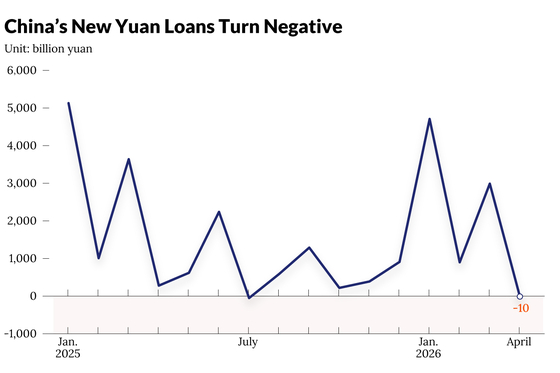

China’s credit engine sputtered back to life in May after April delivered one of the ugliest lending prints in recent memory. New yuan loans contracted by 10 billion yuan ($1.47 billion) in April 2026, the first outright decline since July 2025, and a number so far below the consensus forecast of 300 billion yuan in new lending that it forced a collective double-take across trading floors.

April’s credit shock in context

To understand why May’s bounce matters, you have to appreciate how bad April actually was. New yuan loans didn’t just miss expectations. They went negative. The prior month had delivered 2.99 trillion yuan in fresh lending, making the swing from nearly 3 trillion to negative 10 billion one of the most dramatic month-over-month reversals in China’s credit data.

Outstanding yuan loan growth slid to 5.6% year-over-year in April, a record low. That’s down from 5.7% in March, continuing a steady erosion that has become a defining feature of China’s economic landscape.

The broader credit picture was equally grim. Aggregate financing to the real economy, or AFRE, came in at less than 630 billion yuan for April. The median forecast had been roughly 1.3 trillion yuan.