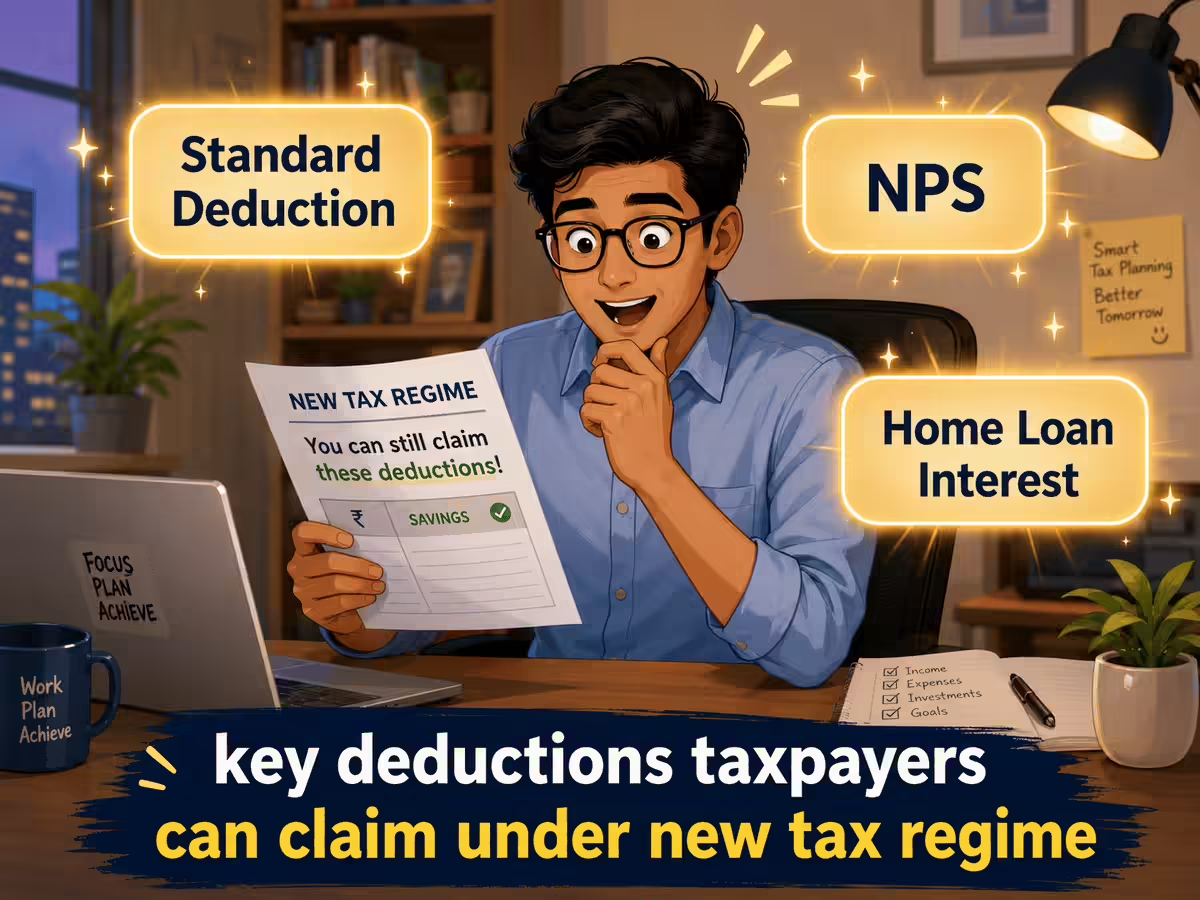

Many taxpayers assume that the new tax regime offers no scope for tax savings. But several deductions, exemptions, and employer-provided benefits are still available under the new tax regime that can help you reduce your tax liability while filing an income tax return (ITR) for FY 2025-26.Here are 7 ways for salaried individuals to lower their tax burden under the new tax regime:1. Employer’s contribution to NPSThe employer’s contribution to the National Pension System (NPS) under Section 80CCD(2) remains one of the most powerful tax-saving benefits available under the new tax regime. The deduction is available to all for employer contributions of up to 14% of the salary (basic salary plus dearness allowance).“This deduction is available over and above the standard deduction of Rs 75,000,” says Sudhir Kaushik, Co-founder & CEO, Taxspanner.For instance, if an employee’s basic salary plus dearness allowance is Rs 12 lakh and the employer contributes 14% to NPS, the Rs 1.68 lakh contribution is eligible for tax deduction. For a taxpayer in the 30% tax bracket, this could translate into tax savings of approximately Rs 52,000, including cess, he explains.However, it should be noted that your own contribution to NPS does not qualify for deduction under the new tax regime.2. Employer’s contribution to EPF also enjoys tax benefitsEmployees’ own contributions to the Employees’ Provident Fund (EPF) are not eligible for deduction because the Section 80C benefit is not available under the new regime.“However, employer’s contributions to EPF continue to enjoy tax benefits subject to the prescribed limits,” says CA Abhishek Soni, CEO & Co-founder, Tax2win.Additionally, for ITR filing for the tax year 2026-27, the due date of which is July 31, 2027, the employer’s contribution to a Recognised Provident Fund (RPF) continues to enjoy tax exemption under the new tax regime.“However, where the aggregate contribution of the employer to the Recognized Provident Fund (RPF), National Pension System (NPS), and Approved Superannuation Fund exceeds Rs 7,50,000 during a tax year, the excess amount becomes taxable as a perquisite under Section 17(1)(h) of the Income-tax Act, 2025,” says CA Milin Bakhai, Partner, Direct Tax, N. A. Shah Associates LLP.Also, annual accretion by way of interest, dividend, or similar earnings on such a taxable contribution is also taxable, he adds.3. Standard deduction continues under the new tax regimeThe standard deduction remains one of the most valuable benefits under the new regime. Salaried employees and pensioners can claim a standard deduction of Rs 75,000.“This deduction is available automatically and does not require any bills or proof of expenses,” says Soni.4. Deduction of home loan interest on let-out propertyInterest on capital borrowed for a let-out house property is deductible under the new tax regime while computing income under the head “House Property”.“However, the deduction can be utilised only against income from house property. Where the interest deduction results in a loss under the head “House Property”, such loss cannot be set off against income under any other head,” says Bakhai.5. Exempt perquisites and reimbursements under the new tax regimeThe tax treatment of perquisites remains largely unchanged under the new tax regime. Accordingly, perquisites that are exempt under the Income-tax Act and Rules continue to remain exempt even where the taxpayer opts for the new tax regime.Meal benefitsFor FY 2025-26 (AY 2026-2027), meal card tax benefit is not available under the new tax regime but only for the old tax regime. However, for the Tax Year 2026-2027, the meal card tax benefit is available under the new tax regime.“With effect from Tax Year 2026-27, free food and non-alcoholic beverages provided by the employer, as well as paid meal vouchers usable at eating joints, are exempt up to Rs 200 per meal,” says Bakhai.Telecom and Broadband ReimbursementsTelephone and internet reimbursements for official use are fully exempt from tax under both old and new tax regimes in India, provided they are based on actual bills submitted to the employer.“The rules continue to exempt reimbursement of mobile phone bills, SIM charges, voice plans, data plans, mobile insurance, broadband expenses, and internet/Wi-Fi expenses for official use,” says Kaushik.Reimbursement is generally available for one mobile phone connection and one broadband/internet connection. The mobile and broadband bills should preferably be in the name of the employee claiming reimbursement, he adds.Mobile/Device leasingEmployer-provided mobile phones under device leasing programmes continue to enjoy favourable tax treatment.“The rules specifically clarify that mobile phones remain excluded from movable asset perquisite taxation, and insurance paid on such devices also continues to enjoy exemption,” says Kaushik.Key conditions include the leasing arrangement to be employer-sponsored, the device to remain covered under the approved leasing policy, and documentation and asset tracking to be maintained, he explains.Health, wellness, and financial wellness programmesHealth clubs, wellness seminars, diagnostic services, sports facilities, employee wellness programmes, and financial wellness initiatives may continue to enjoy favourable tax treatment.“Financial wellness programmes are increasingly being viewed as an extension of employee well-being because financial stress directly impacts productivity, engagement, and mental health,” says Kaushik.The programmes should be offered uniformly to a class of employees, focus on employee well-being and capability enhancement, not be convertible into cash, and should not represent disguised salary payments or personal benefits, he adds.6. Allowances exempt under the new tax regimeMost allowances have become taxable under the new tax regime. However, allowances granted to meet official duties continue to enjoy exemption.“These include allowances received for official travel, transfer, daily expenses incurred during official duties, and transport allowance provided to specially-abled employees,” says Soni.Additionally, an allowance granted for the purchase or maintenance of uniforms required during the performance of official duties continues to remain exempt subject to prescribed conditions, explains Kaushik.7. Exemption on gifts given by employerGifts received by an employee from the employer are exempt from tax up to an aggregate value of Rs 5,000 for the financial year 2025-26. The limit will be increased to Rs 15,000 for FY 2026-27.“Gifts received from specified relatives on the occasion of marriage through inheritance or under a Will are generally exempt regardless of the amount,” says Soni.Additional benefits for family pensioners under new tax regimeIn the case of a family pension received by a family member of a deceased employee, a deduction under Section 93(1)(d)(i) of the Income-tax Act, 2025, is available even under the new tax regime. “The deduction is restricted to the lower of (i) one-third of the family pension received, or (ii) Rs 25,000 per annum,” says Bakhai.

New tax regime: 7 ways for salaried employees to reduce their tax liability while filing ITR for FY 2025-26 - The Economic Times

Salaried individuals can still reduce their tax liability under the new tax regime for FY 2025-26. Key deductions include employer contributions to NPS and EPF, a standard deduction of Rs 75,000, and interest on home loans for let-out properties. Exempt perquisites and certain official allowances also offer tax benefits.

1,058 words~5 min read