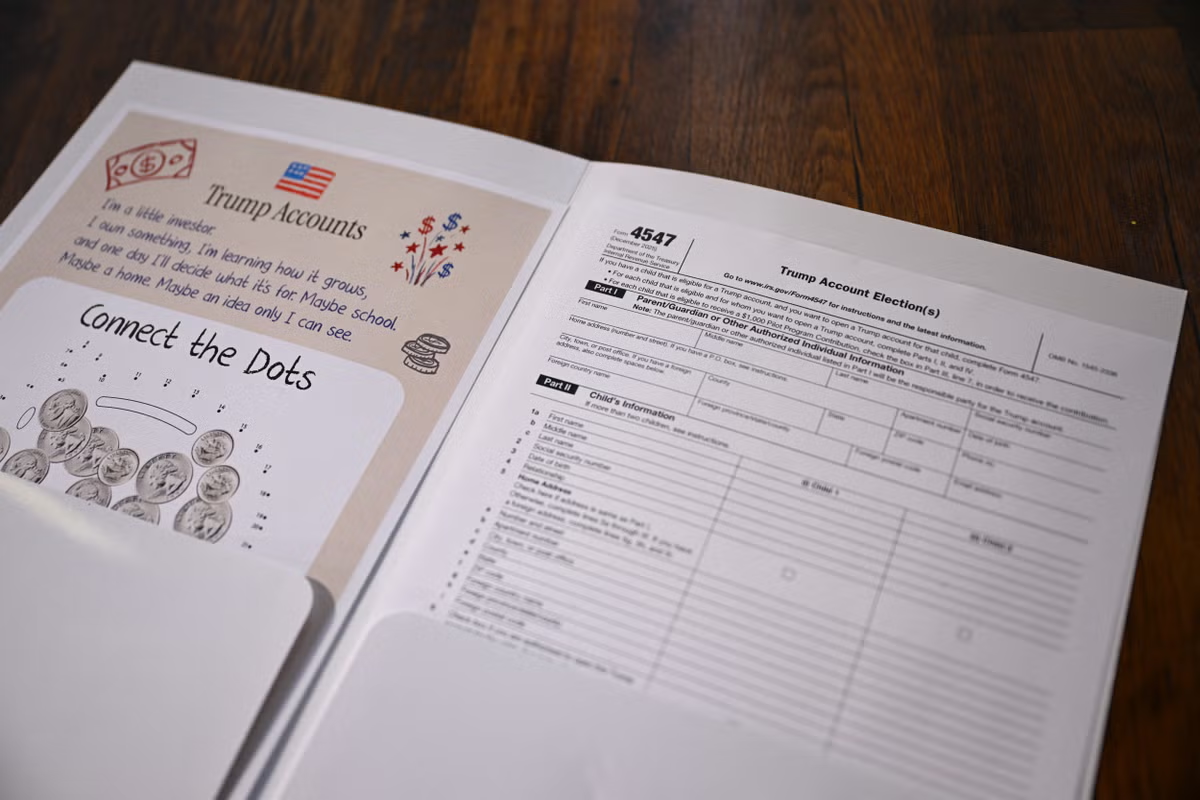

ToplineThe tax-advantaged investment funds for babies dubbed “Trump Accounts” by the administration will launch July 4 and eligible families can expect to see the initial $1,000 donation promised by the president deposited from this weekend—here’s everything we know about how the ambitious plan will work. U.S. President Donald Trump signs the One, Big Beautiful Bill Act into law on July 4, 2025 in Washington, DC.Getty ImagesKey FactsThe so-called Trump Accounts, or 530A accounts, are long-term IRA-style retirement vehicles that can be started for anyone under age 18 by an authorized adult and, when the beneficiary reaches adulthood, the account will convert into a traditional IRA.Family members, employers and other contributors can add money to Trump Accounts on behalf of children and the funds, managed by Bank of New York Mellon, will be invested in U.S. stock funds and grow tax-deferred. For babies born between 2025 and 2028, the investment account will be kickstarted by a $1,000 donation from the government and that money will be deposited (and any other investments can be made) starting July 4. Some additional children born between 2016 and 2024—who wouldn’t otherwise qualify for the $1,000 contribution from the government—will be eligible for $250 in seed money if they live in a ZIP code where the median income is $150,000 or less (which encompasses an overwhelming majority of the U.S.).After July 4, parents or other contributors can put up to $5,000 per year (collectively) in post-tax dollars into the accounts up until the year before the beneficiary turns 18. More than 6 million kids were signed up for the accounts as of early June, according to the Treasury Department, 1.5 million of which are eligible to receive the $1,000 in government seed money.BIG NUMBER14.3 million. That’s about how many babies are expected to be born in the U.S. from 2025 to 2028, meaning it will cost $14.3 billion to seed each one with a $1,000 investment. WHERE DOES THE MONEY FOR TRUMP ACCOUNTS COME FROM? The $1,000 seed deposits come from the U.S. treasury and are funded through general federal revenues. Philanthropists and more than 50 companies have increasingly pledged to fund or match donations for the accounts. Micron, SoFi, Charter Communications, BNY, BlackRock, Investment Company Institute, Robinhood and Charles Schwab, among others, have all said they will match the federal $1,000 contribution for employees’ children. Micron, a U.S. chip manufacturer, also said it will make a one-time, $250 deposit into accounts for children in counties where it operates in Idaho, New York State, Virginia, California, Colorado, Minnesota and Texas. The $250 in seed money for children in disadvantaged zip codes is being funded by a $6.25 billion pledge from billionaire tech CEO Michael Dell and his wife, Susan. Billionaire hedge fund manager Ray Dalio and his wife, Barbara, have pledged additional donations for children in Connecticut who live in lower-income zip codes, the criteria for which is met by about 87% of the state. HOW TO REGISTER FOR A TRUMP ACCOUNTParents or guardians can open accounts via IRS Form 4547 or at TrumpAccounts.gov. Families can then download a Trump Accounts app (created with help from Robinhood) to activate the account and to track and manage activity over time.HOW WILL TRUMP ACCOUNTS IMPACT THE WEALTH GAP?While the accounts will provide an investment vehicle to children who may not have otherwise had one, research shows that an expected inequality in family contributions could compound wealth disparity over time and concentrate the benefits among higher-income households. The universal $1,000 narrows the gap at the starting line, but not by much, according to the Brookings Institution. Connecticut Treasurer Erick Russell estimates a wealthy family who is able to contribute the maximum $5,000 per year could build a $150,000 nest egg by the time their child turns 30, while a child from a low-income family "is likely to be left with about $2,500." Of the people who’ve registered for the account so far, about 85% are linked to families who earn less than $200,000 annually, according to the Treasury.CRUCIAL QUOTE "Given that Trump accounts depend primarily on family and employer contributions... Many policymakers predict that these accounts will disproportionately benefit wealthy Americans," the Brookings Institution explained. KEY BACKGROUNDThe idea behind "Trump accounts" is a largely bipartisan one. Economists and lawmakers have for decades been trying to find a reasonable way to give every child a financial asset at birth, including the SEED (Saving for Education, Entrepreneurship and Downpayment) initiative of the 2000s and "Baby Bonds," the idea to give federally funded trust accounts to every newborn that was introduced in congress by several Democratic lawmakers in the 2010s and 2020s. States have their own savings programs, often linked to 529 college savings plans, but a universal national system never existed—until now. Trump's program differs from earlier proposals largely in that it does not give more benefits to poorer children and that the money will grow in the stock market as opposed to being put into a government-managed trust fund or a bond account. further readingForbesTrump Accounts Are The ‘Dirty Little Secret’ Of U.S. Retirement PolicyBy Virginia La Torre Jeker, J.D.ForbesMust Trump Account Donors File Gift Tax Returns? Here’s The IRS AnswerBy Kelly Phillips ErbForbesTrump’s Financial Disclosure: Major Crypto Moves Made Him Over $1 Billion In 2025By Antonio Pequeño IV

Everything To Know About ‘Trump Accounts’ Launching July 4

The federal government will give $1,000 in investment seed money to kids born between 2025 and 2028.

879 words~4 min read