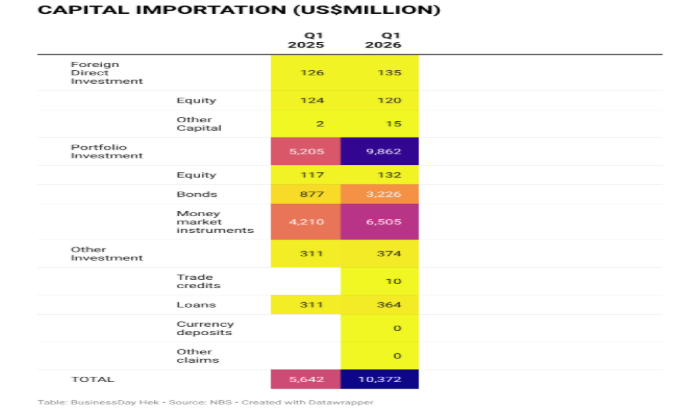

The current debate over Nigeria’s capital-importation figures has generated far more heat than light. On one side stands a government eager to present the $10 billion that entered the country during the first quarter of 2026 as proof that its economic reforms are working. On the other stand critics who point to the composition of those inflows and dismiss them as little more than speculative capital chasing exceptionally high yields. Both sides have facts on their side.

Both are also missing the deeper story.

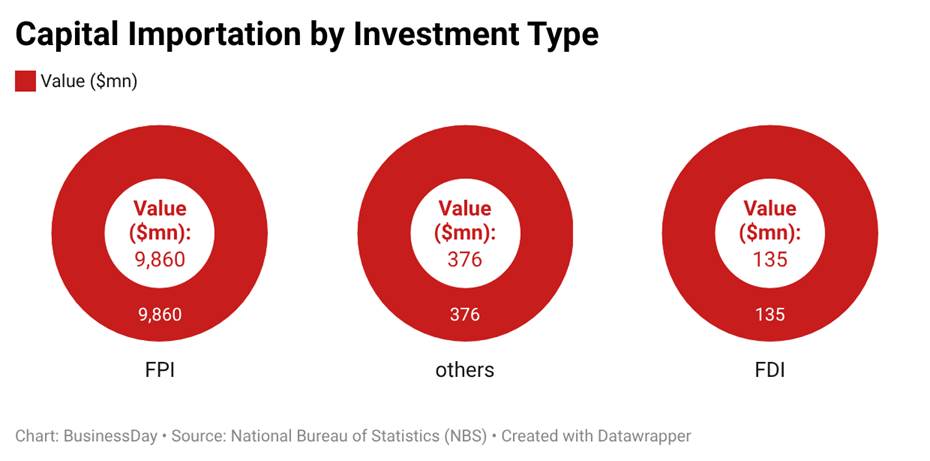

The government is correct that the inflows matter. After years in which international investors largely avoided Nigeria, the return of significant foreign capital is not an insignificant development. Yet the critics are equally correct that the overwhelming majority of those inflows arrived not as foreign direct investment but as portfolio capital, much of it flowing into Treasury bills and other short-term money-market instruments. Foreigners are lending to Nigeria far more enthusiastically than they are investing in it.

The argument has therefore become trapped in a false binary. One camp sees success. The other sees failure. One sees confidence. The other sees illusion. Yet the most important question raised by the figures is neither financial nor ideological. It is institutional.