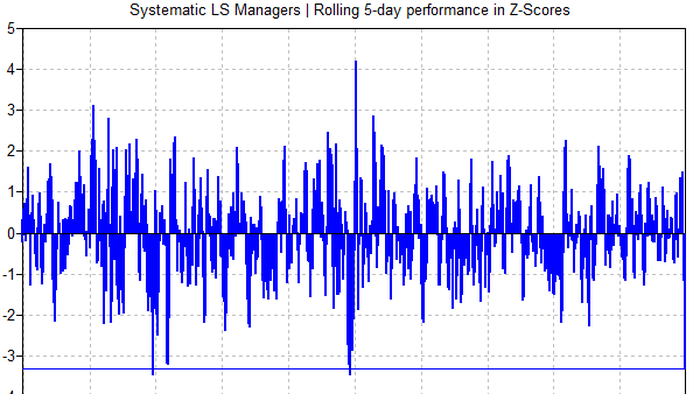

Systematic long-short equity managers, the algorithmic strategies that parse mountains of market data to find statistical edges, just posted their worst multi-day run since 2023.

According to Goldman Sachs prime brokerage data, the first half of January 2026 was the weakest period for systematic long-short equity managers since October 2025, with the cohort losing approximately 1% over a critical 10-day stretch. UBS went further, estimating that US-focused quant funds were down around 2.8% in the first two weeks of 2026 alone.

Who got hit and how hard

Renaissance Technologies saw its strategy down roughly 4% by early January. Schonfeld’s quant operation dropped approximately 3.9% through mid-month. Engineers Gate fell around 6%.

UBS identified one-day deleveraging events as a key driver, describing the unwinding as the sharpest seen since December 22, 2025.