Y

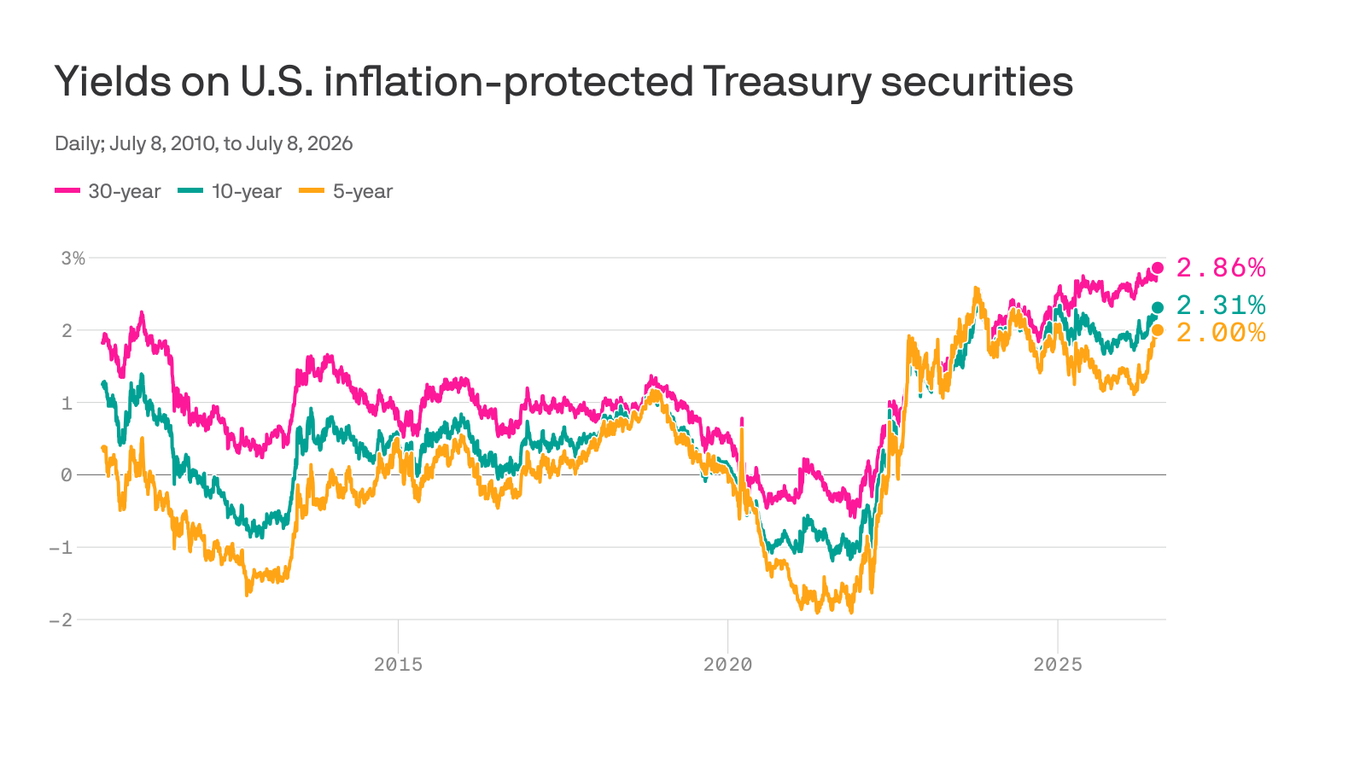

ou’re sold on the idea of adding cost-of-living protection to some or all of your bond portfolio. You’re going to invest in Treasury Inflation-Protected Securities. You know that now is a particularly good time to buy, since the yield on TIPS due in 2056 is 2.7%, close to as high as it has ever been. Now the details.

Which will be better for you, individual bonds or bond funds? Which of either of these is the best buy? If you put the investment in a taxable brokerage account, how will the taxes be computed? Do you really need one of those bond ladders that financial planners talk about? Are I bonds, the inflation-protected version of U.S. Savings Bonds, a good deal?

This article will answer those questions, beginning with the fundamental choice of fixed-income investing: bonds versus bond funds.

First rule of bonds: individual securities make sense only if you can hold at least 100 bonds ($100,000 of initial par value) in each position. For smaller stakes, the better choice is a low-cost fund. Remember that you need liquidity, whether you are a retiree planning to spend down the portfolio or a younger saver who might need cash unexpectedly.