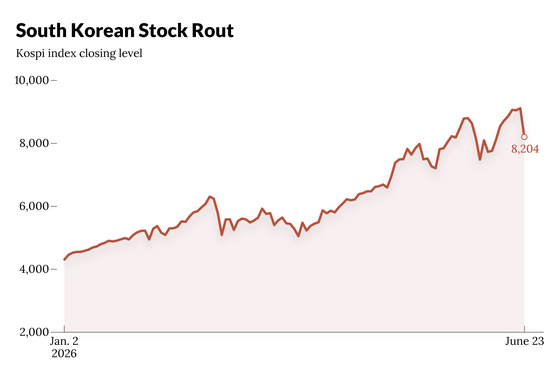

An unprecedented concentration crisis in global technology equities has evolved into a structural trap for investors, triggering a violent "Black Monday" unwind that is reverberating across Asian emerging markets, such as Korea and Taiwan. Active portfolio managers are increasingly being forced to dump their best-performing chip heavyweights because these explosive stocks have grown too large for risk compliance limits.This structural anomaly has distorted regional benchmarks, accelerated a massive migration from active to passive funds, and triggered a historic correction.The structural breakdown manifested in extreme volatility across the region's tech hubs. South Korea’s Kospi index plunged more than 8% shortly after the market opened, triggering a mandatory 20-minute trading halt before narrowing its drop as memory giants Samsung Electronics and SK Hynix rebounded from their session lows.Also Read | Kospi crashes 9%, trading halted for 20 minutes, as chip rout deepens; Samsung, SK Hynix worst hitThe Cycle of Forced SellingThe core of the market distortion lies in a mechanical paradox: As tech giants outperform, active funds are legally or structurally required to trim their holdings to manage concentration risks. Just three mega-cap tech firms—Taiwan Semiconductor Manufacturing Co. (TSMC), Samsung, and SK Hynix—now command nearly a third of the MSCI Asia Pacific ex-Japan Index.The concentration is even more extreme on a national level. TSMC occupies a staggering 41.5% of Taiwan's TAIEX, while Samsung and SK Hynix together comprise 55% of South Korea's KOSPI."We have been forced sellers of TSMC, Samsung and MediaTek," Sam Konrad, investment manager for Asia Equity Income at Jupiter Asset Management, was quoted as saying by Bloomberg. His fund must shed these chipmaking stocks despite explosive year-to-date gains of 52% for TSMC, 159% for Samsung, and 184% for MediaTek.This mechanism creates an institutional dilemma where strong performance mandates divestment, artificially capping the upside for active portfolios trying to beat their benchmarks."As equities continue to outperform, funds will find it increasingly difficult to add exposure, reinforcing a cycle of forced selling and enlarging underweight positions even amid strong fundamentals," Herald Van der Linde, head of equity strategy for Asia Pacific at HSBC in Hong Kong, noted in a research report. HSBC data confirms that TSMC has become the largest portfolio underweight among Asian and global emerging-market funds.Emerging Market Exhaustion and Fund OutflowsData from Elara Securities India confirms that the Global Emerging Market (GEM) trade is experiencing its first major phase of sustained exhaustion since its rally began. GEM fund redemptions expanded to $3 billion, the largest outflow since December 2021, marking a clear breakdown in momentum.The capital flight has extended significantly beyond Korea and Taiwan to hit other major emerging markets. China saw foreign investors pull $3.7 billion, the largest single-week redemption in over a year, while South Korea logged six consecutive weeks of foreign outflows, compounded by a record $27.9 billion foreign portfolio rebalancing outflow.The systemic nature of the unwind is visible in the broader indices. Goldman Sachs data reveals that while the MSCI Asia Pacific ex-Japan index is up 27% year-to-date, it is actually down 4% when South Korea and Taiwan are excluded.This regional distortion has accelerated a massive, unprecedented migration from active stock-picking to passive indexing. Over the last five years, Asia's active funds have suffered $269 billion of cumulative outflows. Meanwhile, passive funds have accumulated $510 billion, with a quarter of that volume arriving in just the last six months."The size of recent inflows into the region’s passive funds... has no precedent across the last 10 years," said William Bratton, head of cash equity research for Asia-Pacific at BNP Paribas Securities.This phenomenon mirrors the “Magnificent Seven” dynamic on Wall Street, where tech giants account for about a third of the S&P 500. However, concentration in Asia has unfolded at a faster and more extreme pace, turning regional indices into concentrated bets on just one or two stocks and undermining the diversification benefits of benchmark investing.Broader Trade ImplicationsThe shockwaves from the AI tech unwinding are bleeding directly into structural commodities and the wider electrification ecosystem. Precious metal funds witnessed $2.8 billion of outflows, driven heavily by gold (-$2.1 billion) and silver (-$910 million, a 12-week high redemption), while energy funds recorded their second consecutive week of outflows. These asset classes had operated as indirect beneficiaries of the global AI infrastructure and electrification trade.Furthermore, Wall Street's nine-week winning streak concluded abruptly following a hot jobs report that ignited fears of a hawkish policy pivot by the US Federal Reserve, sending technology stocks into their largest one-day decline.Despite the steep selloffs, which saw South Korean equities slide 12% and Taiwan fall 6% from their record highs, market opinions remain starkly divided on whether this correction marks a peak or a buying opportunity.Some money managers are exploiting the correction to pivot to alternatives further down the supply chain, like mid-sized semiconductor equipment makers, or shifting money toward cheaper domestic themes like robotics. China's CSI Robot Index actually bucked the broader market declines, rising 1.4%.

The AI trade trap: Why successful tech stocks are triggering a trillion-dollar market meltdown in Korea, Taiwan

A sharp tech selloff exposed concentration risks in Asian markets, where chip giants such as TSMC, Samsung and SK Hynix dominate benchmarks. As their rapid gains pushed portfolio weights beyond risk limits, active fund managers were forced to sell despite strong fundamentals. The unwind triggered market volatility, accelerated fund outflows and intensified the shift from active to passive investing.

814 words~4 min read