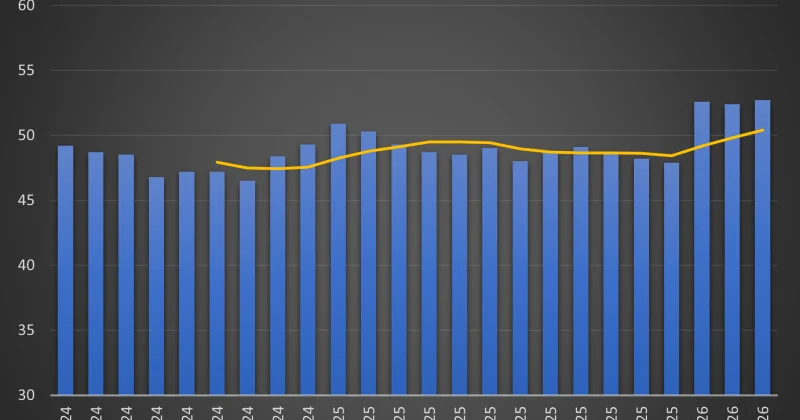

Growth in activity across India’s manufacturing sector in May came in stronger than what was suggested by Flash PMI numbers released earlier, final numbers for the HSBC India Manufacturing PMI released by S&P Global on Monday showed, indicating continued stockpiling amid the protracted conflict in West Asia.The data showed that manufacturers stepped up purchases, new orders and output at a faster pace than in April. (File)The seasonally adjusted manufacturing PMI, a gauge of overall conditions derived from measures of new orders, output, employment, supplier delivery times and stocks of purchases, rose to 55 in May—higher than both April’s final reading of 54.7 and the May flash estimate of 54.3. A reading above 50 indicates expansion from the previous month. The final PMI print pointed to the strongest improvement in manufacturing sector conditions in three months.The data showed that manufacturers stepped up purchases, new orders and output at a faster pace than in April, with stockpiling gaining strength as a result. “India’s final manufacturing PMI points to another month of possible precautionary stockpiling as the Middle East conflict remains unresolved. Output growth accelerated, while purchasing activity and stocks of finished goods rose at a faster pace,” said Pranjul Bhandari, Chief India Economist at HSBC.Manufacturers reported the fastest growth in new orders and output since February. The improvement was driven by stronger gains in the intermediate and capital goods segments, even as consumer goods makers saw growth slow. Domestic demand provided the main boost, while new export orders rose at a softer but still solid pace. Firms reported higher international sales to markets in Asia, Europe, Kenya, Nigeria and West Asia.The war in West Asia continued to keep cost pressures elevated in May, even though they eased marginally from April, with manufacturers reporting higher spending on energy, fuel, materials and transportation. Input prices rose sharply, with only April seeing a stronger increase in the past 45 months. Cost inflation was highest among capital goods producers, followed by intermediate and consumer goods firms.Factory gate prices also rose at a solid pace, but the increase was weaker than input cost inflation and below the average seen over the past year. Only 8% of firms said they passed higher costs on to customers, while others held back because of competitive pressures, suggesting a potential squeeze on margins.Despite sharp increases in input costs, manufacturers stepped up purchases of raw materials in May. Buying activity rose at the fastest pace in three months and remained above its long-run trend, as firms sought to build contingency stocks.Supplier delivery times shortened again, though by less than in April, helping manufacturers add further to pre-production inventories, for which the pace of accumulation was the strongest in three months. Finished goods inventories also rose for the second month in a row, as some firms said supply had exceeded demand. While the increase was moderate, it was the fastest accumulation of finished goods stocks in 11 years.Higher production requirements meant that employment continued to rise at a solid pace in May, although growth eased from April. Outstanding business also increased for the second straight month, but only marginally and at a pace broadly similar to April. Business confidence remained positive, supported by hopes that cost pressures will ease later in the year, alongside advertising efforts and strong order pipelines.

Manufacturing sector growth hits 3-month high in May

The final PMI print pointed to the strongest improvement in manufacturing sector conditions in three months. | Business News

TL;DRAI

India's manufacturing PMI reached 55 in May (3-month peak), lifted by accelerating output and inventory building. Input inflation at 45-month highs but only 8% raised prices—margin squeeze accelerates enterprise demand for supply chain automation solutions.

547 words~2 min read