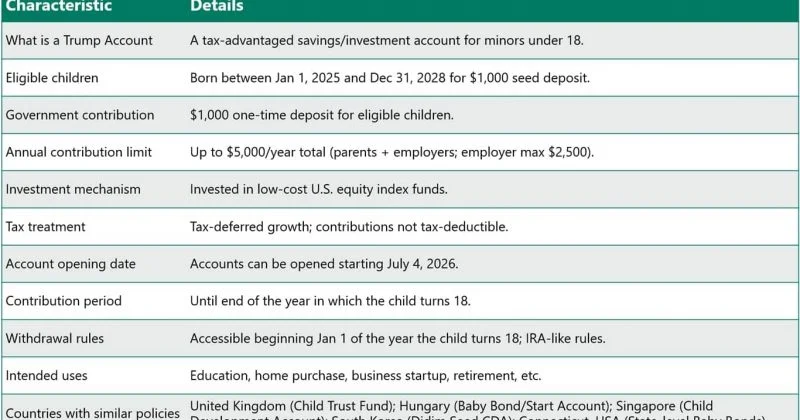

Trump Accounts, basically IRA-style investment vehicles for kids, are set to launch on Saturday — and more details are emerging about how they work.Why it matters: The accounts put a conservative spin on a progressive idea, giving kids money so that they can build wealth — think the "baby bonds" proposal of Sen. Cory Booker (D-N.J.) , but done Wall Street style. For now, the federal government is giving babies born from 2025-2028 $1,000 to seed the accounts. Some philanthropists are also kicking in donations, and some employers are teed up to contribute to their employees' accounts.The latest: On Wednesday, the Treasury Department announced that at launch, all contributions will be invested in an exchange-traded fund that tracks the S&P 500, the State Street SPDR Portfolio S&P 500 ETF.Four other ETF options are rolling out in the next few months — including another S&P 500 ETF from iShares and Vanguard's Total Stock Market ETF.These are pretty plain-vanilla, low-cost funds.How it works: Families who are eligible for the $1,000 contribution from the federal government — and have signed up for accounts — should see the money on Saturday, per a Treasury spokesperson. And they'll also be able to start contributing.Between the lines: These accounts are the latest sign of how U.S. policy has moved toward stock-market solutions for some of Americans' biggest money challenges — retirement via 401(k)s, saving for college with 529s.Catch up quick: The accounts were created last year, part of Trump's One Big, Beautiful Bill Act.The idea originated with progressive economists, as a way to close the racial wealth gap. Baby bonds, as originally conceived, were meant to be publicly funded — $50,000 seeded at birth for the poorest kids by the time they reached adulthood. Zoom in: Some proponents of the accounts now worry that they risk widening the wealth gap.The main concern is that the accounts are opt-in and that parents with higher incomes are more likely to sign up and contribute more money. "Small differences can compound into large gaps," as McKinsey lays out in a new analysis.Advocates are pushing for auto-enrollment. "We still need to figure out how to get this to be as automated as possible in order for it to have maximum reach," says Madeline Brown, a senior policy associate at the Urban Institute.Yes, but: 86% of Trump Accounts opened are linked to families who earn less than $200,000 annually, according to the Treasury's June 2026 figures, per a Treasury spokesperson.More than 50 companies have committed to making contributions for their employees — so children who aren't eligible for the federal money could still get something, the department says.The accounts will get more people invested in the stock market.For the record: "Billionaires and multinational corporations ranging from Michael Dell to Ray Dalio to Micron have pledged to donate billions of dollars of their wealth to the Trump Accounts of working-class children," White House spokesman Kush Desai tells Axios. "High-income parents have always had an array of tools to grow wealth for their kids, but Trump Accounts are giving middle-class parents the same opportunity — with billionaires chipping in to help."By the numbers: Already more than 6 million accounts have been registered — including 1.5 million who are eligible for the $1,000, according to a Treasury spokesperson.23 governors have pledged to work toward opening accounts on behalf of foster kids. What to watch: Many of these companies plan on contributing funds to accounts their employees open for their children. Details on how that would work are still forthcoming.

Trump accounts are about to launch. Here's what we know

More details are emerging about how they work.

585 words~3 min read