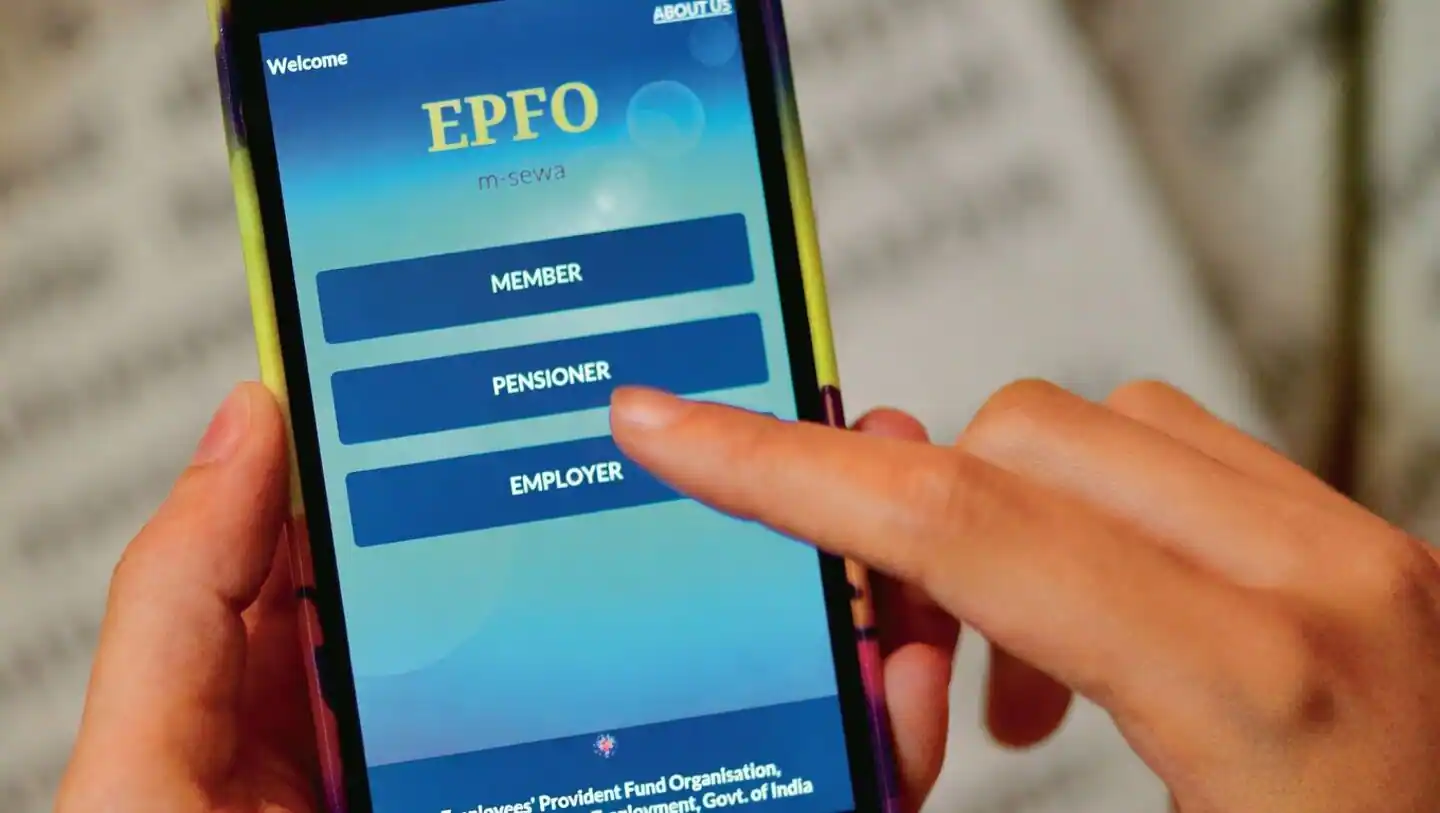

For lakhs of subscribers navigating the frustrating maze of the Employees Provident Fund Organisation (EPFO), a digital revolution has been promised. The much-awaited overhaul of the social security body—EPFO 3.0—is set to roll out to users in July. This upgrade seeks to make provident fund (PF) services faster, paperless, and more accessible for salaried employees and pensioners.But can this migration of an archaic, paper-led administrator to a digital financial services platform deliver the instant fixes it promises?What EPFO 3.0 offersEPFO has, for years, suffered from many vexing issues. Applying for PF transfer or withdrawal is often time-consuming, with subscribers facing a range of hurdles, including portal errors, record mismatches, missing contributions, non-compliant employers, and more. Subscribers often experience delays, have to visit EPFO offices, and face outright claim rejections. Filing a PF claim can feel a lot like chasing a winning lottery ticket. The 3.0 digital upgrade aims to speed up claims and simplify access to PF money through several changes.Revamped IT infrastructureOne of the biggest challenges of the organisation has been its legacy information technology (IT) backbone, which has evolved at a glacial pace over decades. EPFO has struggled to modernise a system originally designed for a paper-driven era. Data is not stored centrally; it lies fragmented across regional offices. Reconciliation of contributions, transfers, and claims is very slow because information is stored in different databases. Software systems have not been updated uniformly. Technical glitches with the EPFO portal are fairly common.With EPFO 3.0, the PF body is moving away from its older, fragmented IT architecture towards a more integrated platform. Under the Centralised IT Enabled System (CITES), EPFO will adopt a unified, centralised, and highly automated system. “The new system will unify the back-end for employers and regional PF offices, which earlier operated in silos,” indicates Ketan Das, Manager–Operations and Strategy, FinRight Technologies, a platform that assists in resolving PF-related issues.The broad idea is to make EPFO function closer to a modern banking platform. This will reduce dependency on regional EPFO offices for routine approvals. It will afford a single view of member accounts, contributions, claims, transfers and pension-related records. For members relocating to different cities and jobs, this could remove location-based hurdles in processing PF transfer or withdrawal claims. It will enable faster transaction processing and better integration across banks and payment systems. Simplifying internal administrative tasks will also allow for smoother handling of grievances. Complaints and service requests may be handled from any EPFO office, regardless of where the account was originally registered.A re-engineered electronic challan-cum-return (ECR) has already been rolled out for employers, providing a streamlined four-step workflow to upload returns, validate data, generate challan and make payments. This will improve employer compliance and drastically reduce errors in submissions and claim rejections.To be sure, every EPFO office has also transitioned to the Centralised Pension Payment System (CPPS)—a new disbursal system to accelerate pension delivery. It allows pensioners to receive seamless, timely credits directly into their bank accounts or Aadhaar-linked accounts from any branch, anywhere in the country. EPFO has also tied up with the India Post Payments Bank (IPPB) to provide doorstep digital life certificate (DLC) services to EPS-95 pensioners. Earlier, pensioners needed to physically submit life certificates to continue receiving benefits.Instant, automated withdrawalsOne of the biggest provisions in EPFO 3.0 pertains to how employees access their PF. Starting next month, the portal will allow subscribers to withdraw money from the PF instantly via Unified Payments Interface (UPI) apps and UPI-enabled ATMs. This money will be directly credited to the member’s linked bank account. This facility will be offered through EPFO’s integration with the National Payments Corporation of India (NPCI) network. Initially, a limit of Rs.25,000- 50,000 per transaction may be put on such withdrawals.For UPI withdrawals, Aadhaar OTP-based authentication will enable instant claim processing. For ATM withdrawals, EPFO will issue a PF-linked ATM card to its members, which would function like a debit card and allow subscribers to withdraw eligible PF funds directly from UPIlinked ATMs. To access these withdrawals, members must be know your customer (KYC)-compliant, have an active Universal Account Number (UAN), an active mobile number linked to the UAN, and Aadhaar and a Permanent Account Number (PAN) linked to the UAN. Members must note that the introduction of UPI-based withdrawals will not alter the existing tax provisions on EPF interest income.However, some reckon UPI-based withdrawals is not as useful as it is being made out to be. “The only problem this solves is not having to wait three days for partial withdrawals, which technically could have been solved in the current system as well. Linked bank accounts shouldn’t take 3-7 days in processing such transfers,” reckons Kunal Kabra, Founder, Kustodian.Life, another platform that helps with stuck PF claims.To allow quicker access, EPFO 3.0 had already enabled auto-settlement of claims up to Rs.5 lakh for KYC-compliant accounts, with fast-track disbursal within 72 hours. Initially introduced for payouts up to Rs.1 lakh, EPFO increased the auto-settlement threshold from Rs.1 lakh to Rs.5 lakh in June 2025. This provision seeks to reduce dependence on employer approvals and manual form submissions, cutting turnaround time for claims. This automated settlement has also been integrated into PF account transfers. During financial year 2025-26, the auto-settlement mode had already processed over 3.5 crore claims for amounts up to Rs.5 lakh as of February 25, 2026, according to the Ministry of Labour and Employment.However, withdrawals exceeding Rs.5 lakh will continue to undergo full verification, including employer approvals and manual intervention. Kabra remarks, “Full withdrawals will continue to face challenges. In partial withdrawals, data mismatches are not checked. But full withdrawals will be subjected to the gamut of checks, so members must go through the entire loop of approvals, verifications and corrections.”How to get ready for EPFO 3.0To avail of EPFO’s new digital services, members can take the following steps now:Link Aadhaar with your EPFO account.Link your bank account on the EPFO member portal.Check that your name, date of birth, and other details match across your Aadhaar, PAN, and EPFO records.Confirm UPI ID corresponds to the EPFO-linked bank account.Register on DigiLocker to access PF-related documents.Correct any profile discrepancies to prevent delays when the new system goes live.What EPFO 3.0 must solveOutdated technology architectureData fragmentation across regional PF offices leads to slow reconciliation of contributions, transfers and claims.Lack of UAN level accountingWithdrawals/transfers are done on different member IDs even when mapped under a single UAN.Slow, inconsistent claim settlementManual interventions required despite digital submission; member experience differs as per the regional PF office.Employer-dependent processesMany corrections still require employer approval, a digital signature, clarification letters, or physical documents.Offline processesPhysical visits to regional PF offices are required in certain cases, such as death claims, old PF accounts (pre-UAN era) withdrawal/transfer, and EPS corrections.Employer compliance challengesDelayed or missing deposits, incorrect wage reporting, and non-cooperation by exemployers.Data quality issuesMismatch or gap in records leads to withdrawal rejections (multiple PF accounts not merged, name mismatch, incorrect date of birth, wrong joining/exit date, etc).EPS-related complexitiesIncorrect EPS deductions, wrong EPS date of joining/date of exit, and previous service clarification issues frequently create complications.Grievance redressal problemsDelayed resolution, closure without complete resolution (reasons often not specified), repeated followups required.Simplified, flexible withdrawalAs part of EPFO 3.0, the PF body has streamlined its withdrawal rules. Earlier, members making withdrawal claims faced varying eligibility conditions and caps across thirteen different withdrawal reasons.Under the revised framework, these are merged into three broad buckets: essential needs, housing needs, and special circumstances. The minimum eligible service period is uniformly set at 12 months for all types of partial withdrawals. In the ‘special circumstances’ category, members are now allowed withdrawals without providing any specific reason. Earlier, claims under this head required documentary proof, such as for ‘natural calamities’, ‘unemployment’, or ‘other emergencies’.Members will now be allowed to withdraw up to 75% of their PF balance, including both employee and employer contributions, depending on the type of claim. This limit also applies to UPI-based withdrawals. At least 25% of the corpus must be retained to protect long-term retirement savings. Members can now apply for final PF settlement only after 12 months of leaving employment, up from two months previously.Even as access to money improves, investors must be mindful of the tax implications of premature PF withdrawals. Das remarks, “Earlier, large withdrawals could be done after five years of contributions, making the amount tax exempt. But with the eligibility being dropped to 12 months under the new rules, the withdrawals could become taxable.” Premature withdrawals may still qualify for tax exemption in certain circumstances, including medical emergency or job termination.Correcting records digitallyGaps or inaccurate data in members’ profiles are among the biggest reasons for PF claim rejections. Data corrections largely required manual intervention. EPFO 3.0 plans to make record corrections more digital and less employer-dependent. Members can make corrections to their PF account on their own via OTP verification. Those who have faced claim rejections due to data mismatches can now resolve these issues digitally, without office visits. Some changes have already been introduced on this front. Members can currently update information such as name, date of birth, and marital status directly. Between January and December 2025, 32.23 lakh profile corrections were processed through this facility.Members will be able to make additional corrections under EPFO 3.0 without requiring employer approvals. But some corrections may still require verification by the employer or EPFO, depending on the type of change. “Many corrections still require employer approval, digital signature, clarification letters, or physical documents. This causes major delays when employers are unresponsive, shut down, or unwilling to cooperate,” Das points out.No magic wandOver 30 crore EPFO subscribers are hopeful that this digital overhaul will bring much-needed relief from tedious processes, slow moving machinery and administrative gaps. EPFO’s apparatus has largely been archaic so far, whereas the banking and investment landscape has modernised and marched ahead. Modernising this lethargic administrative body is essential to handle the next wave of workers entering India’s social security net. EPFO 3.0 is an attempt to rebuild the PF body around this new reality.But a single sweeping overhaul is unlikely to fully address the multiple ailments of EPFO. Some issues are particularly vexing; there are no quick fixes for these. “A new era for social security is being promised, but don’t expect all problems to suddenly go away,” cautions Das. Particularly, those with higher PF balances may not enjoy the same benefits and still must go through the rigmarole of approvals and verifications. There is also no easy fix for the recurring problem of gaps or mismatches in KYC records.Several features of EPFO 3.0 have been announced or approved. Many of these are likely to be implemented in phases. There is no clarity on when these facilities will go live and in what order. Many operational details are also not yet spelt out. Kabra warns that EPFO’s transformation will not happen overnight; rather, it will be implemented in phases. EPFO’s database has accumulated decades of records, creating a huge data-cleaning challenge. “Transitions of this nature, involving legacy systems with crores of data points, cannot be implemented in a hurry because of the sheer scale,” Kabra asserts. A few hiccups in the promised delivery of services can be expected during this transition.To be sure, EPFO has made some initial progress in its digital facelift. The downtime in its portal has reduced, while claim rejections have declined to some extent.But for the organisation to truly function like a modern bank—with quick, easy access to PF money and services with minimal intervention—it requires a monumental rebuild. As the rollout unfolds, it remains to be seen if EPFO can deliver on its promises.

EPFO 3.0 promises a digital PF experience, but can it fix years of legacy problems? - The Economic Times

EPFO 3.0 aims to modernize provident fund services through upgraded technology, faster claim processing, simplified withdrawals, digital record corrections and improved user access. While these reforms promise greater convenience, longstanding issues such as data quality, employer dependence, pension complexities and grievance resolution remain challenges that will require sustained implementation efforts.

1,930 words~9 min read