Show Caption

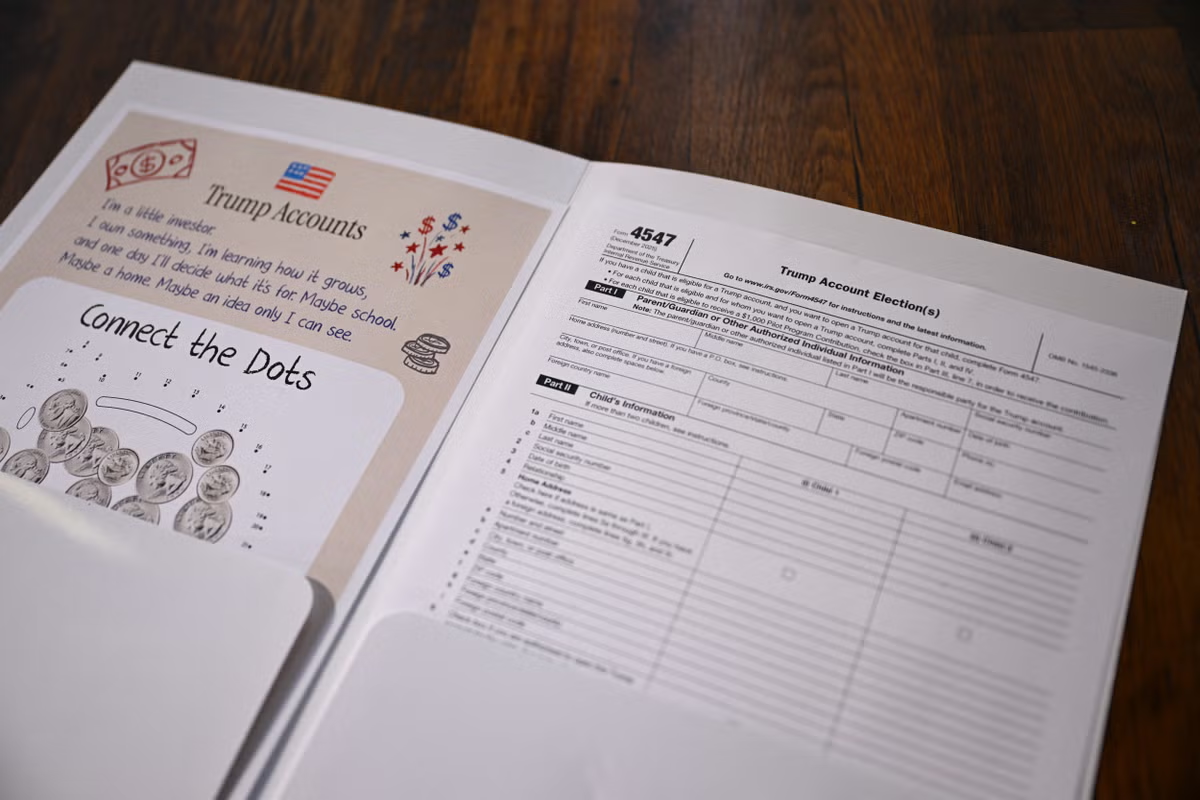

About 1.5 million American babies will receive $1,000 in their new Trump Accounts as America celebrates its 250th birthday this July 4, according to the U.S. Department of the Treasury.Trump Accounts officially launch on Independence Day, when the government opens the accounts. It will deposit $1,000 of "seed" money in each newborn's account to be invested and grow until the child reaches 18 years old. At adulthood, the account converts into a traditional IRA and takes on the same rules.Another roughly 5 million kids under 18 years who aren't newborns and have signed up for a Trump Account will have theirs activated on July 4, the Treasury said. They won't receive the $1,000 newborn seed money, but up to 25 million children aged 10 or younger who live in qualifying ZIP codes may receive a $250 charitable gift deposited by the Michael & Susan Dell Foundation. Everyone else can start receiving up to $5,000, adjusted for inflation after 2027, per child annually in total contributions from families, relatives and employers."For context, nearly 40% of Americans have no exposure to U.S. equities," said U.S. Treasury Secretary Scott Bessent earlier this month in a Senate Finance Committee hearing. "No stake in the companies they help to build; little share in the wealth they help to create. Trump Accounts represent a profound reimagining of that arrangement. They will ensure that every American child can benefit from private ownership and compound growth; that every American baby, in short, is born a shareholder."Is it too late to sign up for a Trump Account?There's still time to sign up for a Trump Account, and based on population data, millions of kids are eligible and missing out.According to the Census Bureau, in 2024, there were roughly 73.1 million children under age 18 nationwide, which means millions more children could still take advantage of the new tax-deferred investing accounts.To sign up, use the online portal at Trumpaccounts.gov or go to the IRS site, create or use your existing account and apply. The Treasury has also launched a Trump Accounts app, which can be used to complete setup and manage accounts.No contribution is necessary but encouraged once the account is open so savings can grow, the site said.Don't worry if the account isn't set up by July 4. You can still open an account anytime as long as the child is under 18 years old.Who qualifies for the $1,000 'seed' money?To get $1,000 from the government, the baby must:be born between Jan. 1, 2025, and Dec. 31, 2028.be a U.S. citizen.have a Social Security number.What do parents need to know about contributions?The annual limit is $5,000 per child from all non-government sources combined, with inflation adjustments expected after 2027. Employers can contribute up to $2,500 per year under an employer contribution program, and that amount counts toward the $5,000 cap but is generally excluded from the employee’s taxable income when structured through that employer program.Government entities and charities may also be able to make qualified general contributions for groups of children, and those amounts do not count toward the annual $5,000 cap.Are Trump Accounts worth it?When the accounts first launched many said other than the free $1,000 from the government, maybe not.If money's being saved to pay for school, for example, many financial advisers said 529 plans were better, citing the limited investing options for Trump Accounts and tax treatment. Trump Accounts will invest in low-cost index funds with no withdrawals allowed until the year the child turns 18 years old, when they'll be treated like a traditional IRA with basically the same rules. That means withdrawals will be taxed as ordinary income and could be subject to early withdrawal penalties if used for unqualified expenses.In contrast, 529s offer more investing options and withdrawals for qualified expenses are tax free."While Trump Accounts add an interesting new dimension to long-term planning, they are best viewed as a complement to existing education and retirement strategies, rather than a substitute," said California CPAs in an email.Other advisers, though, pointed to a loophole allowing Trump Accounts to ultimately convert to a Roth IRA instead of a traditional IRA that could provide a lifetime of tax-free savings.The loophole is that the year the child turns 18 and the Trump Account turns into a traditional IRA, it becomes eligible for a Roth conversion, advisers said. Transitioning into an IRA also opens up investment choices beyond only the low-cost index funds that the Trump Accounts allowed."And, if we're strategic about how we convert the Traditional IRA [formerly a Trump Account] when the child reaches age 18 there will be no tax on the Roth conversion," said Mat Sorensen, founder and chief executive of Directed IRA & Directed Trust Company, in a blog post.No tax on the Roth conversion assumes the teen has little-to-no income that'll put them in the zero federal tax bracket, he said. As long as "the taxable portion of the Roth conversion is under the standard deduction [$16,100 in 2026], they will pay no tax on the amounts converted," Sorensen said.However, even if a small amount of taxes are due, the conversion could be worth it for years of tax-free growth, advisers said."The Roth conversion is taxable, but the tax-free growth over many decades is appealing," said Richard Pon, certified public accountant in San Francisco.Medora Lee is a money, markets and personal finance reporter at USA TODAY. You can reach her at mjlee@usatoday.com and subscribe to our free Daily Money newsletter for personal finance tips and business news every Monday through Friday morning.