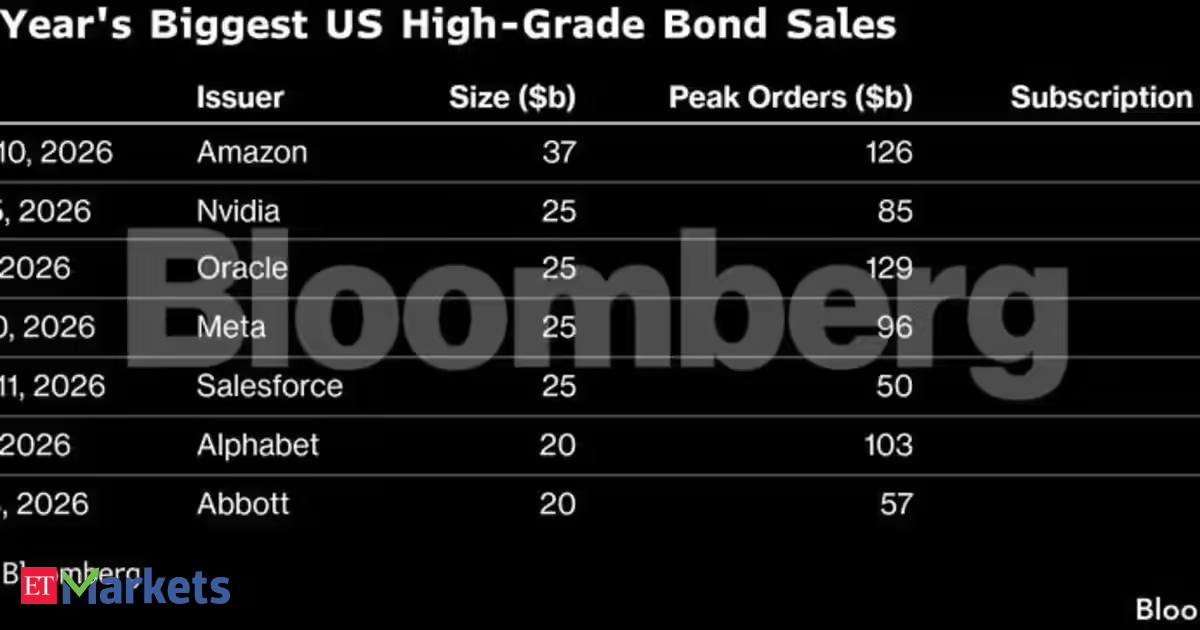

SpaceX completed a roughly $86 billion IPO in early June 2026, sat on more than $100 billion in cash, and then went back to investors asking for $25 billion more in bonds. The response from markets: an overwhelming yes, backed by nearly $90 billion in orders.

That kind of demand would normally be cause for celebration. For Ludovic Subran, the chief investment officer at Allianz, it was cause for alarm.

When the market says yes to everything

Subran spoke at the FT Global Insurance Summit and did not mince words. His assessment of the SpaceX bond deal: it signals that markets have entered bubble territory. His colorful summary of what Elon Musk walked away with: “$70 billion of funny money.”

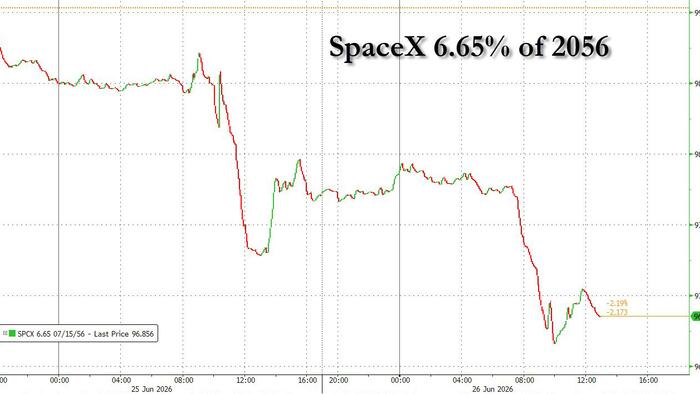

SpaceX disclosed approximately $100.8 billion in cash at the time it announced the bond offering. The bond offering was initially sized at $20 billion. Demand came in so hot that the deal was upsized to $25 billion, structured across five tranches of senior unsecured notes with maturities running from 2031 to 2056. The notes carry investment-grade ratings. Proceeds are earmarked primarily for refinancing existing bridge debt and supporting general corporate activities, including the buildout of AI infrastructure connected to SpaceX’s merger with xAI.