That doesn’t seem to be the case with Palantir. The company continues to deliver better than solid numbers, along with bullish projections. Its last Rule of 40 score was 145%, which in the words of CEO Alex Karp, “shattered the metric.”

Going forward, Palantir raised its full-year 2026 guidance for revenue to $7.65–$7.662 billion, which implies ~71% year‑over‑year growth. PLTR’s share price has dropped by 12% since its earnings report a little over a month ago.

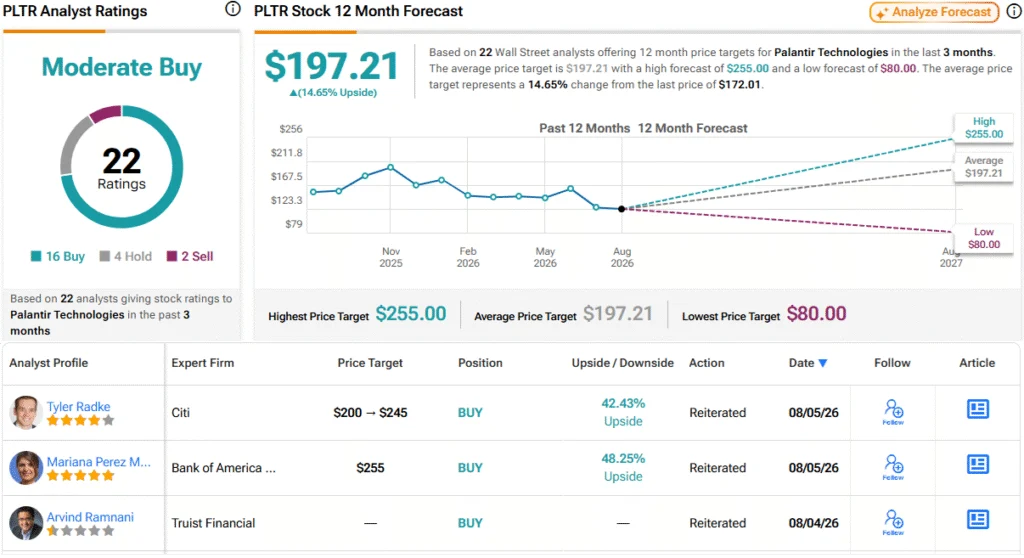

What’s going on? That would be the company’s high-flying valuation, which even after the dip still trades at an elevated price-to-earnings multiple of 135x. Is this an opportunity to go bargain hunting for a company delivering stellar growth?

Top investor Keithen Drury isn’t so sure.

“I think there’s one metric that tells the truth, and it’s a harsh reality,” states the 5-star investor, who is among the top 4% of stock pros covered by TipRanks and a writer for The Motley Fool.