U.S. homebuyers can't get a break.

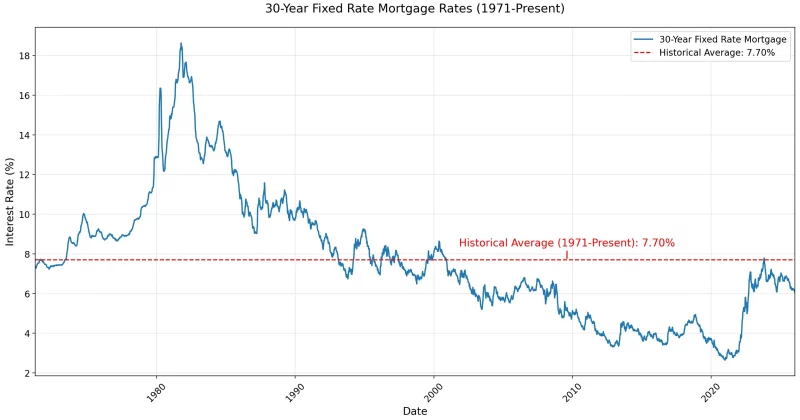

The 30-year mortgage rate has been stuck at recent highs well above 6% and now averages 6.48%, according to the data released on June 4, 2026, by Freddie Mac, which bundles and sells home loans. That marks another blow for Americans hoping to buy a home or refinance their current mortgage that had been locked in at similarly steep rates. It's also a sharp jump since February 2026, when the financing cost of a 30-year mortgage had dropped as low as 6%.

READ MORE: The 'biggest mistake' people make when they're falling behind on mortgage payments

Pricey mortgages have been weighing on the housing market more broadly, which has not escaped President Donald Trump. He has waged an aggressive campaign to pressure the Federal Reserve, which sets the short-term benchmark rate, to make deeper cuts to the cost of borrowing. The new Fed chief, Kevin Warsh, has also been touting rate cuts since he was nominated by Trump, a reversal from his earlier anti-inflation stance.

As a professor of finance, I have been asked why mortgage rates are rising even though the Fed has been keeping rates steady after a series of cuts in 2024 and 2025. The central bank actually has little control over the cost of home loans – and Americans may be stuck with high rates for a long time.