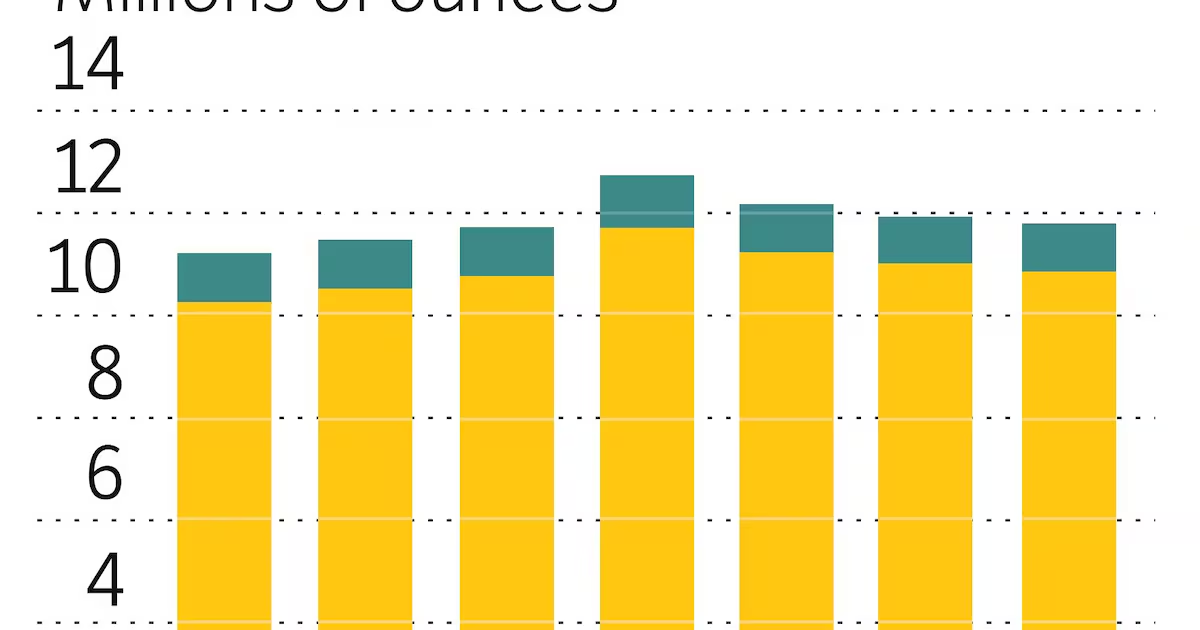

South Africa’s mining sector, particularly its dominant platinum group metals (PGMs) industry, possesses immense potential, as illustrated by its resilience and contribution to the national economy in 2025. However, this potential is significantly undermined by a persistent disconnect between bureaucratic policy and market realities. Capital investment, crucial for a sector defined by deep, labour-intensive operations and rising energy costs, hinges not only on geological endowment but critically on policy certainty and price stability. South Africa’s PGM operations face structural challenges, including high operating costs and logistical bottlenecks. While these are inherent to the industry, policy instability is a manageable factor that, if addressed, could mitigate the impact of price volatility and ensure attractive returns on investment. PGMs remain indispensable, with South Africa supplying 71% of the primary global output. This geographic concentration offers a unique opportunity for industrial growth through vertical integration in upstream and midstream markets. Furthermore, the PGM recycling business is a rapidly expanding segment, driven by increasing recovery from end-of-life autocatalysts and electric waste.In 2024 nearly 120,000kg of combined palladium and platinum were recycled. However, primary mining continues to form the bedrock of global supply, especially for high-grade ore deposits essential for burgeoning demand from hydrogen technologies and advanced electronics. The global PGM market is moderately consolidated, with big producers such as Valterra Platinum, Norilsk Nickel, Impala Platinum Holdings, Sibanye-Stillwater and Northam Platinum dominating primary output. These firms are increasingly pursuing vertical integration to enhance efficiency and profitability across mining, smelting, refining and recycling. Commodity markets, as reflected by the London Metal Exchange, react swiftly to geopolitical shifts and supply-demand dynamics and not to governmental timelines. While South African PGMs have historically shown a strong balance due to demand, despite high all-in sustaining costs from energy, labour and transportation, recent price volatility has been extreme. Furthermore, average primary platinum all-in sustaining costs are forecast to increase 7.7% to $1,006.14/oz in 2026. For instance, PGM pricing in 2025 saw platinum hover around $900-1,000/oz in late 2024 before spiking to $1,600/oz in Q2 2025. Palladium traded at $1,000 for most of the year, rising to $1,200 after June 2025, and rhodium recovered to $7,000/oz from $4,000-5,000/oz. These surges were influenced by increased demand from EV ambitions, hybrid cars, and jewellery, particularly in China and India, where platinum substitutes gold. In addition, output cuts and restructuring by South African producers contributed to a global supply shortage, given the country’s prominence. The World Platinum Investment Council forecasts a 4% decline in global growth for 2025, leading to a platinum supply deficit of 966,000 ounces. Beyond domestic challenges, geopolitical tensions, notably involving Iran and Russia, introduce inventory instability and long-term supply uncertainty. These factors collectively hinder the market’s ability to scale supply in line with growing demand. The extreme price volatility poses a big structural challenge for downstream industries and upstream project developers. Palladium, for example, surged past $3,400/oz after Russia’s invasion of Ukraine, only to decline by nearly 37% shortly thereafter. Similarly, rhodium plummeted from its 2021 peak of almost $30,000/oz to about $4,365/oz by February 2024. Such instability erodes confidence in long-term offtake agreements, particularly for capital-intensive hydrogen infrastructure projects reliant on fuel-cell manufacturers, thereby constraining overall market momentum. Demand opportunity Despite these challenges, the fast-growing rollout of green hydrogen infrastructure is creating a big demand opportunity for PGMs in 2026–33 period. Proton exchange membrane (PEM) electrolysers, which rely heavily on platinum-based catalysts, are expanding at an annual rate of about 28% across transport and stationary energy applications.Strong policy incentives such as the US Inflation Reduction Act and Canada’s 40% clean hydrogen tax credit are accelerating large-scale electrolyser investment. In South Africa the Integrated Resource Plan (IRP) 2025 further supports this trajectory by promoting a more diversified energy mix that includes solar, wind and green hydrogen. IRP 2025 identifies green hydrogen as a key solution for cutting emissions in hard-to-abate sectors such as steel, cement, chemicals and heavy transport. National hydrogen strategies in Japan and South Korea are positioning Asia as a big emerging demand hub. Fuel cell vehicles, requiring 20–30g of platinum per unit, are projected to exceed 10-million units in production by vehiclemakers by 2032. This shift establishes a structurally new and diversified demand pathway for PGM producers and refiners, moving beyond traditional autocatalyst applications. About 60% of PGMs used in new products are derived from recycled materials, highlighting the maturity and strategic importance of secondary supply channels. The merger of four major North American catalytic converter recyclers in June 2024 to form Elemental North America exemplifies the efficiency gains achievable through consolidation in this space. The global energy transition and the push for decarbonisation offer a compelling future for PGMs. However, South Africa’s ability to fully capitalise on this future hinges on its capacity to foster a stable policy environment that attracts and retains the necessary capital investment, balancing the inherent volatility of commodity markets with predictable governance. • Mabasa, a development economist, is executive manager in the office of the deputy minister of mineral & petroleum resources and co-chair of the Brics Youth Council.

ASHLEY NYIKO MABASA | Policy certainty could act as a shock absorber for the PGM industry

Hydrogen infrastructure and Asian demand drive new opportunities for PGMs

838 words~4 min read