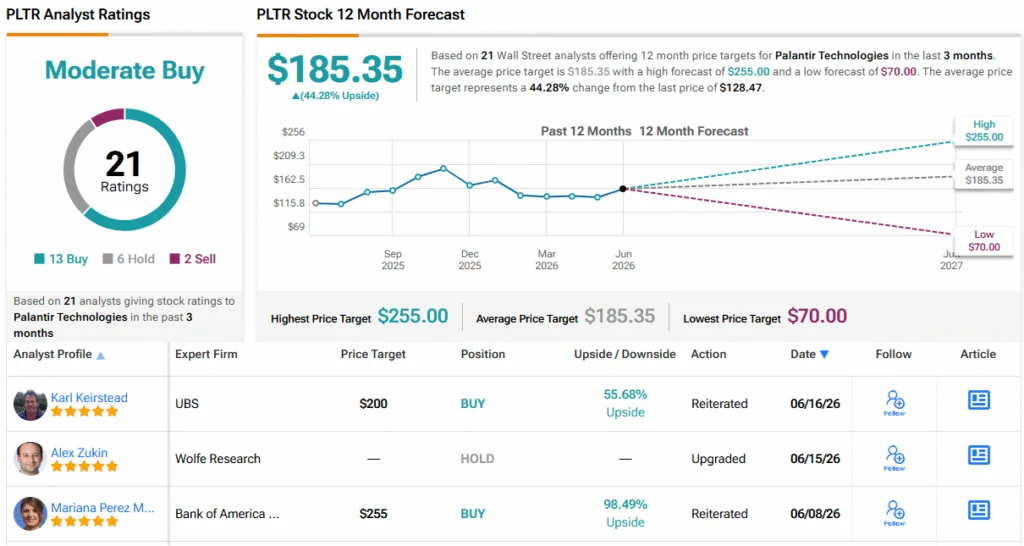

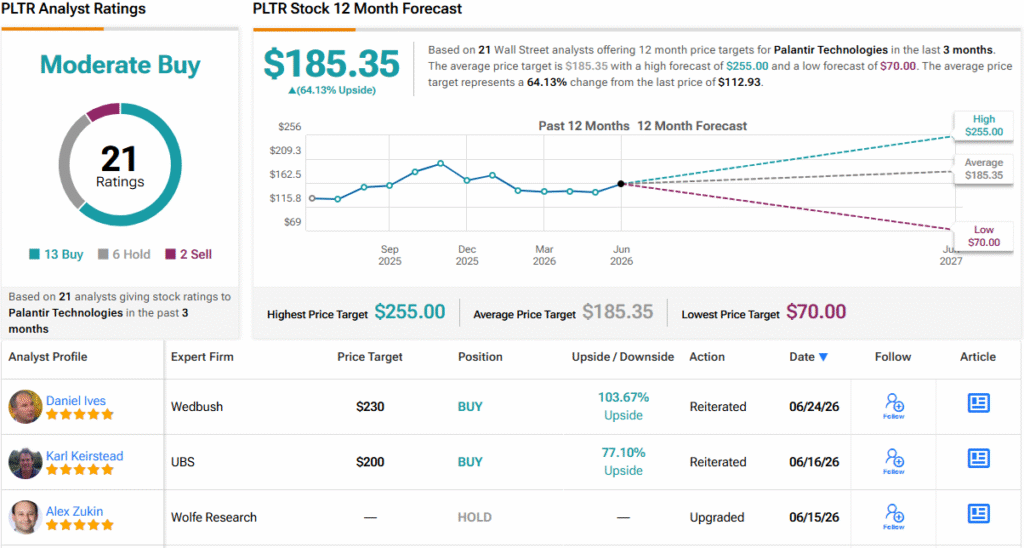

Aggressive Valuation CompressionDespite delivering an 85% year-over-year revenue spike to $1.63 billion in the first quarter of 2026, investors are scaling back Palantir’s premium multiple. The equity maintains an elevated trailing price-to-earnings (P/E) ratio exceeding 121 times.This adjustment follows a broader technology selloff initiated earlier in the week by double-digit declines in South Korean memory-chip manufacturers, which triggered a widespread reassessment of richly valued artificial intelligence software names.Competitive Headwinds From AnthropicHeightened enterprise adoption of Anthropic’s AI solutions adds further pressure to the stock. In an April 8, post on X, prominent short-seller Michael Burry stated that “Anthropic is eating $PLTR Palantir’s lunch,” citing data from Ramp’s March AI Index.According to Ramp, Anthropic secures roughly 70% of first-time, head-to-head enterprise purchasing decisions against OpenAI. Burry, who holds long-dated 2027 put options against Palantir, argued that Anthropic’s rapid scaling outpaces Palantir’s traditional software deployment timeline.Shifting Enterprise AI Procurement ModelsAnthropic’s transition toward usage-based, pay-as-you-go pricing, initially reported by The Information in April, alters corporate AI spending dynamics.The flexible consumption structure allows businesses to deploy tools instantly via APIs, contrasting with the longer sales cycles and heavier integration requirements characteristic of Palantir’s platform.Palantir CEO Alex Karp countered this narrative at a recent customer event, noting that direct reliance on large language models creates cost control issues for enterprises.Sustained Financial ExecutionThe downward price action contrasts with Palantir’s raised full-year 2026 guidance issued on May 4. Management increased its annual revenue forecast to between $7.65 billion and $7.66 billion, up from prior expectations.On Tuesday, Burry highlighted that Palantir’s volume “fell into the top and still has not recovered as it falls,” signaling a continuing technical downtrend as the market re-rates software multiples.Technical AnalysisPLTR is in a clear longer-term downtrend, trading 18.9% below its 20-day SMA, 20.9% below its 50-day SMA, 22.8% below its 100-day SMA, and 31.8% below its 200-day SMA. The 20-day SMA is below the 50-day SMA, and the death cross (50-day below the 200-day. Momentum is stretched: RSI is 28.12.

Why Is Palantir Stock Falling On Thursday? - Palantir Technologies (NASDAQ:PLTR)

Palantir plunges into deeply oversold territory, trading 31% below its 200-day SMA. Check out the key support and resistance levels now.

359 words~2 min read