These days, the eyes of the global financial world are fixed on St. Petersburg. The investment forum, dubbed the "Russian Davos" by Western media, has opened its doors in an extraordinary atmosphere. On display, defying Western sanctions, are popular figures of the American right like Candace Owens and Andrew Tate, alongside European billionaires such as Germany's Thomas Bruch. Through this lineup, the Kremlin sells the illusion that it remains a center of attraction for the global economy.

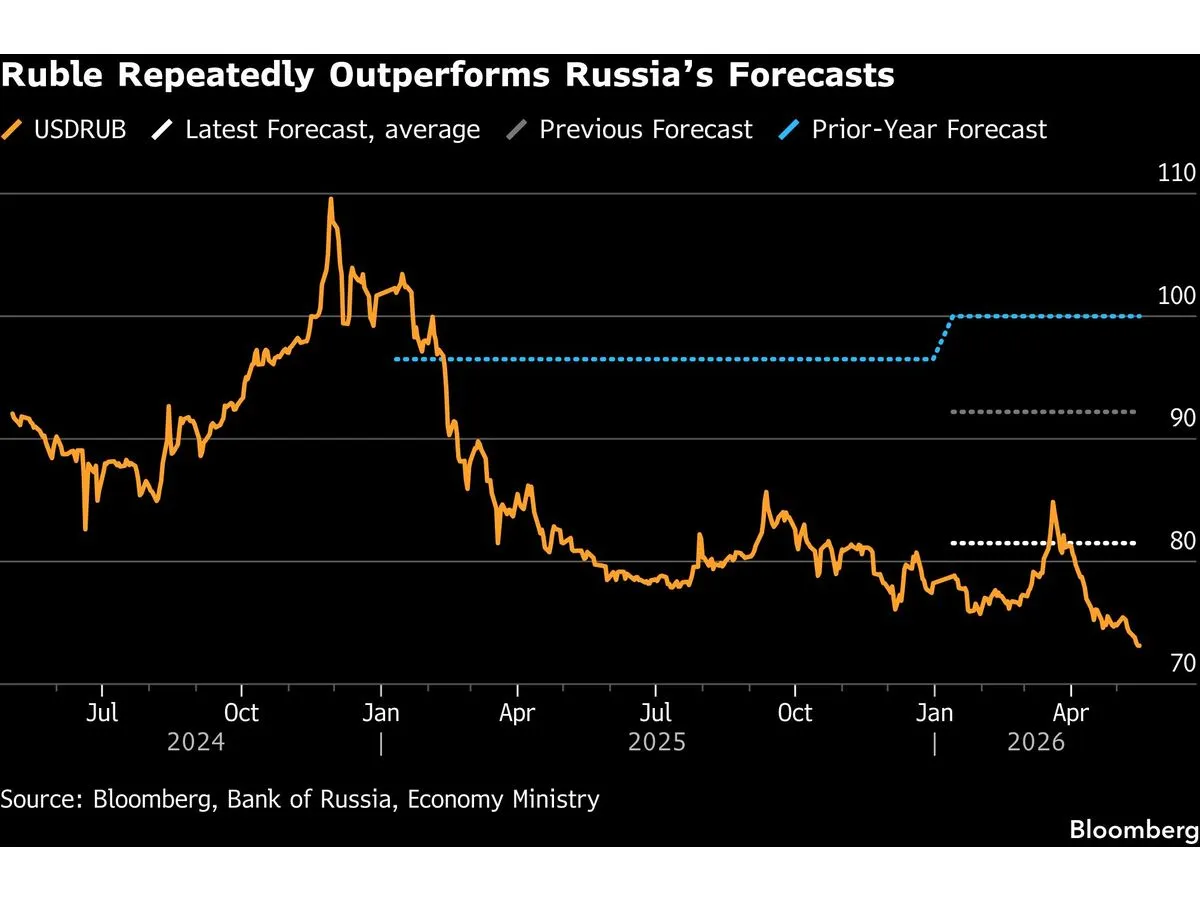

Yet, behind this glamorous runway, two staggering pieces of data expose the real economy behind the headlines: on the one hand, a surging Russian ruble in the wake of the Middle East shock, and on the other, oil refineries struck by Ukrainian drone strikes.

The fundamental textbook rule of economic science, Ceteris Paribus, meaning "all other things remaining constant," shatters in this savage arena of geopolitics. Because in the real world, no variable is static. While Russia survives the day under the illusion of a short-term price victory handed by a conflict entirely outside its control, which is the U.S.-Iran conflict, it is watching its own economic pool drain due to locked production volumes and draining budgetary costs in the long run.