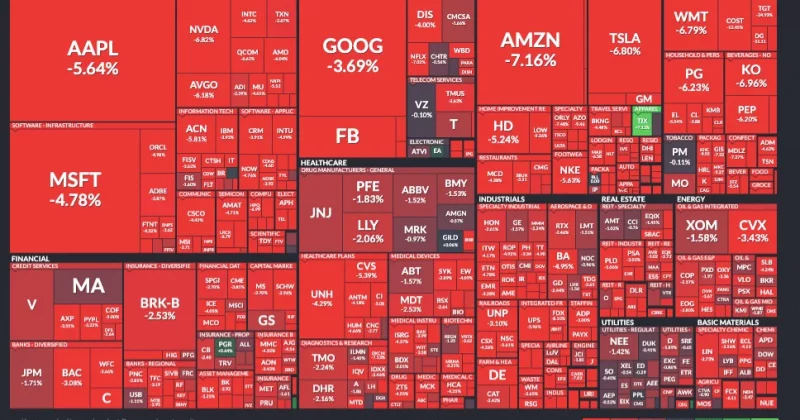

The S&P 500 fell 2.64% on June 5, closing at 7,383.74 in what became the index’s first negative week in ten. The Nasdaq Composite fared even worse, plunging 4.18% to 25,709.43 in its worst single-day performance since April 2025.

The catalyst was a one-two punch: Broadcom delivered earnings guidance that disappointed the market’s appetite for AI chip growth, and a May jobs report landed so hot it made inflation hawks look prescient. The economy added 172,000 jobs versus expectations of 80,000, pushing Treasury yields above 4.5%.

The great rotation: from momentum to defense

Healthcare and consumer staples absorbed a significant share of the capital fleeing tech. Procter & Gamble led the charge with a 5% gain, followed by Colgate-Palmolive at 4%, Coca-Cola at 3%, and Johnson & Johnson at 2%. The healthcare sector ETF XLV posted gains above 1%, while consumer staples broadly climbed more than 2%.

The semiconductor sector absorbed the worst of the damage. The SOXX ETF dropped 10% on the day. Individual names were even uglier: Broadcom (AVGO) fell 8%, Micron (MU) shed 13%, and Marvell Technology (MRVL) cratered more than 16%.