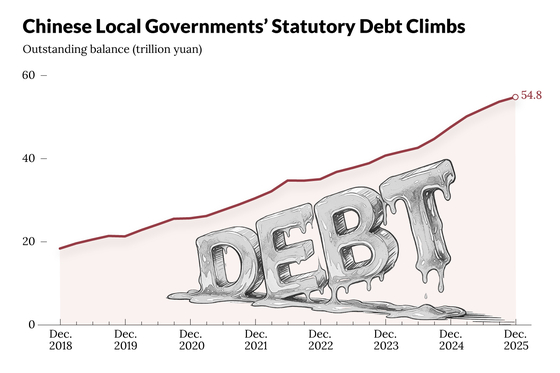

China’s financial regulators are tightening the screws on offshore borrowing, making it significantly harder for municipal-linked entities to raise money abroad. The goal: contain a growing pile of hidden debt at the local government level before it becomes something much harder to manage.

The National Development and Reform Commission, the powerful agency that oversees China’s economic planning, has stretched its approval process for offshore bond quotas from a typical 2-3 months to 5-6 months or longer.

## The LGFV problem

At the center of this regulatory clampdown are local government financing vehicles, or LGFVs. Think of them as the financial arms that Chinese municipalities use to fund infrastructure projects, from highways to housing developments. They borrow money, build things, and hope the economic returns cover the debt.

LGFV offshore issuance in 2025 totaled $40.78 billion, which sounds impressive. It was the third-highest level on record. But here’s the number that actually matters: net financing came in at negative $1.77 billion. In English: these entities paid back more than they borrowed, meaning the overall pool of available capital actually shrank.