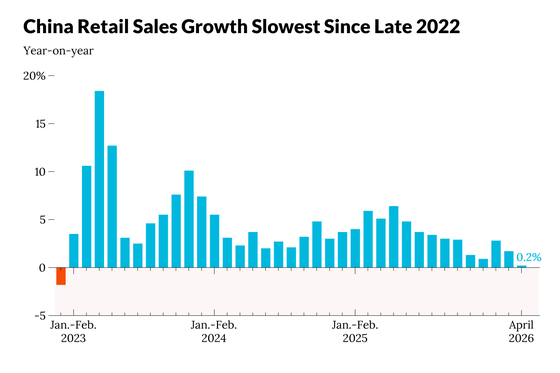

China’s consumer engine is sputtering. April retail sales growth clocked in at a mere 0.2% year-over-year, the weakest reading since December 2022, when the country was still unwinding its zero-COVID policies. For context, economists had expected something closer to 2%. They got a rounding error instead.

The sharp deceleration from March’s already tepid 1.7% growth rate has prompted major financial institutions to slash their outlook for the rest of 2026. HSBC cut its full-year retail sales growth forecast nearly in half, from 5.2% to 2.8%.

The numbers paint a grim picture

Cumulative retail sales for January through April 2026 totaled 16.49 trillion yuan, roughly $2.41 trillion. That figure represents a 1.9% year-over-year increase.

A 1.9% nominal increase in an economy that’s been running persistent deflation means the real spending picture is even more anemic. The culprits are familiar at this point: a property market downturn that refuses to bottom out, consumer confidence that remains stubbornly low, and deflationary pressures that make waiting to buy things, rather than buying them now, the economically rational choice.