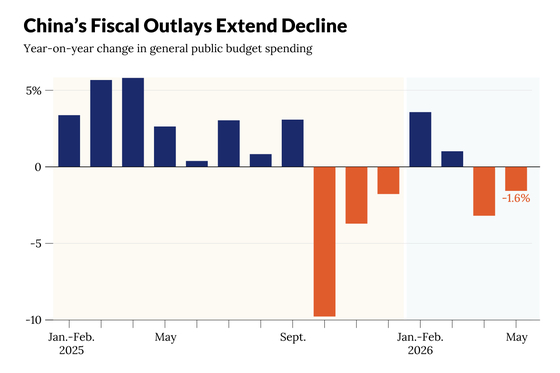

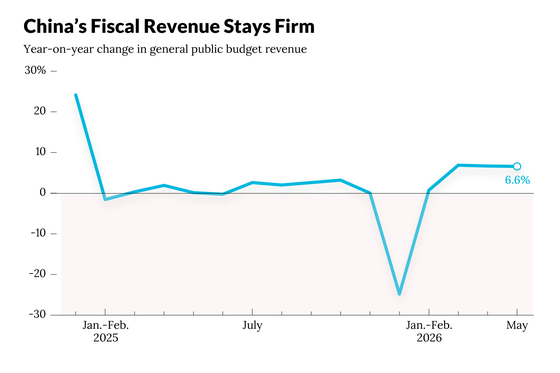

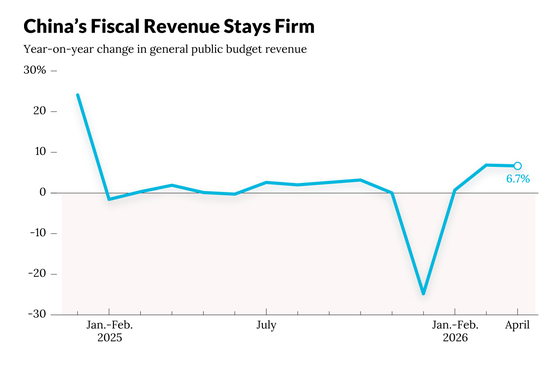

1. The 2025 budget reports from 31 Chinese provincial-level regions indicate a broad-based recovery, with overall fiscal revenue growing 2.4% and all but four regions reporting increases [para. 1]. However, this headline masks deeper structural pressures: traditional revenue streams, especially land sales from the real estate slump, continue to collapse [para. 2][para. 3]. Governments have turned to monetizing state-owned assets as a key tactic to plug budgetary holes, driving nontax revenue growth [para. 3][para. 4].2. Despite the recovery, land sale revenue—a key part of the government-managed fund budget—fell in 17 of 25 regions releasing data, with double-digit declines in 11 provinces including Shaanxi and Jiangsu [para. 7][para. 8]. Nonetheless, S&P Global Ratings notes that land sales and real estate taxes now account for only 13% of total adjusted local fiscal revenue in 2025, down from 36% five years ago, reducing their impact [para. 9][para. 10]. Local governments expect tight budgets for 2026; for example, Henan province faces sluggish tax growth from pillar industries, limited room for nontax revenue growth via asset monetization, and rising spending commitments for debt interest, social programs, and urban maintenance [para. 11][para. 12][para. 13][para. 14].3. To compensate for shortfalls, many local governments are increasingly monetizing state-owned assets, generating crucial nontax revenue [para. 16]. In Shaanxi, nontax revenue jumped 11.6% to 87.1 billion yuan, driven by a 54.3% surge in revenue from farming out mining rights (34.9 billion yuan) [para. 17][para. 18]. Similar patterns emerged in Tianjin, Hubei, Sichuan, Chongqing, and Jilin, where revenue from monetizing state resources drove growth while fines and confiscations stagnated [para. 19]. Jilin’s fiscal revenue grew 13.3% (second-fastest nationally), largely due to a 25.4% surge in nontax revenue, while tax revenue grew only 4.3% [para. 20]. This was fueled by a provincial campaign to inventory state assets, generating 110.9 billion yuan from idle resources [para. 21]. Other provinces like Hunan and Liaoning similarly reported windfalls in the tens of billions [para. 22]. The approach has become formalized: Chongqing, a pioneer, aims to monetize 200 billion yuan of assets in 2026, after generating 198.4 billion yuan last year [para. 23][para. 24].4. As they hunt for new revenue, local governments enforce new rules to manage mandatory “three guarantees” spending—for basic livelihoods, wage payments, and government operations [para. 26]. These guarantees accounted for nearly 40% of fiscal spending in Guangxi last year [para. 26]. Jilin has placed these funds in special accounts, while Henan uses a county-level digital tagging system, ensuring no other expenses (except emergency relief) are paid until those obligations are met [para. 27][para. 28]. Meanwhile, China’s campaign against hidden local government debt has entered a new phase: many provinces exceeded targets for bringing borrowing onto official balance sheets, but swapping hidden debt for government bonds has created new repayment challenges [para. 29]. Some regions are establishing dedicated funds to guarantee timely bond repayment; Jiangxi set one up, and Guangdong and Guizhou are exploring similar measures this year [para. 30][para. 31].AI generated, for reference only

Analysis: China’s Local Fiscal Recovery Hides Scramble to Plug Budget Holes

A look beyond headline growth figures reveals how provinces are relying on the monetization of state assets to fill in the gaps left by the collapse of traditional sources of revenue, such as land sales

TL;DRAI

31 province cinesi crescita +2.4% 2025, ma land sales crollano in 17; governi monetizzano asset: Shaanxi mining rights +54.3% (34.9B yuan). Segnale: strain budget pubblici cinesi anticipa capex ridotto in tech player locali e meno M&A/deal in Asia nel 2026.

492 words~2 min read