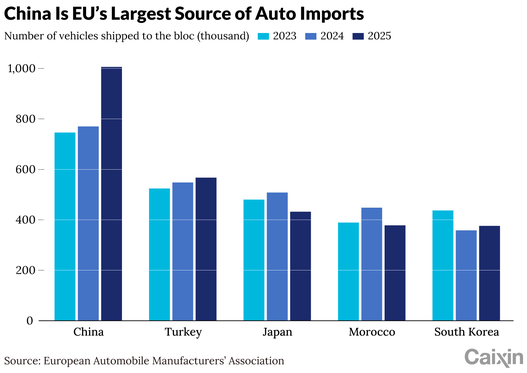

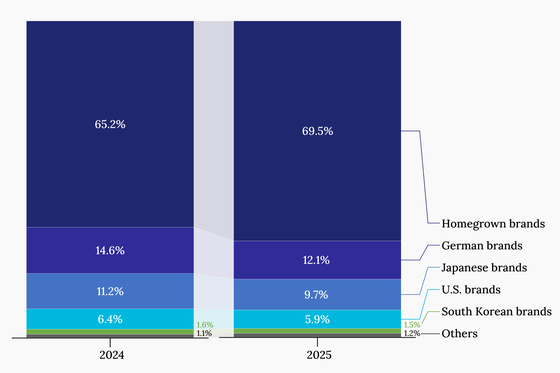

1. Chinese carmakers are expanding their presence in Europe, reshaping the continent's auto market even as the EU attempts to curb the rise of China-made electric vehicles (EVs) with punitive tariffs, investment restrictions, and stricter localization rules. [para. 1] According to the European Automobile Manufacturers’ Association (ACEA), China remained the EU's largest source of auto imports in 2024, with shipments surging about 30% year-on-year to exceed 1 million cars for the first time, driven by strong demand for plug-in hybrids and conventional vehicles. [para. 2]2. Despite the EU imposing countervailing duties on China-made EVs, Chinese brands captured about 9% of EU pure EV sales in 2025, up from 2% in 2021. Cigdem Cerit of Fitch Ratings attributed this growth to competitive pricing, technological edge, and attractive configurations. [para. 3][para. 4] In response, the European Commission introduced the Industrial Accelerator Act, requiring EVs to be assembled within the EU and source at least 70% of non-battery components locally to qualify for public procurement and subsidies. [para. 5] Some Chinese carmakers have accelerated plans to establish local manufacturing to circumvent tariffs and meet compliance. [para. 6]3. Chinese EV-makers are pursuing different strategies to gain a foothold in Europe. BYD shifted focus to hybrids after EU duties, and its Seal U plug-in hybrid SUV became Europe's best-selling model in its category in 2025, priced about 20% cheaper than Volkswagen's Tiguan. [para. 8][para. 9][para. 10] Leapmotor leveraged its partnership with Stellantis, with EV registrations in the EU more than sextupling to 28,000 cars in the first four months of 2026. Its T03 compact EV, starting at 4,900 euros after subsidies, became Italy's best-selling all-electric car in April. [para. 11][para. 12] XPeng is betting on technology, testing an intelligent driving system and offering Level 2 assisted-driving features. [para. 13] However, success is concentrated: of 21 Chinese automakers that entered the EU, only nine sold more than 1,000 new-energy vehicles last year. [para. 14]4. The EU's response is evolving beyond tariffs, with investment screening, localization requirements, and carbon-related trade measures. The proposed Industrial Accelerator Act would impose restrictions on foreign investment in strategically important sectors, including EVs, where a single country accounts for over 40% of global manufacturing capacity. Projects worth €100 million or more would face enhanced scrutiny and need to meet at least four of six conditions, including capping foreign ownership at 49%, licensing IP, spending 1% of annual revenue on local R&D, and sourcing at least 30% of components locally. [para. 15][para. 16][para. 17][para. 18]5. The proposal has exposed divisions within the bloc: France supports tougher safeguards, while Germany is more cautious due to its carmakers' dependence on the Chinese market. Zheng Yun of Roland Berger noted that Chinese automakers with existing or planned factories in Europe could face additional scrutiny. Local R&D, hiring, and procurement are relatively easy to fulfill, but ownership caps and technology transfer provisions pose significant challenges. [para. 19][para. 20][para. 21] The EU may revise some provisions to accommodate competing interests, and the act is estimated to take effect no earlier than 2027. [para. 22][para. 23]6. Another challenge is carbon-related trade barriers. The EU's Carbon Border Adjustment Mechanism (CBAM), effective January 2025, applies a carbon levy on imported cement, steel, aluminum, etc. The European Commission has proposed extending CBAM to cover nearly 180 downstream products, including cars and auto parts, from 2028. Isadora Wang of Transition Asia noted that while assembled vehicles are not yet covered, the trend of regulation moving downstream is clear, potentially adding carbon costs for Chinese auto exports. [para. 24][para. 25][para. 26]7. In response to protectionist measures, Chinese automakers are deepening manufacturing localization in Europe through partnerships. Chery became the first Chinese automaker to produce vehicles in Europe, signing a joint venture with Spain's EV Motors in April 2024 to revive a former Nissan plant in Barcelona. [para. 27][para. 28] Guangzhou Automobile Group and XPeng opted for contract manufacturing with Magna International, allowing localization without building their own factories. Contract manufacturing provides a faster and cost-effective route while benefiting from Magna's familiarity with local regulations. [para. 29][para. 30][para. 31]8. Leapmotor and Dongfeng have expanded partnerships with Stellantis. Leapmotor is evaluating building a new production line at Stellantis's Zaragoza plant in Spain to manufacture both an existing model and an Opel all-electric model. Dongfeng and Stellantis announced plans to form a joint venture to sell and produce EVs under Dongfeng's Voyah brand in Europe, with production at Stellantis's Rennes plant in France. Stellantis has become a sought-after partner due to its manufacturing footprint and underutilized capacity. BYD is also exploring cooperation, including potential acquisition of some of Stellantis's underused European factories while its own Hungary plant runs on a trial basis. [para. 32][para. 33][para. 34][para. 35]AI generated, for reference only

In Depth: Chinese Carmakers Push Deeper Into Europe Despite Rising EU Trade Barriers

EV-makers, from giants such as BYD to upstarts including Leapmotor and XPeng, are gaining market share despite tariffs, while new localization and carbon rules accelerate the shift toward manufacturing inside Europe

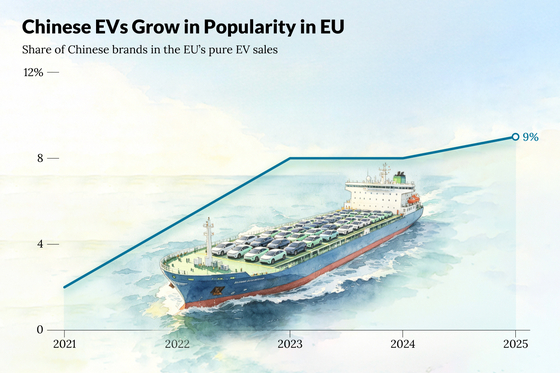

784 words~4 min read