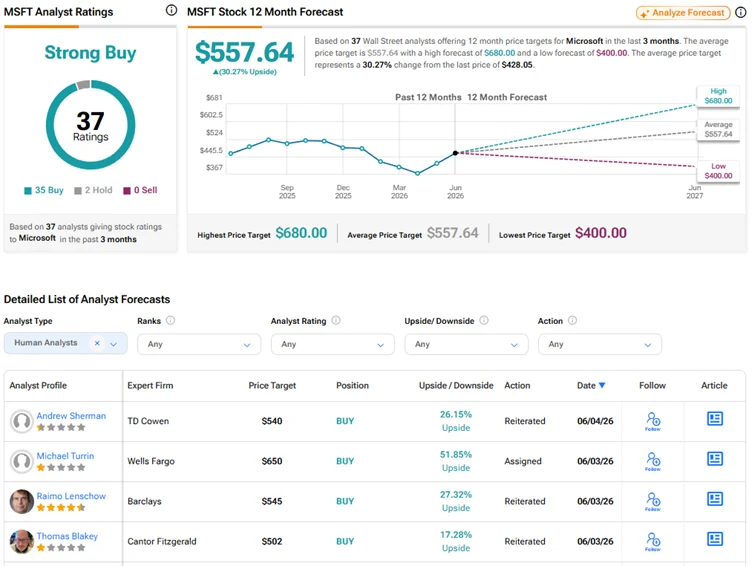

Wells Fargo just raised its price target on Microsoft from $625 to $650, keeping its Overweight rating intact. The thesis is straightforward: Microsoft’s AI business is becoming too big to ignore, and the stock has room to run.

The adjustment reflects growing confidence that Microsoft’s homegrown AI efforts, particularly Azure cloud services and its Copilot suite, are translating into real revenue momentum.

The AI revenue machine

Wells Fargo has previously projected that Microsoft’s AI business could reach $100 billion in revenue. For context, that figure alone would make Microsoft’s AI division larger than most standalone companies in the S&P 500.

The broader Wall Street consensus on MSFT spans a wide range. Analyst price targets stretch from a low of $400 to a high of $870, with the average landing near $561. Wells Fargo’s $650 target puts it firmly in the bullish camp, though not at the extreme end of optimism.