Discover high-conviction stock picks and new investing opportunities with the TipRanks Smart Investor Newsletter

Alphabet: The stronger full-stack AI platform

Alphabet’s bull case is that AI is not killing Google Search. In fact, Q1 showed Search revenue growth of 19%, as queries reached an all-time high. That helps push back against the biggest bear case, which is that ChatGPT-style tools will slowly eat away at Google’s core advertising engine. At the same time, Google Cloud is becoming a much bigger part of the story, with revenue reaching about $20 billion in Q1 and growing 63% year-over-year.

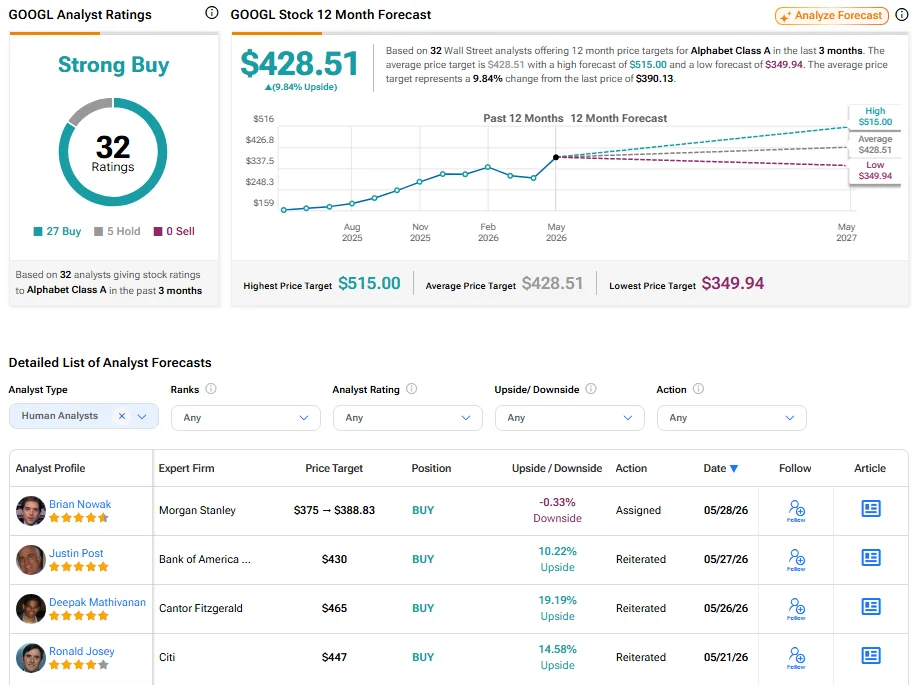

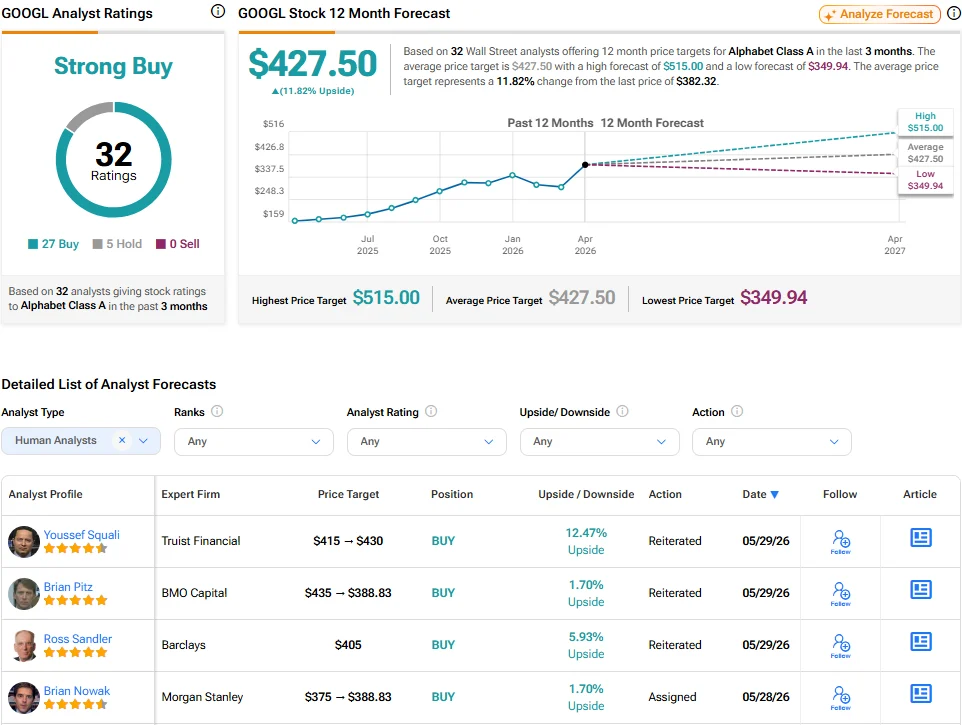

Unsurprisingly, analysts have become more optimistic due to this cloud acceleration. Recent data shows Alphabet still has a Strong Buy consensus, with an average GOOGL price target of $427.50, implying roughly 12% upside from recent levels. The risk is that Alphabet is spending heavily, with 2026 AI capex expected to reach up to $190 billion, which could pressure free cash flow if returns take longer to materialize. Still, Alphabet has the advantage of owning a full AI stack that includes Search, YouTube, Cloud, Gemini, TPUs, Android, and Waymo.

Amazon: The stronger AI monetization and margin story