1. For over a decade, millions of Chinese mainland investors bypassed strict capital controls using internet brokerage apps to trade U.S. and Hong Kong stocks, but this multibillion-dollar grey market now faces eradication. [para. 1]2. On May 22, the China Securities Regulatory Commission (CSRC) launched a two-year campaign with seven other ministries to wipe out illegal cross-border securities operations, while Hong Kong regulators simultaneously updated rules to seal off grey channels. [para. 2]3. Under the new framework, all onshore websites, trading applications, and servers operated by offshore brokerages lacking domestic licenses will be shut down. Existing mainland clients have a two-year transition period to sell holdings and withdraw funds, with all new buying and depositing strictly prohibited. [para. 3]4. The regulatory dragnet targets major online platforms such as Nasdaq-listed Futu Holdings Ltd. (5.95 million registered accounts, $158.5 billion total client assets), Up Fintech Holding Ltd. (2.66 million accounts, $60.8 billion), and Long Bridge HK Ltd., which provided marketing and order-processing services on the mainland. [para. 4][Graphic]5. Market observers say the move underscores Beijing’s unwavering grip on its closed capital account. While global banks like Goldman Sachs have secured wholly foreign-owned securities licenses in China, their operations are confined to the domestic A-share market, and Beijing has never issued a license for cross-border securities brokerage to mainland retail investors. [para. 5]6. Some domestic critics argue regulators could gradually bring grey brokers into the formal framework through licensing and quotas, but opponents counter that allowing individuals to massively accumulate offshore securities would destabilize exchange rates and monetary policy. [para. 6]7. Miao Yanliang of China International Capital Corp. noted that opening the capital account requires careful macroeconomic coordination, flexible exchange rates, and robust prudential regulation. [para. 7]8. Internet brokers like Up Fintech and Futu thrived by exploiting a structural loophole: offshore licensed entities handled core securities services while mainland operations were registered only for technical support. Futu secured a Hong Kong Type 1 license in 2012; Up Fintech acquired a New Zealand provider in 2015. [para. 9][para. 10]9. By end of 2020, the firms boasted over 2.5 million accounts and trading volumes exceeding $220 billion. Regulators began eyeing them from 2015, and in 2022 the CSRC explicitly declared their operations illegal, banning new mainland client solicitation. In June 2025, a report alleged Up Fintech continued illegally acquiring new clients; the company denied this. [para. 11][para. 12][para. 13]10. On May 22, the CSRC proposed roughly 2.3 billion yuan ($338 million) in confiscations and fines against the two firms and their founders, applying a "substance over form" standard. Based on end-2025 data, the firms face forced liquidation of an estimated 570,000–630,000 mainland-funded accounts holding $27–$29 billion in assets. [para. 14][para. 15]11. Hong Kong’s Securities and Futures Commission and Monetary Authority updated their guidelines on the same day, requiring brokers and banks to obtain written client declarations proving investment funds originate from legal, non-mainland sources. [para. 21]12. After mainland regulators halted new domestic client onboarding in late 2022, some Hong Kong firms exploited a loophole by accepting clients with statements from other offshore brokers. A recent SFC probe found widespread compliance failures, including forged documents in more than half of sampled accounts. [para. 22][para. 23]13. With a strict two-year transition period, industry insiders expect a total "physical cutoff" of mainland investors, likely using dual IP and GPS tracking similar to the cryptocurrency crackdown. [para. 25]14. Regulators are nudging investors toward formal avenues such as the QDII program (cumulative $176.2 billion approved quotas as of late April), Stock Connect (requiring 500,000 yuan minimum), and Cross-boundary Wealth Management Connect (confined to Greater Bay Area). [para. 26][para. 27][para. 28]15. However, QDII funds suffer from severe price distortions and frequent subscription suspensions; popular ETFs recently saw premiums soar past 35%. Stock Connect and Wealth Management Connect are limited by steep thresholds and conservative products. [para. 27][para. 28]16. High-net-worth investors can use the QDLP pilot program for offshore private funds, but approvals have largely stalled since mid-2024, and wealthy clients seeking direct trading are unlikely to shift easily to this restrictive structure. [para. 31][para. 32]17. Whether the crackdown brings capital back to the mainland remains uncertain. While fresh capital flows through grey channels are being cut off, the billions already parked in offshore bank accounts may stay in foreign-currency deposits or other offshore wealth products, depending on the appeal of China’s compliant investment channels. [para. 33][para. 34][para. 35]AI generated, for reference only

In Depth: China Slams Door on Multibillion-Dollar Offshore Trading Loophole

A sweeping two-year regulatory crackdown aims to dismantle the grey market that allowed mainland residents to trade global stocks

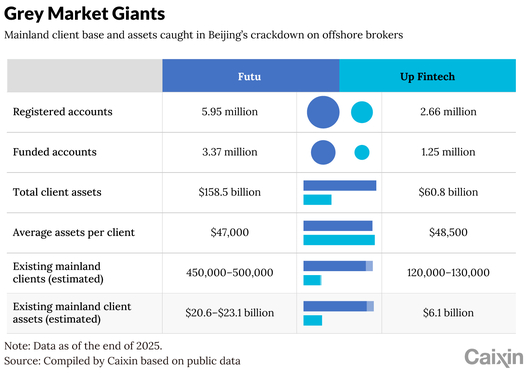

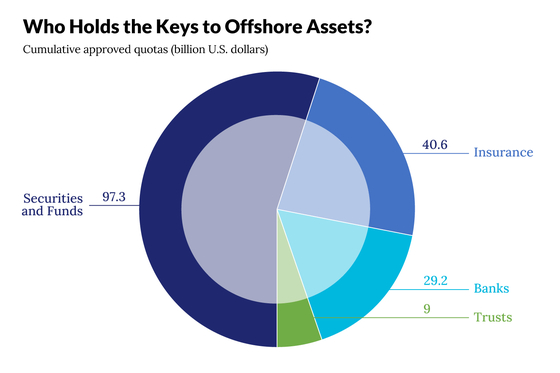

731 words~3 min read