1. On July 24, 2022, prominent figures from China’s technology and business sectors convened at a private villa at Qiandao Lake in Hangzhou, under the pretense of shareholder and board meetings for Baolide Holdings Group Co. Ltd. However, according to Hithink RoyalFlush Chairman Yi Zheng, the true purpose was a lavish private banquet where Baolide founder Yu Haijun openly displayed his relationships, creating an aura of confidence. Among the attendees was NetEase Inc. founder William Ding, who had invested nearly 1 billion yuan (approximately $140 million) through various entities in Baolide Co. Ltd., holding a 20% stake. The gathering aimed to reinforce Yu’s IPO ambitions for Baolide and sustain investor confidence, despite the company facing mounting financial pressures at that time[para. 1][para. 2][para. 3][para. 4].2. Just over two years after the Qiandao Lake event, Baolide’s problems surfaced publicly as wages went unpaid and customers reported delayed deliveries and unregistered cars. Audits and court documents indicated the company’s financial distress predated the gathering. Baolide’s collapse drew in major entrepreneurs and institutional investors, including the private equity firm Hillhouse, exposing the dangers of relationship-driven (guanxi) investment strategies prevalent in China’s private sector[para. 4][para. 5].3. Baolide’s dramatic crisis became public in September 2024 when its funding chain snapped. In November 2025, a Hangzhou court ordered comprehensive bankruptcy liquidation for Baolide and 56 affiliated entities because their finances were so intertwined that they could not be separated. At its zenith, Baolide was one of East China’s largest luxury car dealers, running over 30 dealerships and holding rights to prestigious brands like Rolls-Royce, Aston Martin, Mercedes-Benz, and Jaguar Land Rover. Yet, the slowing Chinese auto market and the rise of electric vehicles destabilized the traditional dealership business model. Between 2016 and 2024, Baolide paid nearly 2 billion yuan in interest on private loans, relying on costly financing that eroded its cash position[para. 6][para. 7][para. 8][para. 9].4. The origins of Baolide’s failure lay with Yu Haijun’s fixation on launching an IPO. In 2016, Minsheng Life Insurance Co. acquired a 25% stake in Baolide Co., contingent on a “bet-on agreement” requiring Baolide to repurchase the investment at a 12% annualized return if it failed to list by late 2018. As the IPO never materialized and repayment obligations grew, the principal plus interest reached nearly 1.2 billion yuan by December 2023. Yu attempted asset restructurings and alternate listing strategies, shifting key assets to Baolide Network Technology Service Co. Ltd. for a planned Hong Kong IPO, while raising about 1.3 billion yuan from new investors, including NetEase’s Ding and Alibaba’s Hu Xiaoming[para. 10][para. 11][para. 12][para. 13][para. 14].5. Audited financials were provided to attract investors, showing a 2020 net profit of 862 million yuan and net assets near 2.4 billion yuan, later used for due diligence by Hillhouse, which invested 300 million yuan via a convertible bond. However, later investigation revealed these figures had been inflated, with actual net profit around 543 million yuan and net assets approximately 1.2 billion yuan. When the capital chain snapped in September 2024, both the IPO and buyback promises proved untenable, leaving investors exposed[para. 15][para. 16].6. Investors were swayed not only by financials but also personal relationships (“guanxi”). Lü Zhonglin of LianLian DigiTech played a key role as a connector, lending credibility and introducing Yu to business elites, though Lü denied close personal links with Yu. As financial pressures escalated, Yu leveraged these relationships to secure funding and guarantees. The Baolide episode highlights the risks of guanxi-driven investing, where personal trust can overshadow independent checks, contributing to major losses[para. 17][para. 18][para. 19][para. 20][para. 21][para. 22].7. Audits into Baolide revealed highly entangled cash flows and inflated asset figures through circular transactions among group companies. Baolide, Yu, and his wife Chen Yingfei were found to have misappropriated nearly 3.4 billion yuan from Baolide Co. Yu publicly denied fraud, blaming the Minsheng Life dispute and market downturn for the company’s demise. Authorities were cautious, with police declining to prosecute Yu for contract fraud due to challenges in proving intent, though a separate misappropriation case was accepted. Yu and Chen faced exit bans, though Chen reportedly left the mainland in July 2025. Amid mounting troubles, Yu shuffled assets, including transferring property to relatives and dealing with ensuing disputes[para. 23][para. 24][para. 25][para. 26][para. 27][para. 28][para. 29].8. The fate of investors is bleak, with bankruptcy filings confirming Baolide’s deep insolvency and the virtual impossibility of recovery, culminating the story of a business empire marked by high hopes, lavish gatherings, and ultimately, systemic and personal failures[para. 30].AI generated, for reference only

In Depth: How China’s Tech Elite Got Burned by Luxury Car Dealer Baolide’s IPO Mirage

A lakeside banquet, star investors and altered accounts show how trust masked mounting risks

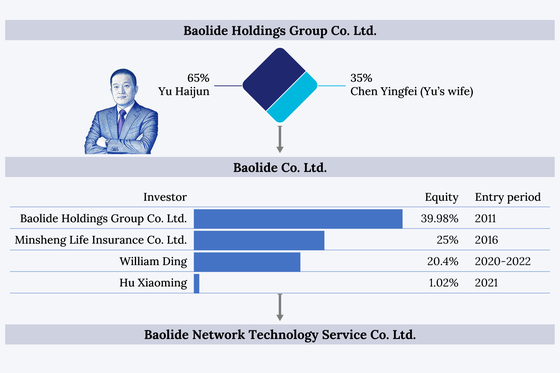

750 words~3 min read