Traditional private credit just had its worst quarter in recent memory. New issuance plummeted to $44.76B in Q2 2026, a roughly 40% nosedive from the $74.56B recorded in the first quarter of this year.

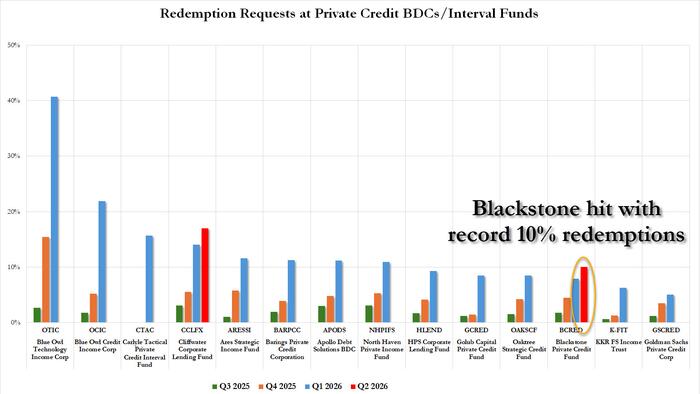

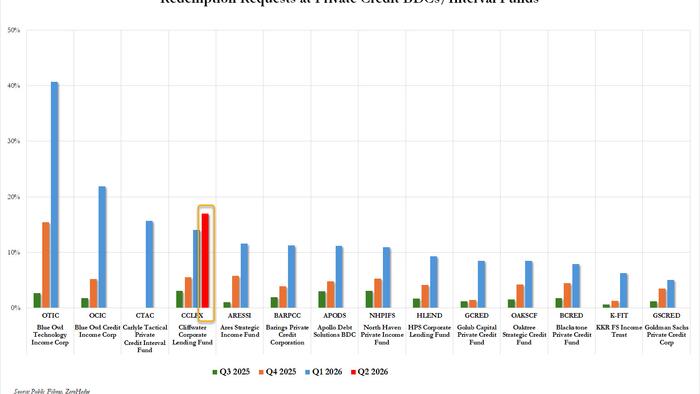

The culprit is a toxic cocktail of rising defaults, spooked investors, and redemption pressures hammering major funds. Meanwhile, the on-chain private credit market is doing the exact opposite, quietly ballooning past $14B in active tokenized loans. That’s approximately three times the size it was in early 2025.

Traditional credit markets hit a wall

US default rates in private credit surged to a record 6% as of Q2 2026. For context, that’s the kind of figure that makes institutional allocators rethink their entire portfolio construction.

This matters beyond just the private credit silo. Private credit has been one of the fastest-growing corners of finance over the past decade, absorbing deal flow that traditional banks shed after the 2008 crisis. A sharp contraction here ripples across leveraged buyouts, middle-market lending, and corporate refinancing broadly.