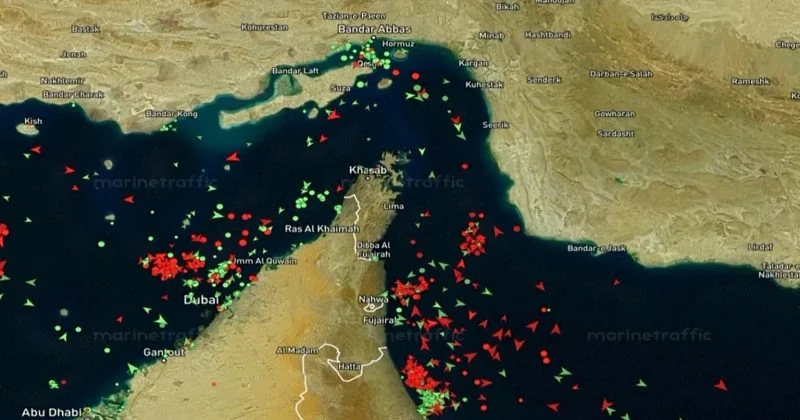

This week the US and Iran signed a memorandum of understanding to end their confrontation. The blockade of Iranian ports is expected to be lifted, the Strait of Hormuz is expected to reopen within days and Qatar has already begun moving its tankers back towards Ras Laffan. The immediate reaction across energy markets in the coming days will be relief. Prices will ease, cargoes will move and the headlines will turn to other things. A familiar conclusion will form quickly: the crisis has passed and gas markets can go back to normal.That conclusion would be a mistake, and we have already seen why. A ceasefire in April reopened the strait for a matter of days before it closed again. Anyone treating this reopening as the end of the story has a short memory.Shocks like this do not simply pass through a market and leave it unchanged. They reshape it. What looks on the surface like a temporary disruption is in truth a turning point, and it is forcing the LNG industry to rethink what it had assumed about security, strategy and risk.Play01:25Gulf LNG carriers to end long wait to cross Strait of HormuzThe past months made the point plainly. A shipping lane barely three kilometres wide at its narrowest has been enough to choke off close to a fifth of the world's liquefied natural gas. Qatar, one of the largest exporters in the world, has been unable to ship at anything near capacity. Buyers from Asia to Europe have chased replacement cargoes at rising prices, and the cost has been felt well beyond the trading floor, in household bills, in schools and offices, in factories, and in the wider economy.When flows resume, some of that pressure will lift. The premium attached to the blockage will fade. But the deeper change will stay because markets do not forget a scare like this one. What has been exposed, and not for the first time, is a flawed assumption: that security of supply could be taken for granted.For decades, the LNG business has been shaped above all by economics, by the pursuit of lower cost, long contracts and predictable cycles. That era is closing. Geopolitics now matters as much as geology, and resilience is displacing efficiency as the industry's organising principle.Every serious buyer has learnt a lesson they will not unlearn: supply that looks secure can vanish overnight, for reasons that have nothing to do with price or capacity. A 20-year contract is only as good as the route it travels down. That realisation will shape decisions long after the tankers are moving freely again.Three things follow. The first is confidence. Security of supply, until recently a background assumption, is now a question for the boardroom. Buyers will pay for resilience in ways that never show up in the headline price, through more diversified sourcing, more storage and firmer contract terms. The risk premium this episode has created does not vanish when the crisis ends. It settles into the way the market is built.The second is that the wave of new supply the market was counting on may not arrive as expected. Much of the capacity meant to rebalance the market is tied, one way or another, to regions now carrying real geopolitical risk, and the delays are measured in years, not weeks. The long-predicted glut may still come, but later, and into a market that has changed in the meantime. Expectations of abundance are giving way to a need for patience.The third, and least visible, is that the system that used to absorb shocks is fraying. Markets are growing more volatile, not less. Producer discipline is weakening, and because so much gas is still priced against oil, trouble in one market feeds straight into the other. The result is a less predictable pricing environment, one that makes it harder to finance the long-term projects on which both energy security and the energy transition depend.None of this calls for waiting until things settle down, because what counts as settled has itself changed. It calls for clear eyes. The firms that come through this well will be the ones that build flexibility into how and where they buy and accept that resilience carries a cost. At a time when gas is already competing hard with other fuels, holding the balance between security and cost will be one of the defining commercial challenges of the coming decade.Nowhere will this matter more than in the Gulf, which sits at the centre of global supply and is now being judged on more than price and volume. Buyers want reliability and assurance in a world that feels less certain. For Qatar, the task is to rebuild not just capacity but trust. For the UAE, the opportunity is to move quickly and make resilience part of what it offers. How the region responds will shape the next phase of the market.None of this is cause for gloom. It is a call for realism. The industry has crossed a line. The assumptions that carried it for years, that supply would be predictable and that economics would settle everything, are giving way to something more complicated.So when the ships return to Hormuz, the relief will be real and well earned. It should not be mistaken for a return to normal. The visible crisis will recede on cue. The quieter changes – lost confidence, delayed supply and a market reorganising itself around resilience – will not. The companies and countries that see this and act on it will shape what comes next. Those that do not may find that the real disruption is only beginning.

The Strait of Hormuz will soon be open for business again – but business will never be the same again | The National

The real test for the gas markets begins only after one of the world's busiest chokepoints reopens

TL;DRAI

US-Iran deal reopens Hormuz; the 20% blockade of global LNG ends as Qatar resumes shipping. Geopolitical risk now drives supply strategy: buyers demand diversified sourcing and resilience, permanently displacing cost efficiency as the market's organizing principle.

933 words~4 min read