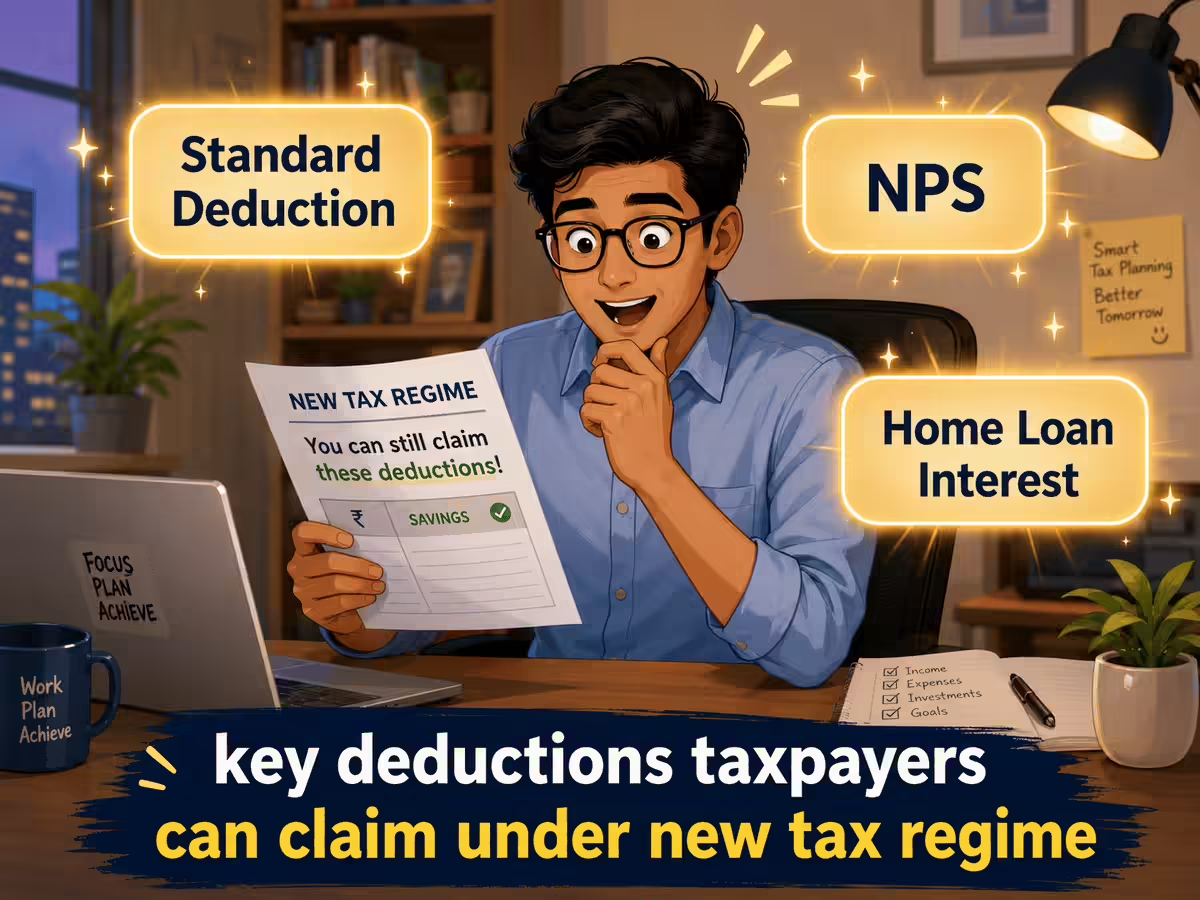

While many taxpayers today choose the New Tax Regime because it offers no income tax on salary income up to Rs 12.75 lakh, they often assume that it provides no deductions at all. This may result in several taxpayers overlooking important tax deductions that are still available under the new regime.While popular deductions such as Section 80C, HRA, LTA and Section 80D are largely not allowed, the New Tax Regime still permits a few key deductions that can help reduce taxable income and lower overall tax liability while filing ITR for FY 2025-26 (AY 2026-27).Here are the 3 key deductions that you can use to reduce your overall tax liability when filing ITR this year.1. Standard deduction under new tax regime: How much can Salaried employees claim?The standard deduction remains one of the biggest tax benefits available under the New Tax Regime.“Salaried employees and pensioners can claim a standard deduction of Rs 75,000. This deduction is automatically applied to salary income and does not require any proof, bills or investments,” says CA Abhishek Soni, CEO & Co-founder, Tax2win.For example, if your salary income is ₹15 lakh, your taxable salary becomes ₹14.25 lakh after claiming the standard deduction.This increased standard deduction (from Rs 50,000 to Rs 75,000) was introduced in the Union Budget 2024 to increase disposable income for salaried taxpayers under the new regime.2. Employer’s Contribution to NPS [Section 80CCD(2)] Employer contribution to the employee’s National Pension System (NPS) Tier-I account is also allowed as a deduction under the new tax regime. For taxpayers opting for the new income tax regime, a specified deduction is allowed.“Deduction Limit: Up to 14% of salary (basic + DA) for employees opting for the new tax regime. This deduction is over and above the standard deduction and can help salaried individuals save significant tax,” says Soni.For instance, if your basic salary is Rs 10 lakh and your employer contributes Rs 1.4 lakh to NPS, the entire amount can be claimed as a deduction, he adds.However, the tax benefit is only given if the combined employer contribution to the NPS, EPF, and superannuation fund does not exceed ₹7.5 lakh in a financial year. Also, investments under the NPS Tier-II account do not qualify for tax benefits.3. Interest on Home Loan for Let-Out Property [Section 24(b)]While deduction for home loan interest on self-occupied property is not available under the new tax regime, taxpayers can still claim a deduction on interest paid on let-out property.“For a let-out property, there is no monetary cap on tax deductibility of interest expense incurred on loan borrowed for acquisition or construction of such property. This position remains the same for individuals under new as well as old tax regime. The difference is individuals under new tax regime cannot set-off the losses from house property against other eligible income,” says Rahul Jain, Partner at Khaitan & Co.“As per Section 22(1)(b) read with Section 202 of the ITA 2025 (corresponding to section 24 read with section 115BAC of the ITA 1961) under the new tax regime, there is no specific monetary ceiling prescribed for deduction of interest on housing loan in respect of a let-out property while computing income under the head Income from House Property”, says CA (Dr.) Suresh Surana.Accordingly, the actual interest incurred on borrowed capital may be claimed as a deduction, he adds.Other deductions available under the New Tax RegimeAccording to Soni, apart from the above, a few additional deductions/exemptions are also available:● Deduction on family pension: Lower of Rs 25,000 or one-third of the pension received● Agniveer Corpus Fund deduction under Section 80CCH● Certain allowances such as conveyance allowance, transport allowance for specially-abled employees, and travel allowances for official duties● Deduction under Section 80JJAA for eligible businesses on additional employee cost The New Tax Regime offers lower tax rates but limits the availability of deductions and exemptions. Therefore, taxpayers should compare both tax regimes carefully before filing their ITR to determine which option results in lower tax liability based on their salary structure, investments and eligible deductions.

New income tax regime: Don’t miss out on these 3 key deductions that will reduce your taxable income & help save more tax - The Economic Times

Many taxpayers mistakenly believe the New Tax Regime offers no deductions. However, salaried employees and pensioners can claim a Rs 75,000 standard deduction. Employer contributions to NPS and interest on home loans for let-out properties are also still permissible, reducing overall tax liability.

668 words~3 min read