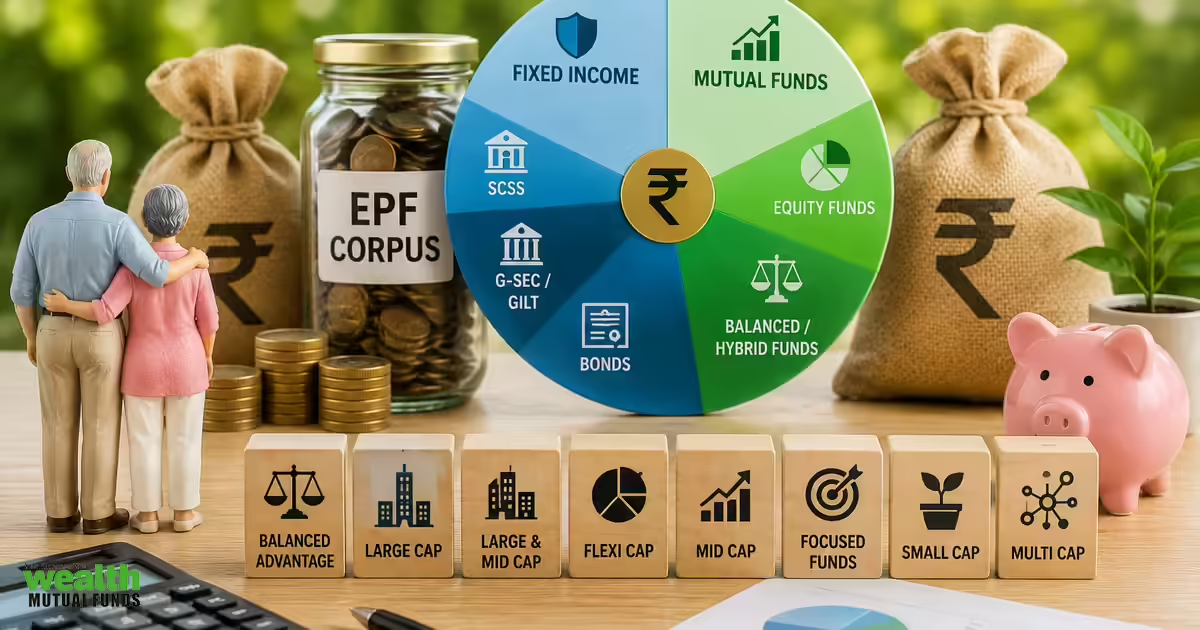

When you start your retirement planning, two things are important- your monthly withdrawal should support your lifestyle, and the corpus should not deplete in your life. For that, you need to consider factors such as inflation, asset mix, liquidity, medical emergency fund, etc, while planning for retirement. Here, we discuss seven points you can consider for a smooth retirement. 1.Plan for adequate corpus based on lifestyle and expenses When you plan your retirement, calculate corpus required for at least 20-25 years. The corpus should be based on your current lifestyle. But if you have some liability such as home loan or responsibility such as child marriage, also plan for those expenditures. 2.Don't forget to factor in inflation Ignoring inflation can deplete the value of your retirement corpus. For example, if you are 40 years old today and have Rs 50,000 as monthly expenses, at 60 years of age, you need Rs 1.09 lakh to maintain the same lifestyle at a 5% inflation. At 80, the same expenditure will reach Rs 2.40 lakh/month. So, remember, you are planning for the future, not for today. Build a corpus that will be adequate for your retirement. 3.Have separate provision for medical funds Many people don’t have a medical insurance plan for old age. For many others, medical cover ends when a person reaches a certain age. Sometimes, a medical insurance plan can have sub limits and may not cover certain diseases. For these reasons, you need to plan for a medical emergency fund from your own resources. For it, you can keep aside a fund to deal with medical emergencies. Since medical expenses rise with time, your fund should be adequate to cover them. 4.Give some equity exposure to your retirement corpus If you put your entire fund in safe assets, it may not be able to beat inflation and generate adequate income. So at least some part of corpus can be invested in equity for higher returns. You can invest a portion of your corpus in equity that you may require after 5-7 years. You may also follow the bucket strategy from where, you can shift profit of the equity investment to debt buckets as it may be used to meet short-term liquidity requirements. 5.How your asset mix should change with age With age, your risk appetite comes down. So, your risk exposure should also reflect your age. Equity is considered to be a risky asset which also gives higher return in long term. Giving an equity exposure to your retirement corpus can help it grow in the long term. However, as your age increases, you can decrease your equity exposure and increase debt exposure. For example, at 60 years of age, you can invest 40% of your corpus in equities, but in the next 15 years, you can bring it down to 25%. Such a strategy will ensure growth and liquidity both. 6.Clearly mark fund for own consumption and succession You can also leave a part of your retirement corpus for your heirs. However, for that you need to clearly mark the corpus required for your own needs and for succession. Scheme such as Senior Citizen Savings Scheme, RBI floating bond, Monthly Income Scheme provide you an interest while your principal remains invested. If you want to leave the principal amount from such schemes for your heirs, you should nominate them and write their names in Will to ensure smooth succession. 7.Have provisions for emergency liquidity option Sometimes, your retirement corpus may turn out to be inadequate. At such times, you may use some asset to generate an income or use the legacy fund left for heirs. For example, if you have gold, you can invest it in a gold monetisation scheme from where, you can get an amount that you can invest to generate an income from intrest. Or, if you have a home, you can keep it as a collateral and take a reverse mortgage loan on it, from where, you can get periodic payments. If you are left with no other option, you can also use some corpus from the legacy amount. You should focus on generating sustainable income while preserving the corpus during retirement. But you should also factor in inflation, lifestyle needs, liabilities and healthcare costs while estimating a retirement corpus. Maintaining an appropriate asset mix, giving some exposure to equity and shifting to debt with age can ensure liquidity and growth both. Plan for corpus you need for yourself and want to leave for your heirs but also be ready with emergency liquidity option to meet unforeseen financial requirements

Retirement planning: 7 golden rules you must consider for easy retirement - The Economic Times

Retirement planning should focus on generating sustainable income while ensuring the corpus lasts throughout life. Key factors include accounting for inflation, healthcare costs, liabilities, and lifestyle needs. Maintaining a balanced asset mix with some equity exposure for growth and gradually increasing debt allocation with age can provide liquidity and stability.

764 words~3 min read