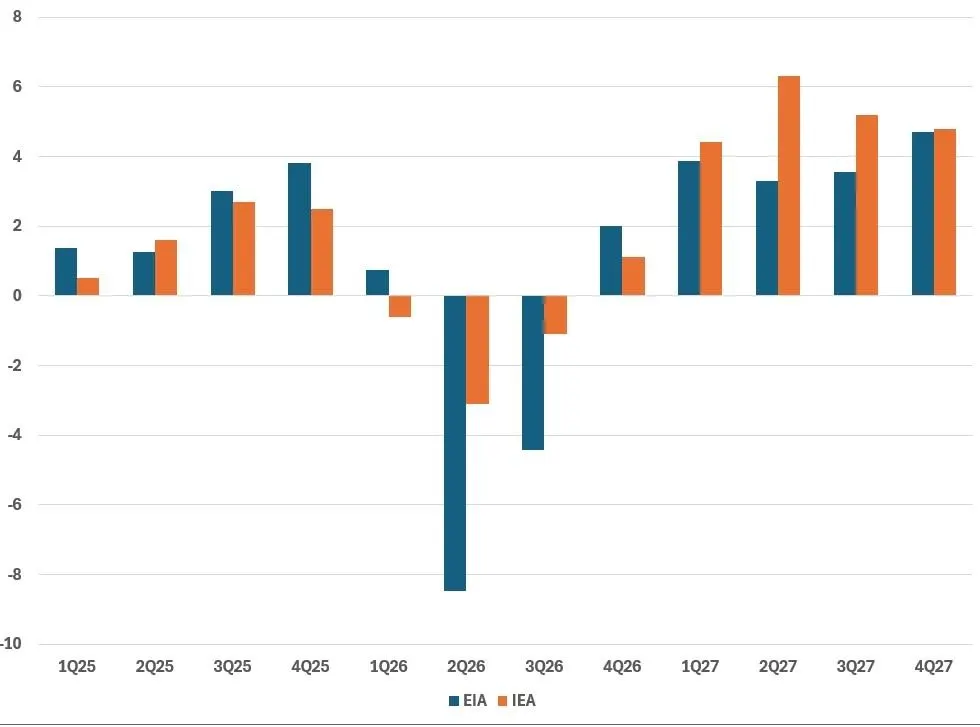

A growing consensus has emerged among major oil market forecasters that today's supply shock will eventually give way to tomorrow's surplus. Energy Intelligence projects the global market will swing from a 3.1 million barrel per day deficit in 2026 to a roughly 4 million b/d surplus in 2027, while the International Energy Agency and US Energy Information Administration (EIA) expect supply to exceed demand next year by 5 million b/d and 3.9 million b/d, respectively, as Mideast oil flows normalize following the recent US-Iran interim peace deal. Yet the narrative of an inevitable glut may be arriving before many underlying market uncertainties have been resolved. The most immediate question is whether Mideast supply and trade flows normalize as smoothly as current balances assume. Much of the surplus story depends on the rapid restoration of Gulf exports, which hinges on the uninterrupted reopening of the Strait of Hormuz. For now, traders appear bullish about a rapid restoration, emboldened by rising trans-Hormuz flows over recent days, but physical and logistical realities suggest the process could face obstacles. Shipping experts say trapped laden tankers and ballast vessels behind the strait could take six to eight weeks to clear bottlenecks, while redeploying vessels back to the Gulf could require up to two months. Even after ships are loaded, voyages to key Asian destinations can take up to 25 days. The restoration of shut-in Mideast production is also unlikely to be uniform. Kuwait Petroleum Corp. CEO Sheikh Nawaf al-Sabah says most producers in the region could restore roughly 80% of shut-in production within weeks, but the remaining 20% could require three to four months. S&P Global analysts do not foresee a full restoration of shut-in volumes until 2027.

Oil 'Surplus' Narrative Hinges on Many Unknowns

Consensus forecasts of a supposedly inevitable oil glut in 2027 may be emerging before many underlying market uncertainties have been resolved.

283 words~1 min read