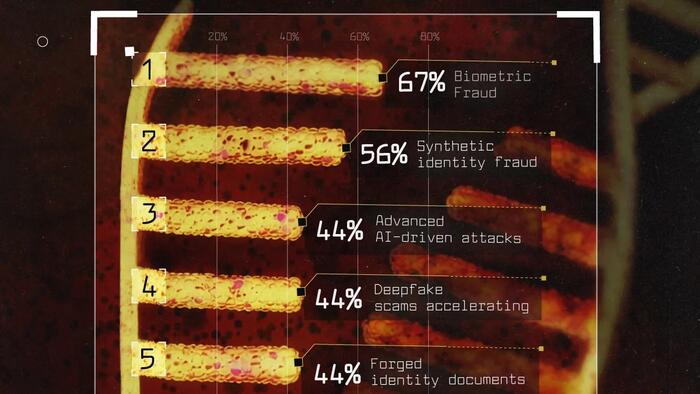

At a time when AI-generated deepfakes, digital arrests, cyber-enabled financial frauds and crypto-powered crime networks have become increasingly sophisticated, combating these next generation of fraud would require a fundamental shift towards advanced forensic technologies, real-time intelligence sharing and stronger collaboration between regulators, businesses and law enforcement agencies said experts at the FICCI Conference on Next-Gen Forensics: The New Age of Fraud Investigation that was held in Mumbai.Brijesh Singh, IPS, Principal Secretary, Government of Maharashtra, said that cybercrime has evolved into a highly organised and industrialised ecosystem where specialised actors perform different functions ranging from data theft and identity creation to mule networks, deepfake generation and crypto-enabled money laundering.“Today, fraud has become an industrial-scale enterprise. By the time the first call reaches a victim, fraudsters may already know their personal details, behavioural patterns and psychological vulnerabilities. The entire chain, from data acquisition to money movement through crypto networks—can be completed in less than 30 minutes, making traditional investigative approaches increasingly ineffective,” said Mr Singh.He further emphasised that the rise of AI, deepfakes and digital evidence requires a complete shift in investigative methodologies. “Trust is being weaponised in the digital era. With voice cloning, deepfake technologies and fraud-as-a-service platforms becoming easily accessible, investigators need integrated forensic platforms, real-time intelligence sharing and new evidentiary frameworks to effectively detect, investigate and prosecute digital crimes,” he added.Govindayapalli Ram Mohan Rao, Executive Director, Market Intermediaries Regulation and Supervision Department, SEBI, stated the market regulator’s ongoing efforts to strengthen investor protection and digital trust through technology-driven governance measures remains the cornerstone of capital markets. “SEBI has introduced initiatives such as SEBI Check, App Check and UPI verification mechanisms to help investors identify legitimate entities and prevent fraud. Strengthening cybersecurity systems, conducting periodic audits and leveraging advanced surveillance technologies are essential to safeguarding the integrity of India’s securities markets,” Mr Rao said.He also underscored the importance of preventive action and digital vigilance in combating fraud. “Prevention is always better than investigation after the event. Through proactive surveillance, monitoring of misleading content, platform coordination and technology-enabled detection systems, we are working continuously to reduce fraud risks and build greater digital trust across the financial ecosystem,” he added.Presenting the findings of the FICCI-KPMG report, Suveer Khanna, Head & Partner – Forensic Services, KPMG India, said that the scale of digital transformation has significantly expanded the fraud threat landscape.“Internet connectivity has multiplied, data consumption has grown exponentially, and digital payment adoption has transformed the economy. At the same time, fraud has evolved into an organised industry. Organisations must move beyond siloed responses and focus on intelligence-led investigations, collaborative risk management and institutional learning to strengthen resilience against emerging threats,” Mr Khanna said.Amey Mirajkar, Partner, Khaitan & Co, said, “India’s digital economy is expanding at an extraordinary pace, but the same infrastructure that enables faster and efficient financial transactions is also being exploited by increasingly sophisticated fraud networks.”“Investigations today routinely involve virtual assets, encrypted communications, digital evidence, and cross-border networks, creating challenges for businesses, regulators and enforcement agencies alike. The knowledge paper examines how legal and compliance frameworks can adapt to address these emerging risks more effectively,” he added.

New age fraud: “Trust is being weaponised in the digital era”

At a time when AI-generated deepfakes, digital arrests, cyber-enabled financial frauds and crypto-powered crime networks have become increasingly sophisticated, combating these next generation of fraud would require a fundamental shift towards advanced forensic technologies, real-time intelligence sharing and stronger collaboration between regulators, businesses and law enforcement agencies said experts at the FICCI Conference on Next-Gen Forensics: The New Age of Fraud Investigation that was held in Mumbai.

517 words~2 min read