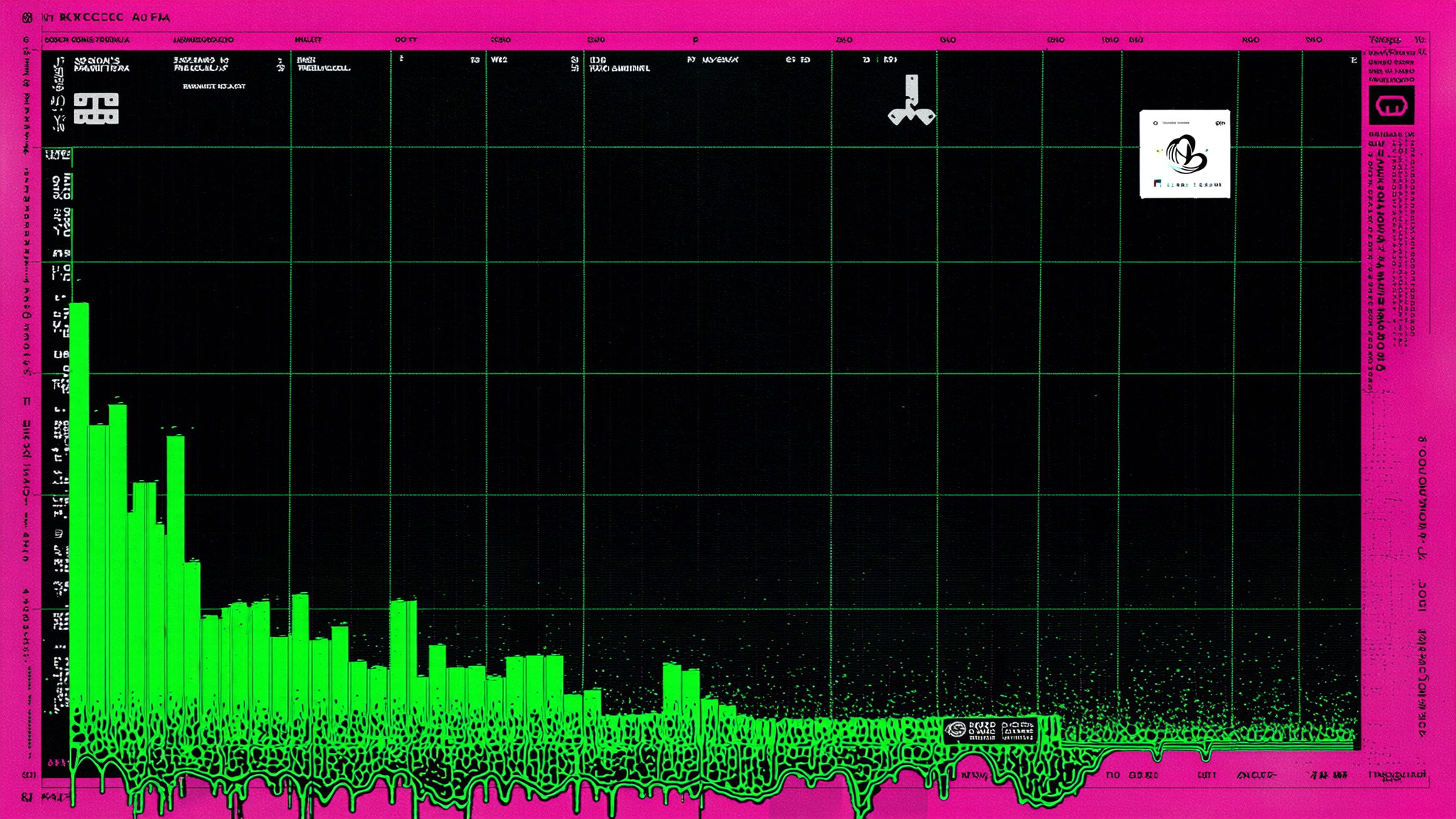

Fees generated by DeFi’s biggest lending protocols and decentralized exchanges cratered by as much as 65% week-over-week following early June’s market selloff. The contraction spans both sides of the DeFi fee equation: lending fees, which include borrow interest, flashloan fees, and liquidation penalties, plus the trading fees that DEXs collect on every swap. Both categories compressed sharply as borrowing demand dried up and trading volumes retreated across major platforms like Aave and Uniswap.

Leverage unwind, not structural collapse

What happened in early June was a classic deleveraging event. Bitcoin tested lower levels around the $61,000 to $64,000 range, triggering cascading liquidations and forcing traders to close positions. Solana experienced particularly notable drawdowns. The result was a rapid unwinding of the leverage that had accumulated during the preceding months of bullish activity.

Outstanding loans across DeFi had risen by over 37% year-to-date heading into June 2026. When the market turned, all that borrowed capital became a liability rather than an asset. Borrowers either got liquidated or voluntarily reduced their exposure, draining utilization rates across lending protocols.