. That’s particularly useful if you already have other income sources at retirement or want to deploy a chunk into something more efficient, like paying off a loan.The flip side is this freedom shifts the responsibility for managing market and longevity risk back onto you. The new system trusts you to manage a larger pool of money sensibly over a 20-25-year retirement. It needs more care.RIS, variantsThis is where PFRDA’s newer reform comes in — the Retirement Income Scheme (RIS). Until recently, if you didn’t want to take lump sum at once, the main alternative was to defer withdrawal and take it out once a year, which wasn’t particularly useful for someone who needs monthly income to live on.RIS addresses that gap. It applies to the non-annuity portion of corpus and lets you draw it down gradually instead of taking it in one shot while the balance stays invested and continues to earn market-linked returns. Within RIS, you choose between two payout methods. One is Systematic Lump Sum Withdrawal or SLW, where you withdraw a fixed amount at a chosen frequency — monthly, quarterly, half-yearly or annually — until age 75 (now 85 in some cases). So it will run until the corpus runs out. The other is Systematic Unit Redemption (SUR), where you redeem a set number of units at each interval, so the payout itself varies with the prevailing NAV. Either way money stays within NPS, continues compounding and pays on schedule you set.MF SWPRIS is structurally very close to a Systematic Withdrawal Plan of mutual fund (MF). In both cases, you leave money invested and withdraw defined amount periodically rather than redeeming all at once.A MF SWP gives wider choice of schemes and you can switch funds/change withdrawal amount with no curbs on moving money. RIS is more limited in fund choice and governed by PFRDA’s process and timelines which means somewhat less flexibility.NPS has historically run at a fraction of the cost MFs charge so the expense drag on retirement corpus is lower under RIS. MF SWP withdrawals are taxed as capital gains while RIS withdrawals sit within NPS tax framework where 60 per cent is exempt and rest is taxed.Neither is really better. If cost efficiency and staying in a regulated pension structure matter more, RIS fits. For wider choice of underlying funds and ability to move quickly between them, MF SWPs give that.For the average subscriber, NPS treats retirement money the way most actually need it treated — accessible sans being reckless and flexible sans being chaotic. The combination of a higher lump sum limit, slab-based withdrawal for smaller corpus, and RIS as a built-in drawdown mechanism gives mass investors real choices at 60. The main thing to observe is discipline: more access to money is useful if you don’t withdraw faster than retirement actually needs.Joydeep Sen is a corporate trainer (financial markets) and an author.Published on July 5, 2026

What new NPS withdrawal rules mean for retirement

Explore the new NPS withdrawal rules that enhance retirement flexibility and accessibility while managing tax implications and risks.

769 words~3 min read