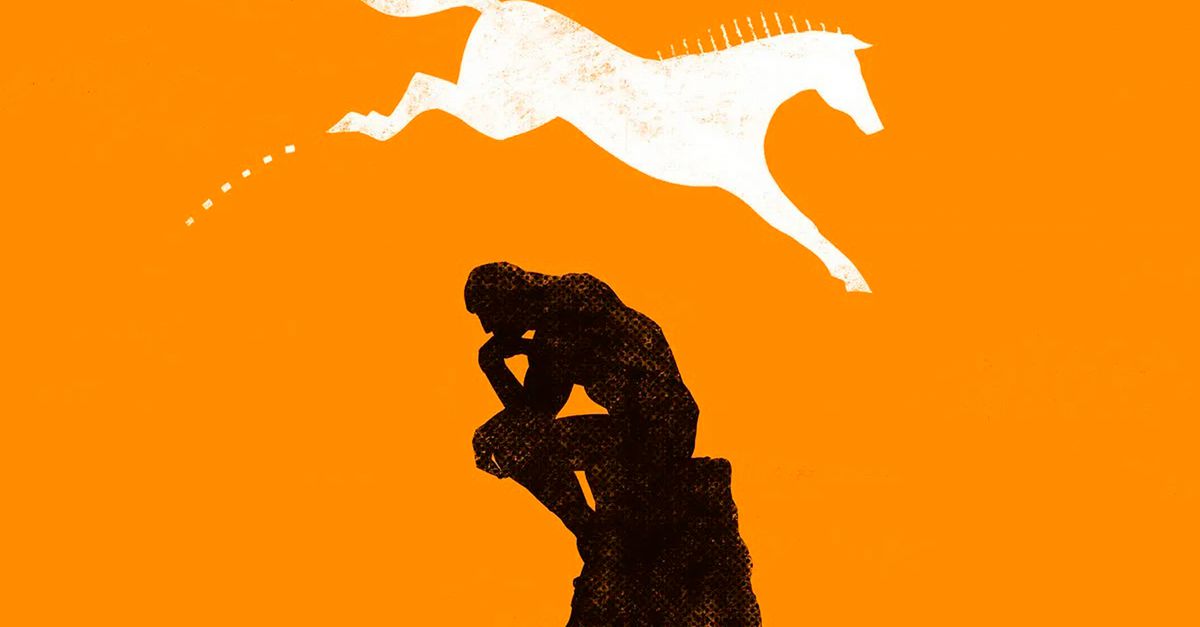

„If economists wished to study the horse,” a dismal scientist once joked, „they wouldn’t go and look at horses. They’d sit in their studies and say to themselves: ‘What would I do if I were a horse?’” But at least horses tend to be spared such attention; finance types are not. And one economic idea is especially liable to get them snorting with impatience and asking whether the person who cites it has been near a trading floor.

This is the efficient-market hypothesis, the formal version of which says that investors, in aggregate, perfectly and promptly incorporate new information into asset prices. Those who invoke it can often mean something even stronger: that markets therefore provide the best possible forecasts of fundamentals like corporate earnings. In other words, the price is always right, as it surely would be if it were economists cantering around and making all the decisions.

Right now this Platonic ideal feels especially remote. Retail traders clamour for meme stocks, whipping up prices just to give short-sellers a thrashing. Shares in GameStop, an ailing video-game seller selected for such favour in 2020, are still worth more than 20 times as much as they were then. They have done about as well as Nvidia’s, the biggest beneficiary so far of the artificial-intelligence revolution. Nvidia’s fellow tech giants are racing to issue new stock and sell it to the public—a sure sign that they reckon the bull market is nearing its peak. Yet investors are still happily piling in.