Banks should be prepared to make additional provisions for the expected deterioration in asset quality under the expected credit loss framework

| Photo Credit:

Deepak Verma

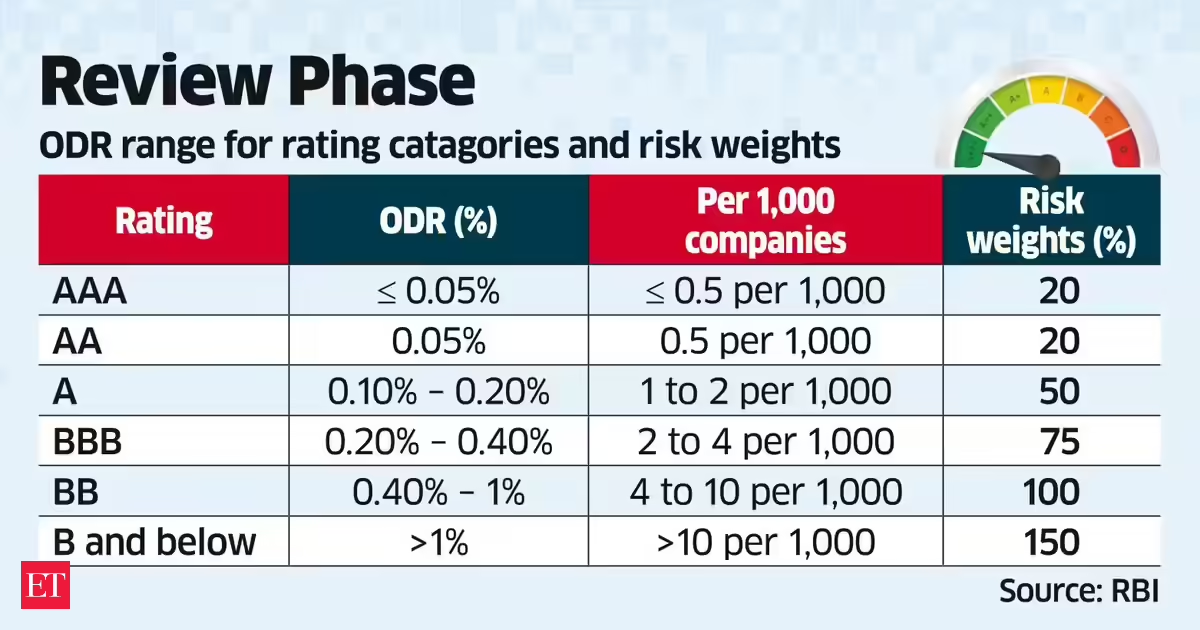

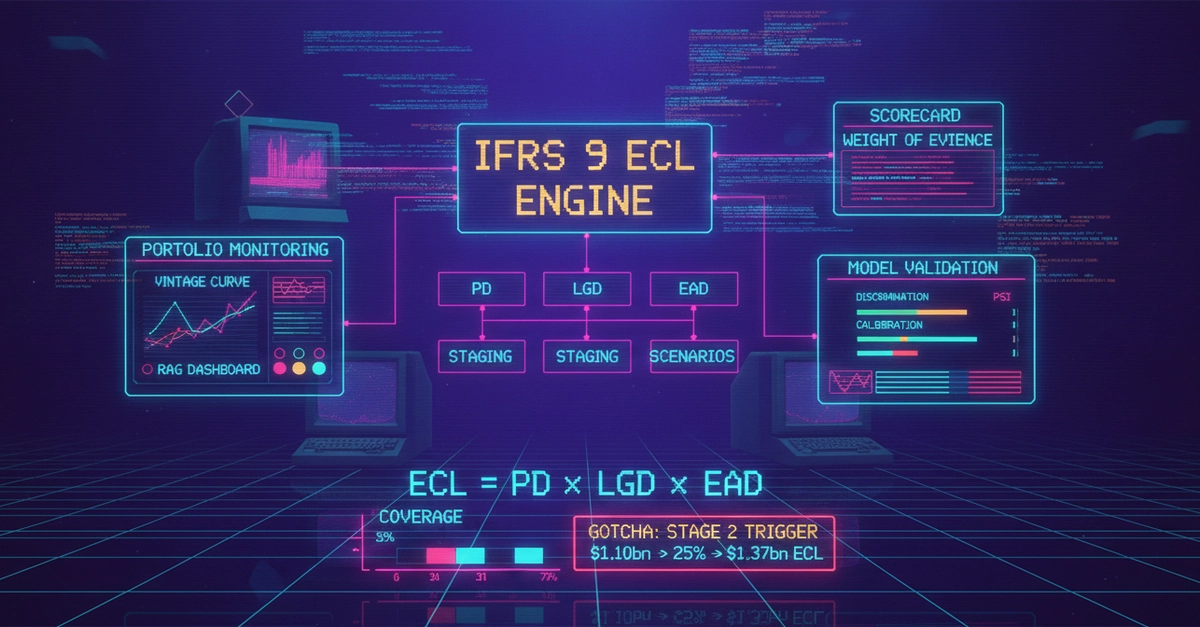

While banks are actively preparing to adopt the expected credit loss (ECL) framework and migrate to the Basel 3.1 framework from April 1, 2027, the recent surge in credit risk due to geopolitical developments has added new dimensions to credit risk management (CRM). Banks, however, are in a strong position, with gross non-performing assets (GNPA) at 1.73 per cent in March 2026, down from 2.22 per cent in March 2025, and a strong capital adequacy ratio of 17.68 per cent.Banks should be prepared to make additional provisions for the expected deterioration in asset quality under the ECL, and even if aggregate risk-weighted assets are low under the Foundation Internal Ratings-Based (FIRB) approach which the lenders may migrate to or under Basel 3.1. These two key regulatory policy measures can strengthen CRM but may impinge upon some key performance parameters such as NIM/ROA/EPS unless proactive measures are taken.CRM dataSince the ECL framework calls for a minimum of five years of data to compute its components — probability of default (PD), loss given default (LGD), and exposure at default (EAD) — a look at past data will be pertinent. The ratio of loan assets to total assets was 61 per cent in FY22, which jumped to 64.5 per cent by FY26, with an average loan-to-total assets ratio over the last five years of 62.6 per cent. Similarly, among the risk-weighted assets (RWAs) forming the basis for computing the capital adequacy ratio (CAR), RWAs on loan assets were 82.1 per cent in FY22, rising to 84.8 per cent by FY26. The data clearly indicate that in the risk management hierarchy, CRM is the backbone of the risk architecture and has a major impact on balance sheet management. Credit risk intelligence must be so sharp and data-driven that composition of loan assets, internal and external ratings, risk weights, risk-based pricing, and trends in PD, LGD, EAD, SMA, and CRILC data should be under close scrutiny.As banks move towards the Basel 3.1 framework, even if the RBI has not approved migration to the FIRB model, banks should run it as a parallel model alongside the conservative mandatory standardised approach to determine how close the risk weighted architecture to the 72.5 per cent floor limit enshrined in Basel 3.1, so that compliance is possible as soon as the RBI permits FIRB and to later adopt advanced credit risk assessment approaches. The four-year transition period can serve as a springboard for adopting the international CRM standards by March 2031.The tighter regulatory norms call for rewriting the rule book of CRM. Right from sourcing the credit, through sanction and disbursement, monitoring, control, and intervention, and ultimately to debt resolution, the process should be quality-focused and risk-weight-sensitive.Credit risk governance and board oversight may need to extend not only to the asset-liability management structure, growth in balance sheet, profitability, asset quality, but also to the composition of RWAs to ensure healthy growth of the credit portfolio. The risk-based internal audit teams should be persuaded to guide management on economising on risk weights without compromising business potential.The CRM teams — sourcing, managing, and risk intelligence — should be developed with different objectives but all of them converging into one outcome — competitive asset quality with sustained risk-adjusted returns while consuming low capital, making the aggregate credit portfolio less risky. This needs a mix of loan assets phased over a 5-7-year time-frame, using strategic AI tools for better forecasting and developing a CRM vision with shifting year-on-year goals.Moving from a credit growth model of ‘let it grow’ to ‘make it grow’ is the critical factor in changing the mix of loan assets over time.The writer is an Adjunct Professor, Institute of Insurance and Risk Management, Hyderabad. Views are personalPublished on June 16, 2026