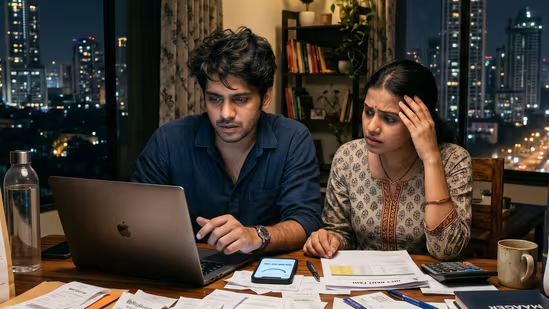

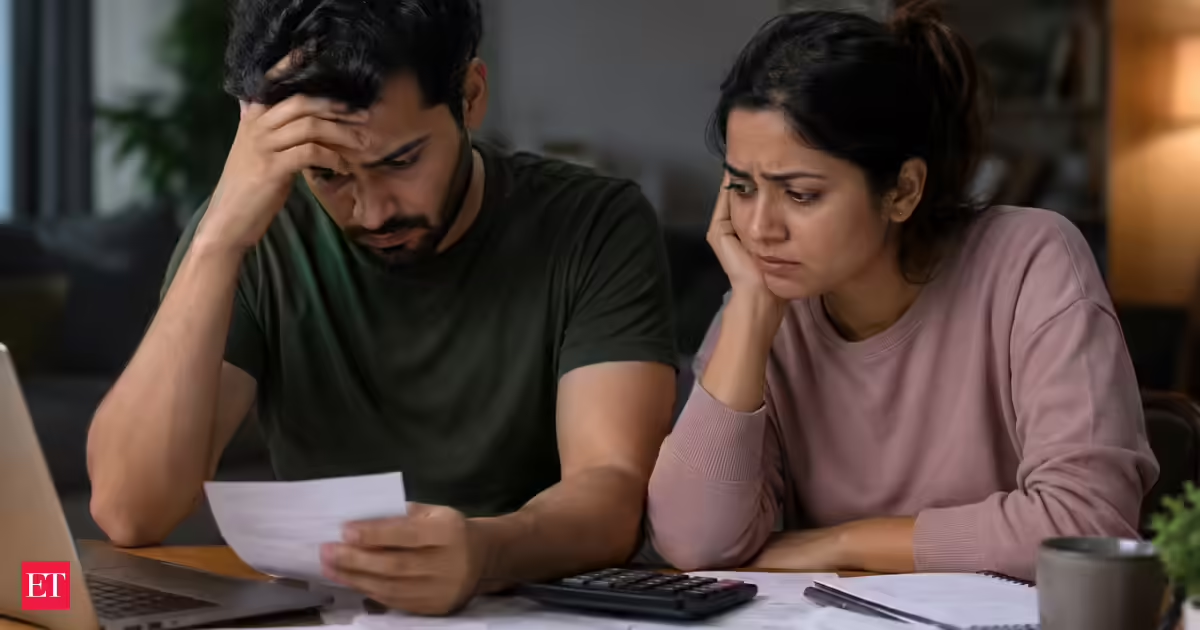

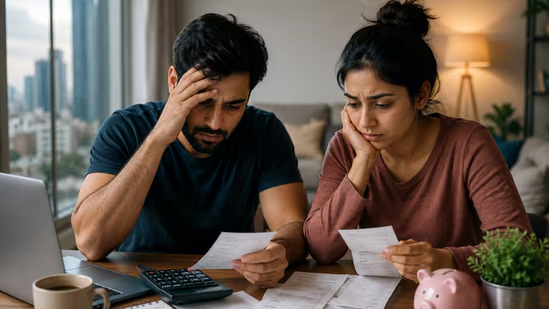

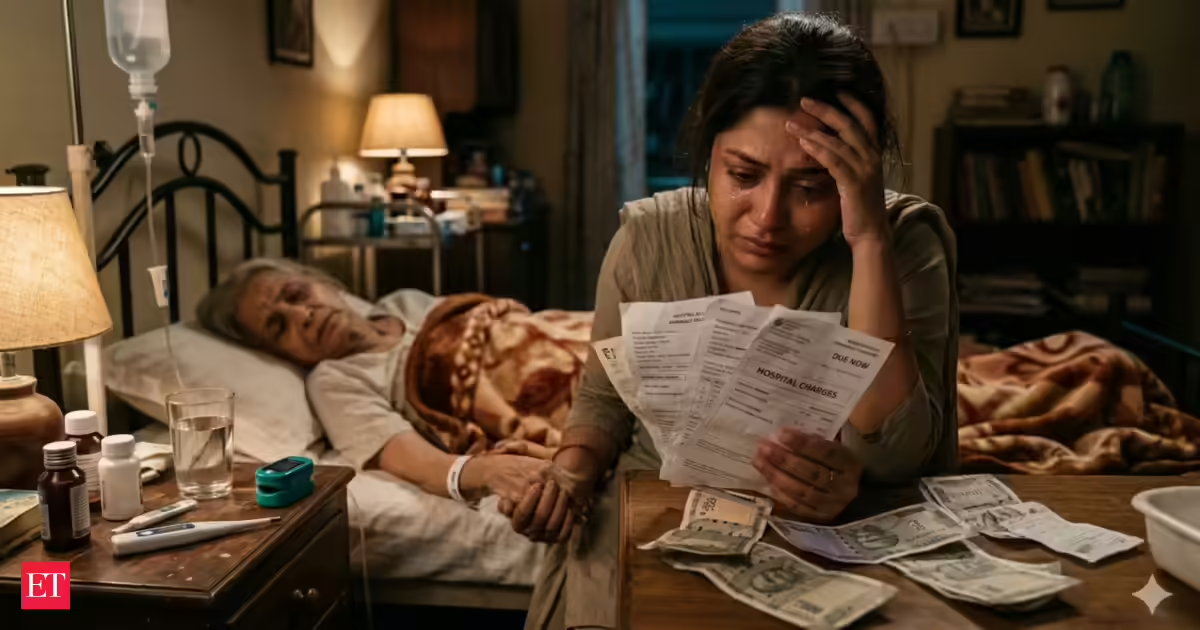

Managing debt can be overwhelming, especially when there is no financial safety net to fall back on. A recent Reddit post from a 31-year-old woman has struck a chord with thousands online after she opened up about her struggle to balance two loans, household expenses, rent, and caring for her mother on a monthly salary of ₹70,000.The woman, who lives in a Tier-2 Indian city with her mother, said she is unmarried, has no savings, owns no property, and is the sole earning member of the family. Her emotional post, titled "Need help, don't know what to do anymore," highlighted the financial stress that has left her unable to sleep properly.ALSO READ: Tuesday Work Quote of the Day by Immanuel Kant‘Every Month Is About Somehow Getting Through’According to the Reddit post, the woman earns ₹70,000 a month but spends nearly half of it servicing debt. She revealed that she has two active loans:A ₹13 lakh loan taken in December 2024 with an EMI of ₹23,000 and a tenure of 84 months at 12% interest.A ₹2.5 lakh loan taken in April 2025 with an EMI of ₹10,000 and a tenure of 30 months at 9% interest.ALSO READ: You've probably used his code today, but the man behind YouTube, Netflix and TikTok isn't a billionaireTogether, the two EMIs add up to ₹33,000 every month, leaving her with around ₹37,000 for all other expenses. That remaining amount covers rent, groceries, utility bills, her mother's medicines and other household costs."Some months I genuinely don't know how we'll manage the last week," she wrote.The woman clarified that the loans were not taken for luxury purchases. Instead, she said they were the result of circumstances and decisions she now regrets.The ₹5 Lakh Loan Plan She Is ConsideringLooking for a way to ease the pressure, the woman shared a financial strategy suggested by someone she knows. The proposal involves taking a fresh loan of ₹5 lakh at an interest rate of 6.5%.She explained that the money would be used in three ways:₹2 lakh to close the smaller ₹2.5 lakh loan early.₹2 lakh to be invested in a fixed deposit earning around 8% interest.₹1 lakh to cover urgent household expenses.The logic behind the plan is that the new loan carries a lower interest rate than the existing 9% loan, while the fixed deposit could potentially generate a higher return than the interest being paid.She also hopes that closing the smaller loan would eventually free up the ₹10,000 EMI and improve her monthly cash flow. However, she was unsure whether the strategy actually made financial sense and turned to Reddit for guidance.Need help, don't know what to do anymore. Two loans, 70k salary, single mother, and I'm barely surviving each month. byu/Traditional_Gene_8 inpersonalfinanceindiaReddit Users Raise ConcernsMany Reddit users advised caution, arguing that taking another loan while already struggling with debt could create additional financial pressure. "From where you are getting loan at 6.5%. Throw some light," asked a user in the comment section.Several commenters pointed out that borrowing money to invest in a fixed deposit rarely works in practice once taxes, loan processing charges and other costs are considered.Others questioned whether it made sense to increase overall debt just to gain a small difference between loan interest and FD returns. "Be strong, look for a part time job from where you can make 15-20 k extra every month. Way better than taking another loan," said another.One common suggestion was to focus on reducing liabilities rather than creating new ones. Some users also recommended building a detailed monthly budget to identify areas where expenses could be reduced, even temporarily.The Reality of Being the Sole BreadwinnerThe Reddit post resonated with many users because it reflects a challenge faced by countless middle-class families. Being the only earning member of a household often means carrying responsibilities beyond personal finances. Medical expenses, rent, inflation and loan repayments can quickly stretch monthly income, leaving little room for savings.For individuals supporting elderly parents, the pressure can be even greater, particularly when unexpected expenses arise.Key Lessons From the DiscussionThe conversation generated several takeaways for people facing similar situations:Understand Your Total Debt CostBefore taking a new loan, calculate the overall repayment amount, including processing fees and interest.Avoid Borrowing to InvestUsing borrowed money for fixed deposits or similar investments may not always deliver the expected benefit.Prioritise Cash FlowA sustainable monthly budget is often more important than short-term financial fixes.Explore Restructuring OptionsBorrowers facing difficulties can speak with lenders about refinancing, tenure extensions or restructuring possibilities.Build an Emergency BufferEven small monthly savings can help reduce dependence on future borrowing.Disclaimer: This article is based on a user-generated post on Reddit. ET.com has not independently verified the claims made in the post and does not vouch for their accuracy. The views expressed are those of the individual and do not necessarily reflect the views of ET.com. Reader discretion is advised.

‘Rs 70,000 Salary, Rs 15.5 lakh debt, no savings, no property and a dependent mother’: Woman’s viral post on loan burden sparks financial advice

A 31-year-old woman's plea for financial help on Reddit highlighted the struggles of being the sole earner supporting her mother on a ₹70,000 monthly salary. She detailed managing two loans, household expenses, and medical costs, leading to significant stress and sleepless nights. A proposed ₹5 lakh loan to consolidate debt and invest was met with caution from users.

TL;DRAI

Woman earning ₹70k/month with ₹15.5 lakh debt considers ₹5 lakh consolidation loan while supporting her mother. Reflects how debt constrains career mobility for breadwinners—dynamics affecting talent retention and costs in emerging markets.

807 words~4 min read