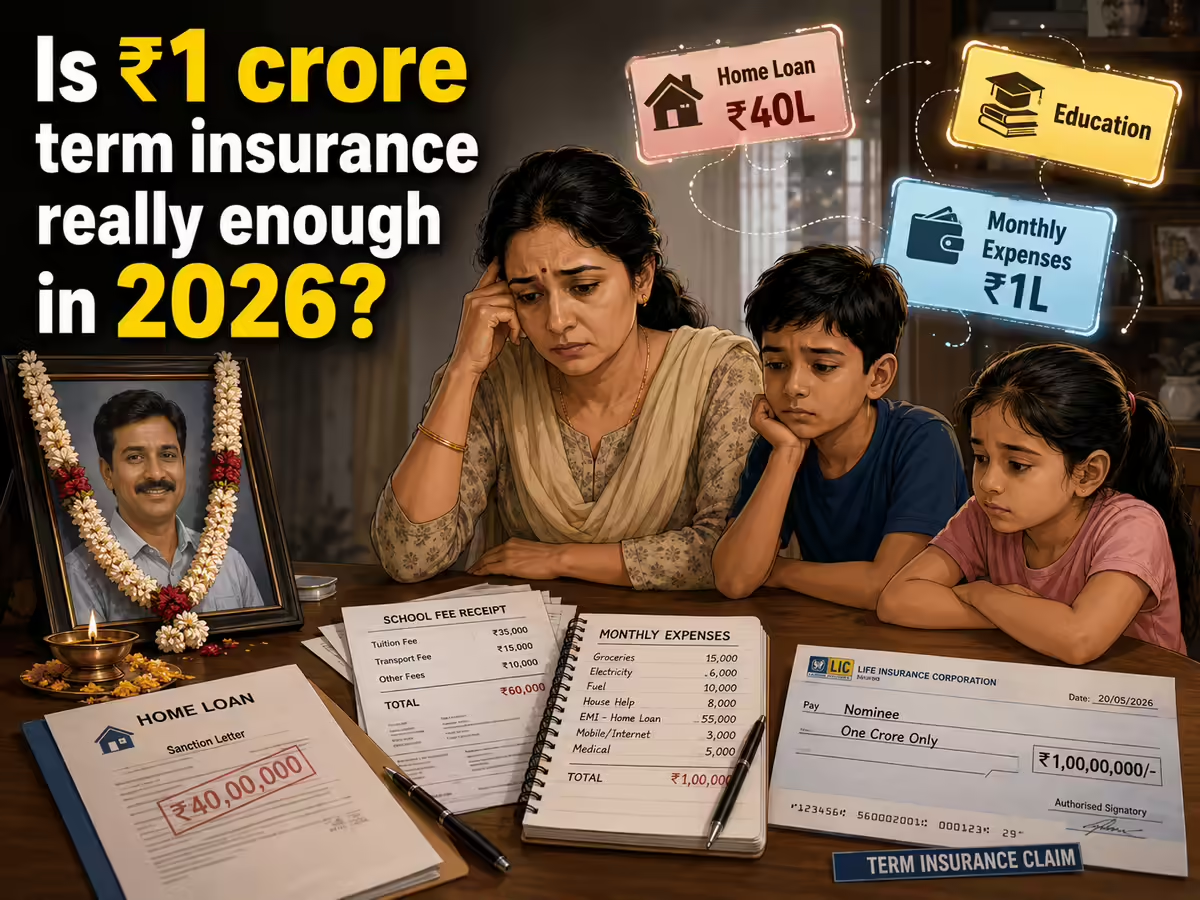

Term insurance is the most responsible financial decision a working adult can make. The real question is whether yours is doing everything it should.India's protection gap tells a sobering story. A report by the National Insurance Academy (NIA)1 found an 87% life insurance protection gap across the country and among adults in the 26-35 age group, the gap exceeds 90%. But the deeper problem is not just that too few Indians are insured. It is that they are insured for far too little. According to IRDAI2 data, life insurance penetration in India stood at just 2.7% of GDP in FY25 against a global average nearly three times higher. Against today's EMIs, rising school fees, and sustained inflation, it barely scratches the surface. The gap widens for a reason most policyholders do not think about: life changes, but policies rarely do. A 28-year-old who buys a term plan to cover a home loan, then gets married, has children, takes on a larger lifestyle, and perhaps becomes the sole earning member of an aging household, rarely revisits whether their life insurance cover has kept pace. Much of India's premium growth continues to be driven by savings-oriented products, while a significant protection gap persists despite the expansion of the life insurance market. The life insurance cover a person holds is often the cover they chose on the day they first thought about it, not the cover their family now needs. For most buyers, the answer to ‘is my life insurance cover enough?’ has been shaped by what the market historically offered, a life cover that pays out when the policyholder is no longer around. That foundation matters and always will. But a working adult today carries risks that a single payout cannot address: a serious illness that disrupts earning capacity, an income gap during a difficult year, a family that may need structured pay-outs more than a lump sum, thirty years of premiums with nothing returned if everything goes well. Life Insurance Coverage is not binary and the gap between having a term plan and having the suitable one is wider than most people realise. It is precisely this gap that Bajaj Life eTouch II has been designed to close.Where standard term plans fall shortMost basic term plans are built around one trigger: death. But financial crises rarely wait for that moment.A terminal illness diagnosis leaves a policyholder unable to work, yet premiums continue to fall due. An Accidental Total Permanent Disability (ATPD) event removes earning capacity entirely, yet most plans offer no response. These are not edge cases. They are predictable gaps in a minimum viable product and naming them clearly is the first step toward addressing them.What Bajaj Life eTouch II does differentlyBajaj Life’s eTouch II, A Non-linked Non- Participating Individual Life Insurance Term Plan is built around a straightforward idea: protection should work across a policyholder's entire life, not only at its worst moment. Here is how each feature addresses a real gap.Terminal Illness and ATPD Cover: Premium Waiver: If terminal illness or Accidental Total Permanent Disability is diagnosed, all future premiums are waived immediately and cover continues in full. A person diagnosed with a terminal illness at 42 stops receiving premium notices and his family's financial protection remains intact for the rest of the policy term.Flexible Pay-out Structure: The benefit can be received as a lump sum, as monthly income over 5 to 40 years, or as a combination of both - decided at policy inception calmly. A family where the breadwinner manages all finances is far better served by a predictable monthly income than a large one-time transfer that demands immediate financial decisions under grief.Premium Holiday Option: Policyholders can skip premium payments for 1, 2, or 3 years without the cover lapsing. For example, a self-employed professional navigating a slow business year keeps the family covered without choosing between paying premiums and cash flow.Auto Cover Continuance: If a premium is missed outside a formal holiday, life cover stays active for up to 12 months, a buffer to regularise without the protection unravelling over a short-term gap.Early Exit4 Value: If the need for cover reduce, like a loan repaid, dependents are now independent - Bajaj Life eTouch II allows an early exit4 option with a return of premiums5 paid. Someone who bought a ₹1 crore policy at 30 to cover a home loan, and clears it by 48, can exit the plan and get back the premiums they paid.Bajaj Life Care Plus Rider Non-Linked: Benefits that start from year oneThe most significant departure from conventional term thinking in Bajaj Life eTouch II is the Bajaj Life Care Plus Rider Non Linked. Available at an additional cost, the rider complements the plan’s life insurance protection with health, fitness, and wellness benefits, reflecting a broader approach to meeting consumers’ evolving protection needs. Available in five variants (Prime, Pro, Ultra, Prestige, Optima), with living benefits worth up to ₹2,00,000 per annum p.a^ At ₹ 60 per day5 for optima VariantHealth: In-clinic consultations across 1.3 lakh+ doctors and unlimited tele-consultations via video, audio, or chat, for the policyholder and family. A parent consulting a specialist from home, any time, without worrying about availability or cost, that is the annual value from a term plan, not just theoretical cover.Fitness Complimentary gym memberships across 8,100+ centres and unlimited diet and nutrition consultations.Wellness: Preventive health check-ups across 7,800+ diagnostic centres, unlimited psychologist consultations, and emotional wellness support. A policyholder who catches a metabolic condition at a routine check-up at 42 may well be preventing a cardiac event at 52.If ATPD occurs, the rider pays a lump sum, waives all future rider premiums, and every Care Plus benefit continues uninterrupted for the rest of the policy term.The right question to ask about your term planMost financially responsible Indians who hold a term plan believe the protection question has been answered. In many cases, only part of it has. The complete question is not whether cover exists but whether it holds up across illness, disability, income disruption, and a family unprepared for a lump sum. These are not exceptional scenarios. They are predictable features of a working life.The most-suited term plan is not the cheapest one. It is the one that leaves no gaps in the years between today and the future you are working to protect.Reference - https://niapune.org.in/uploads/researchreports/NIA Report 2023_Enhancing the Insurance Inclusivi ty and bridging the Portection Gap.pdfhttps://www.pib.gov.in/PressReleasePage.aspx?PRID=2254950®=3&lang=1 Please read in the full disclaimerPlease read in the full disclaimerPlease read in the full disclaimerDisclaimer: This article has been produced on behalf of Bajaj Life by Times Internet’s Spotlight team. Read the full disclaimer here.

The gap between what your term insurance covers and what your family actually needs

Term insurance is the most responsible financial decision a working adult can make. The real question is whether yours is doing everything it should.

1,098 words~5 min read