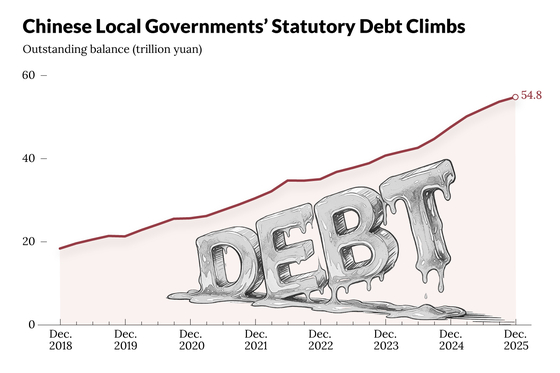

Local government financing vehicles (LGFVs) in China, which have accumulated trillions of dollars in debt, are seeking to rapidly transform themselves into market-driven entities amid mounting financial pressures. Historically, LGFVs have been extensively used by local governments to fund infrastructure and public welfare projects, often bypassing official government budgets to boost GDP growth [para. 1][para. 6]. However, as of late 2023, China's Ministry of Finance reported that hidden off-the-books LGFV debt had ballooned to 14.3 trillion yuan (approximately $2 trillion) [para. 7]. In response to this unsustainable level of debt, regulatory reforms now require LGFVs to fully transition into self-sustaining, market-oriented organizations by June 2027 [para. 2][para. 12].These changes come in light of strict new regulations making it nearly impossible for LGFVs to raise further funds. Many insiders suggest that some LGFVs are only making symbolic changes, manipulating financial statements to inflate trade revenue and claim market transformation [para. 4]. Even those finding legitimate new business models still face difficulties in attracting new financing due to their lingering LGFV legacy, which brings heightened scrutiny [para. 5]. The political push for reform intensified in 2023, when a nationwide debt resolution campaign was launched and LGFVs were categorically listed for enhanced regulatory oversight [para. 9]. LGFVs on the list are now prohibited from taking on new debt except to refinance existing debt or support major state-mandated projects like affordable housing and renovation of urban areas [para. 10].The central government has mandated that by the end of June 2027, all LGFVs must extinguish their hidden debt and fully convert into market entities [para. 12]. The Politburo has clearly signaled its determination for this transformation, using strong language such as “forceful, orderly and effective clean-up” of LGFVs [para. 13][para. 15]. Local governments are thus under pressure to utilize all previous policy resources to manage these transitions [para. 16].Delisting from supervisory lists is contingent on LGFVs meeting several criteria: clearing hidden government debt, obtaining creditor approval or eliminating commercial debt, and fully shedding government financing functions [para. 19]. In 2024, the pace of delisting accelerated, especially after a 10 trillion yuan debt resolution package was introduced in November. Over 7,000 LGFVs were delisted last year, with more than two-thirds of annual removals occurring after this package’s announcement [para. 22]. High-debt regions especially prioritized delisting to escape investment restrictions, and by the end of the year, 70% to 80% of all LGFVs on the 2023 list are expected to have been delisted [para. 25].Nonetheless, many delisted former LGFVs struggle to access new capital. They remain under tough compliance and a one-year risk monitoring period post-delisting, with local governments and banks cautious in granting them additional credit [para. 27][para. 29]. Approaches to transformation include boosting market-based revenue, acquiring listed companies, and shifting business models, although in practice, many efforts are superficial and primarily designed to circumvent restrictions [para. 31][para. 33]. Industry insiders caution that the transformation process remains largely experimental and faces challenges such as low asset quality, weak management, and tenuous links to industrial activity [para. 37]. Experts advise that genuine transformation will require more time and that campaign-style delisting may actually increase risks [para. 43][para. 44]. The key to longer-term success lies in improving the asset structure and financial health of both transitioning and remaining LGFVs [para. 41].AI generated, for reference only

In Depth: The Unfinished Transformation of China’s LGFVs

Facing a 2027 deadline, some local government financing vehicles are just dressing up and still struggling to secure fresh funding

TL;DRAI

China's LGFVs must shed $2T hidden debt by June 2027; 7,000+ already delisted in 2024 under regulatory pressure. Weak asset quality and superficial reforms signal persistent credit instability, raising financing risk for tech enterprises with China exposure.

547 words~2 min read