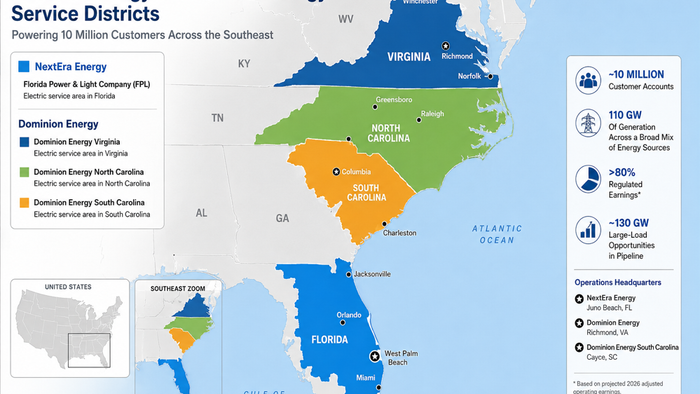

Andrea Sguazzi is Head of Venture Builder & Startup Programs at Mind the Bridge, working with corporates and startups on open innovation.gettyThe proposed NextEra Energy–Dominion Energy merger is already being interpreted as a data center power play. Financial Times described the transaction as a “mega-merger” tied to the AI infrastructure boom, with Dominion’s strategic value rooted in its position as the primary power supplier to Northern Virginia’s “Data Center Alley,” one of the world’s largest concentrations of data centers.The numbers help explain the scale of this “Alley.” Northern Virginia hosts hundreds of operational data centers, while the U.S. Energy Information Administration reports that Virginia’s commercial electricity sales increased by nearly 30 million MWh between 2019 and 2025, driven largely by data centers. PJM expects Dominion’s zone to experience the largest absolute increase in summer peak demand across the PJM footprint between 2026 and 2030.Despite sitting at the center of one of the world’s fastest-growing electricity markets, Dominion struggled for years with lagging stock performance. Markets may not simply reward utilities exposed to electricity demand growth, but rather those capable of executing projects at unprecedented scale and complexity.NextEra’s own investor materials make that point explicit. In a May presentation tied to the merger announcement, the company argued that projects required to serve modern data center hubs are becoming dramatically larger and more capital-intensive—roughly 5 GW and $15 billion in capital expenditure—than the renewable and storage projects that defined the last decade, which typically averaged around 200 MW and $0.5 billion. The conclusion of the slide was blunt: “Scale and a strong balance sheet matter more than ever.”That framing shifts the discussion away from generic electricity demand growth and toward infrastructure execution. AI infrastructure is not creating ordinary load growth. It is creating industrial-scale infrastructure requirements that combine generation, storage, transmission, interconnection, cooling, land development and financing into highly complex project ecosystems.When Speed Becomes More Valuable Than CapacityInterconnection delays measured in years are increasingly incompatible with AI infrastructure economics. In a market where compute deployment speed directly affects competitiveness, compressing infrastructure timelines becomes economically strategic. As Crusoe’s recent AI Infrastructure Trends Report argues, speed-to-market is becoming strategically critical. Data center developers are, therefore, increasingly exploring alternative deployment architectures, including flexible interconnection models, vertically integrated infrastructure and “bring your own power” strategies.A recent study by Camus, encoord and Princeton ZERO Lab, funded by Google, found that flexible grid connections combined with bring-your-own capacity could accelerate data center interconnection timelines by three to five years.In other words, when conventional infrastructure deployment becomes too slow, the market starts reorganizing around faster execution pathways.The Startups Building Around The BottleneckThe consequences of this shift were among the dominant themes at this year’s San Francisco Climate Week, where powering AI infrastructure became a central topic of discussion. A panel hosted by Mind the Bridge featuring hyperscalers, startups and utilities offered concrete examples of how startups are already benefiting from this shift.Noon Energy announced an agreement with Meta involving 100 GWh of planned long-duration energy storage capacity, including an initial 2.5 GWh deployment targeted for 2028. Silicon Valley Power separately launched a pilot with Emerald AI focused on flexible data center power management and grid integration.Meanwhile, Heron Power raised $140 million earlier this year to scale production of solid-state transformers designed specifically to address growing grid bottlenecks linked to AI data center electrification.But perhaps the clearest example of the shift is Crusoe.Originally focused on using stranded energy assets to power bitcoin mining, Crusoe has transformed itself into one of the fastest-growing AI infrastructure companies in the market. The company vertically integrates energy sourcing, AI-optimized data-center construction and cloud services, a model that helped it raise a $1.375 billion Series E round in 2025 at a valuation exceeding $10 billion. Today, Crusoe brands itself as "the AI factory company."What makes Crusoe particularly interesting is not simply its growth trajectory, but the underlying logic of its model. The company effectively positioned itself around the same bottleneck emerging from the NextEra–Dominion transaction: the growing need to deploy increasingly complex AI infrastructure systems quickly, reliably and at enormous scale.What Business Leaders Should Watch NextFor business leaders, the key lesson is that AI infrastructure constraints are no longer just a utility-sector issue. Access to power, speed of deployment and infrastructure execution are becoming strategic variables that can influence where AI workloads are built, how quickly new capacity comes online and which companies capture value across the emerging AI ecosystem.AI may ultimately reshape the energy sector less through sheer demand growth than through the execution requirements it imposes. Utilities with the scale, financing capacity and operational capability to deliver increasingly complex infrastructure projects may emerge stronger. Energy startups capable of embedding themselves into hyperscaler-driven infrastructure ecosystems may gain dramatically faster commercialization pathways than those relying exclusively on traditional utility procurement cycles.Beyond economic and technological considerations, growing political debate and local community opposition add an entirely different layer of uncertainty to the already herculean challenge of infrastructure deployment. Forbes Technology Council is an invitation-only community for world-class CIOs, CTOs and technology executives. Do I qualify?

How AI Is Picking Winners And Losers In The Energy Space

AI may ultimately reshape the energy sector less through sheer demand growth than through the execution requirements it imposes.

839 words~4 min read