A confluence of uncomfortable data points dropped in early June 2026, forcing investors to reckon with something they’ve been quietly avoiding: the gap between AI as a transformational technology and AI as a profitable business is wider than anyone priced in.

The numbers that spooked the market

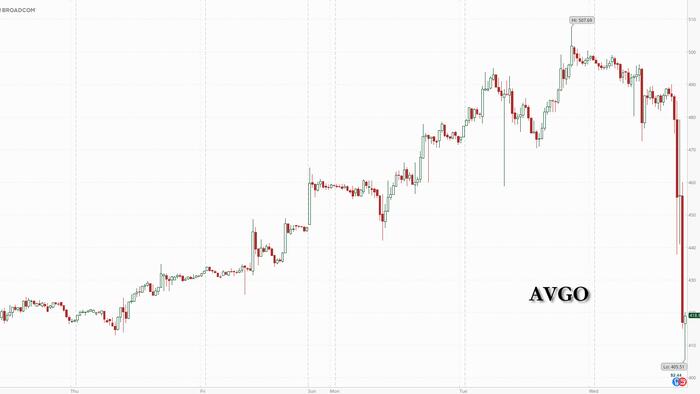

Start with Broadcom. The chipmaker’s Q3 earnings report on June 3 projected AI chip revenue of $16 billion. Wall Street expected $17.2 billion. In English: a company at the center of the AI infrastructure boom missed its own hype by over a billion dollars.

Broadcom shares dropped between 12% and 14% after the report. The damage wasn’t contained. Chip stocks broadly sold off, dragging names like Micron and SK Hynix, which had earlier posted year-to-date gains exceeding 3x and 260% respectively on the back of AI demand.

Then came the Bain survey, conducted in late May 2026, which sampled 951 companies on their AI investment outcomes. Nearly 40% of respondents reported achieving only a 0-10% reduction in costs from their AI deployments. For context, 37% of those same companies had originally targeted cost reductions in the 11-20% range.