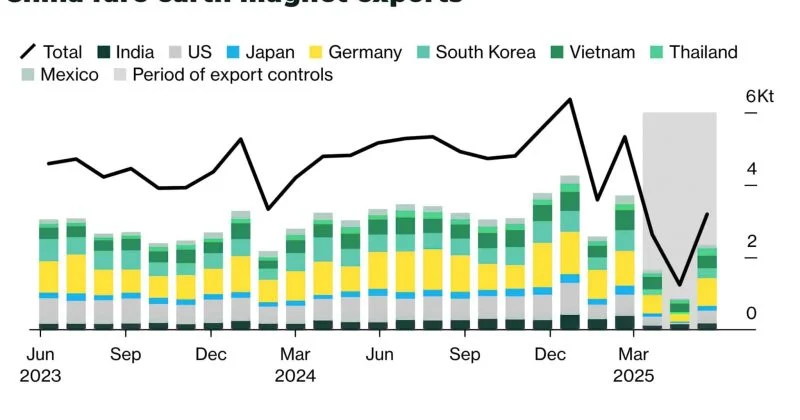

When one country controls roughly 90% of global processing capacity for a critical resource, it doesn’t need missiles to wage economic war. It just needs paperwork. On April 4, 2025, China’s Ministry of Commerce published Announcement No. 18, imposing export controls on seven medium and heavy rare earth elements: yttrium, samarium, gadolinium, terbium, dysprosium, lutetium, and scandium.

The result has been a masterclass in supply-side economics. Yttrium oxide prices in European markets have climbed to approximately $270/kg by late 2025, representing a roughly 4,400% increase. Spot prices surged nearly 1,500% from 2024 levels, when yttrium traded below $8/kg, to about $126/kg.

The numbers behind the squeeze

Here’s the thing about rare earth export controls: they don’t technically ban exports. They require special export licenses, which is bureaucratic code for “good luck getting approval.” The practical impact has been indistinguishable from an outright ban for most buyers.

US imports of yttrium from China tell the story cleanly. In the eight months before the controls took effect, the US imported 333 tons. In the corresponding period afterward, that figure collapsed to 17 tons. That’s a decline of roughly 95%.